Personalization is all around us, with today’s consumers interacting daily with the likes of Amazon, Netflix, Spotify, and others that are providing seamless and highly relevant experiences across touchpoints.

And these cannot be viewed in a vacuum.

Expecting the same from every company they engage with, all industries must now strive to provide greater levels of 1:1 marketing, including those in financial services.

Still need convincing?

Well, let’s consider the fact that a majority of customers have already moved to primarily digital-centric banking relationships, with 45% having moved to mobile and 27% now using the web. Not only that, but 65% of consumers either agree or strongly agree that banks should make it easier to find and shop for financial products, and another 72% think that product offers are more valuable when they’re tailored to their individual needs.

But the benefits of a tailored experience aren’t just about meeting consumer demand – companies who get it right are rewarded with higher engagement, loyalty, and revenue.

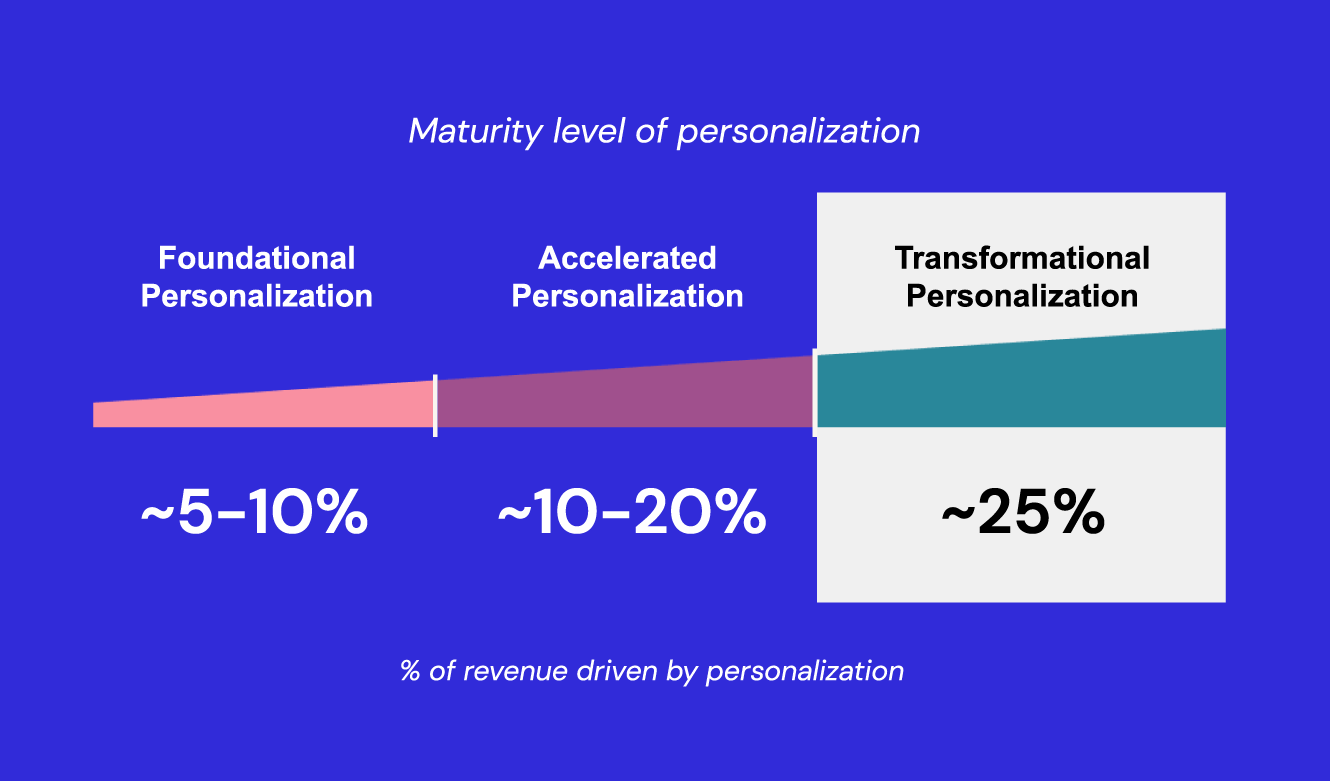

Adapted from McKinsey benchmarking survey on personalization performance.

While personalization is a journey and not a destination, as well as more about programs than projects, those practicing even “foundational” levels can expect to see lifts in revenue between 5-10%, with increased maturity resulting in 10-20% at an “accelerated” state and 25% driven at the “transformational.”

So what are the major ways in which personalization can help businesses move the needle?

The growing shift toward digitally-centric banking impacts customer acquisition on two fronts: a bank’s physical location no longer plays the critical role it once did, and the market is saturated with more consumer options than ever before.

Leading to increased spending on paid media campaigns and referral programs, customer acquisition costs (CAC) are also on the rise, with little actually being done to meet the rising expectations for more personalized experiences from unknown, first-time, or returning visitors.

There is so much opportunity to optimize post-click experiences.

For starters, basic campaign data from ads and social networks can be used to tailor the site upon a visitor’s arrival and first pageview. For example, a user can be assigned as part of a “Students traffic” segment if they clicked through a Facebook ad that was targeted to students, with the appropriate content, recommendations, offers, or products all set up to more effectively connect to that audience. Further, machine learning algorithms could then allow for continuous optimization of those experiences to ensure the best possible variation was shown over time.

Guided selling tactics can also recreate an in-person consultative experience to identify the customer’s needs and interests by asking questions to determine the right core banking product or service.

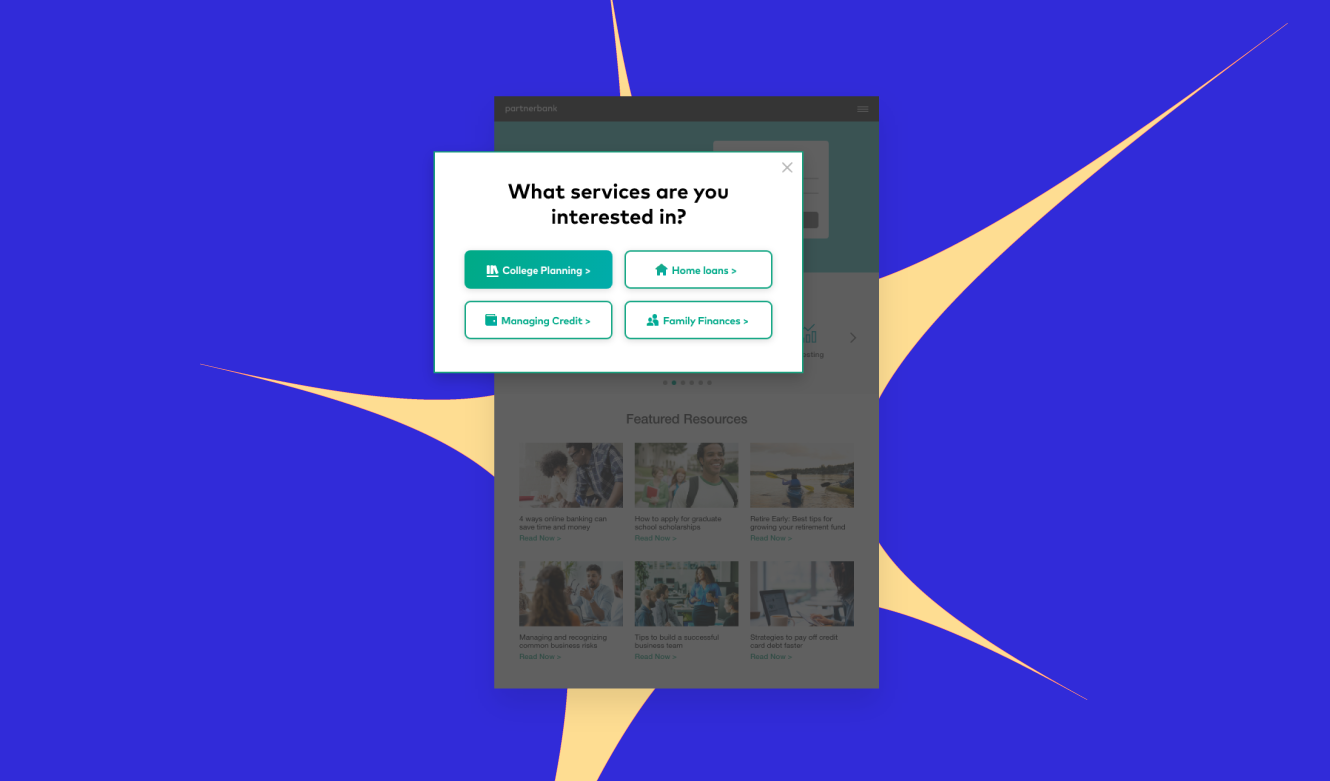

Self-segmentation pop-ups help deliver immediate personalized experiences using the customer’s own inputs.

This not only enables brands within financial services to collect invaluable information in the form of explicit feedback on the part of the visitor (think financial goals, retirement information, and more), but the inputs can go on to be used for delivering more relevant experiences in-the-moment, both easing and expediting the discovery process.

Major US financial institution, Synchrony, harnesses data from LiveRamp to enhance its CRM platform and better differentiate the homepage between first-time visitors and current cardholders. For example, if a visitor is not an existing customer, they are shown the site’s most popular and local offers, whereas a customer cardholder is served more personalized offers based on their credit card type.

And the above reflects just the tip of the iceberg when it comes to boosting acquisition efforts with personalization.

Personalization can be leveraged throughout the customer lifecycle beyond acquisition and into the hard work of driving ongoing engagement. And while this can factor into longer-term goals like loyalty and digital wallet share (which we’ll touch on later), a more immediate impact can be made as it relates to activation, an early month on book, add-to-mobile-wallet, and attrition.

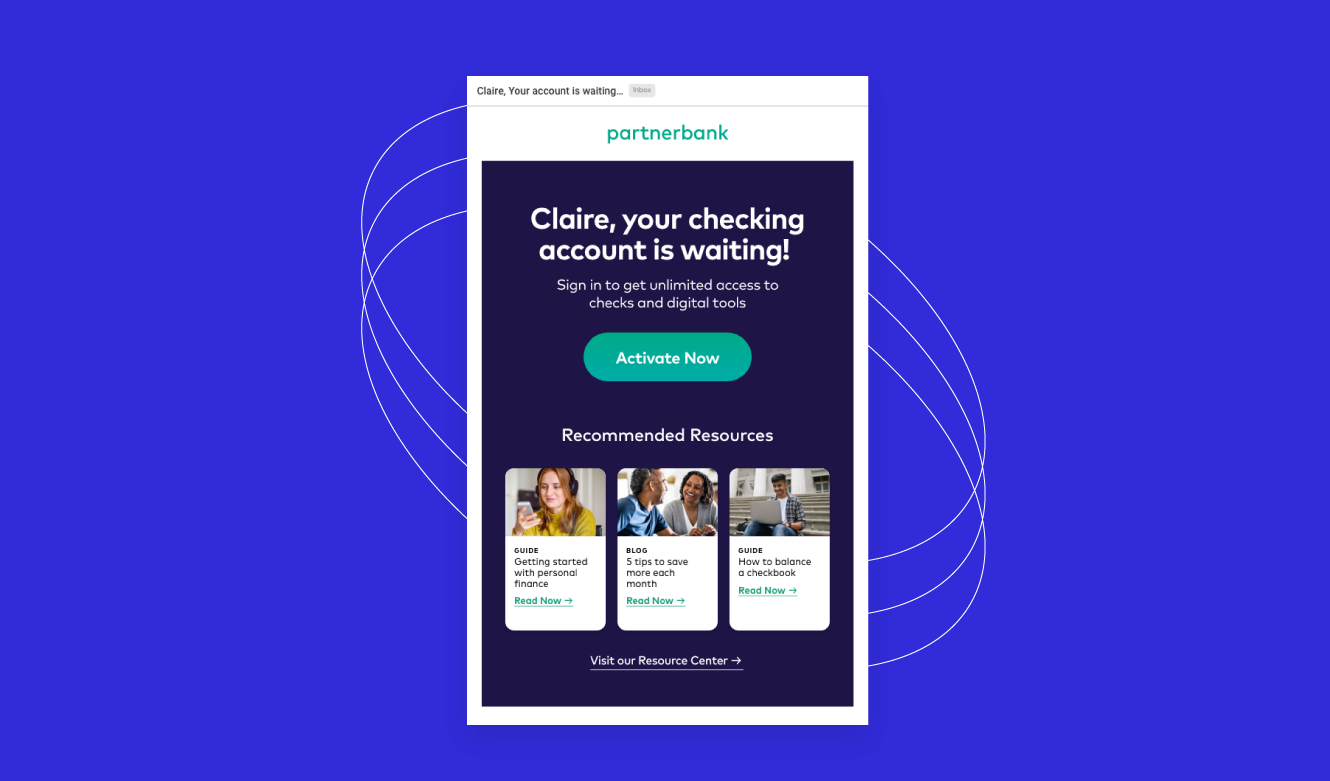

For instance, banks can reach customers at critical moments in the customer journey by triggering emails or push notifications to encourage the incredibly important step of account activation, either shortly after acquisition or when they’ve become inactive. This tactic can also be used to drive push-to-wallet among cardholders, auto-pay registration, or loan application completion, with personalized recommendations and educational content layered in to incentivize action.

Triggered emails like this one use recommended resources to encourage customers to activate their checking accounts.

Incorporating behavioral data can help to understand a visitor by who and where they are, allowing FSIs to identify disengaged or inactive customers and re-engage them with relevant promotions in previous spending categories through triggered emails or push notifications.

A/B testing can further optimize each of the moments above and beyond, ensuring the highest levels of desired action for a given situation through the testing of different messages, layouts, and content variations either site-wide or as part of a strategic audience strategy for financial services.

Once acquired and engaged on a foundational level, how can financial brands then inspire loyalty and drive higher customer lifetime value for the business?

Given 50% of consumers wish that their bank was more proactive about giving them relevant financial information and advice, the use of personalized offers, educational content, and advice can be the difference between a short-term or single-service customer and a long-term, multi-account advocate.

Imagine recommending additional products or services based on the customer’s previously displayed affinities (e.g. travel perks, luxury credit cards) paired with real-time social proof messaging to increase confidence in decision-making.

Social proof messaging combined with affinity and popularity recommendation strategies helps to increase conversions.

Individual account data can also be used to stimulate spending in new categories with relevant offers in the app – for example, highlighting promotions on dining and gasoline to a user who frequently purchases groceries.

With an ever-increasing percentage of online transactions, fewer physical wallets are being opened in favor of saved payment methods and digital wallets – and the top-of-wallet battle is fought and won long before a customer reaches a cash register (or more accurately, a checkout page). This is exactly why FIs want to encourage their card to be made the preferred customer option in the first 60-90 days.

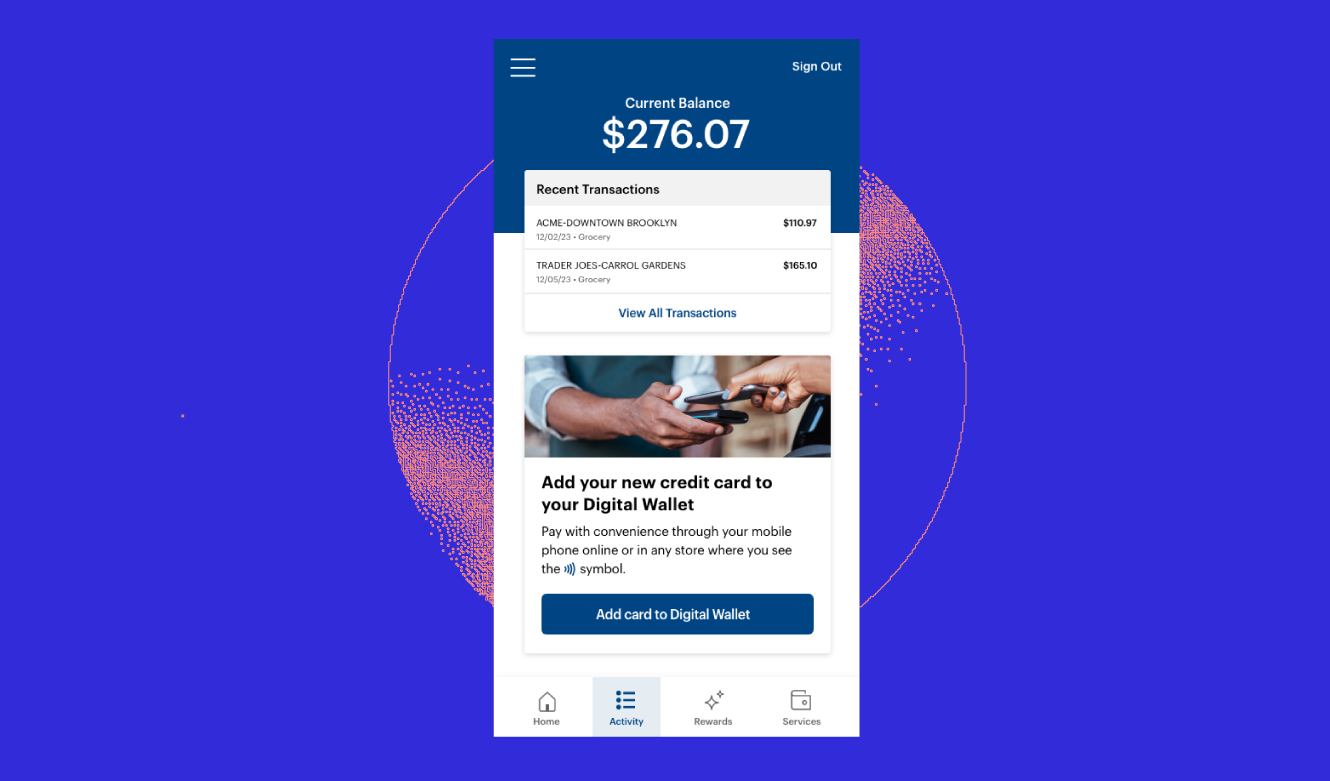

Ah, the coveted add-to-wallet. Beyond the triggered emails and push notifications briefly mentioned above, the post-login page is another great location for promoting this crucial step in the customer lifecycle. Following a recent first purchase by an individual who has not yet paid with their digital wallet, relevant messaging can be used here to highlight its benefits and convenience.

Spur digital engagement with push-to-wallet messaging during post-login experiences.

Further, once a card is added to the digital wallet, banks can provide customers with up-to-date information about the relevant rewards available to them, using spend data to promote curated offers in new categories, and even leverage countdown messages in email, mobile apps, or on their website to create urgency and spur action on applicable promotions.

From increased acquisition ROI to higher engagement, lower attrition rates, stronger customer loyalty and longevity, and greater top-of-wallet behavior, financial institutions stand to gain a lot from embedding personalization more deeply into their operations.

While there is greater demand for personalization within the industry, the path to an effective, individualized approach isn’t always clear, and many financial services brands still face challenges and lack the essential organizational and operational frameworks.

Rising consumer expectations, the proliferation of digital banking solutions, and the increased importance of brand loyalty are driving up customer acquisition costs and cementing “convenience” at the top of the customer experience food chain. For FIs who want to realize long-term, exponential revenue gains — the time for personalization within the financial services industry is now.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。