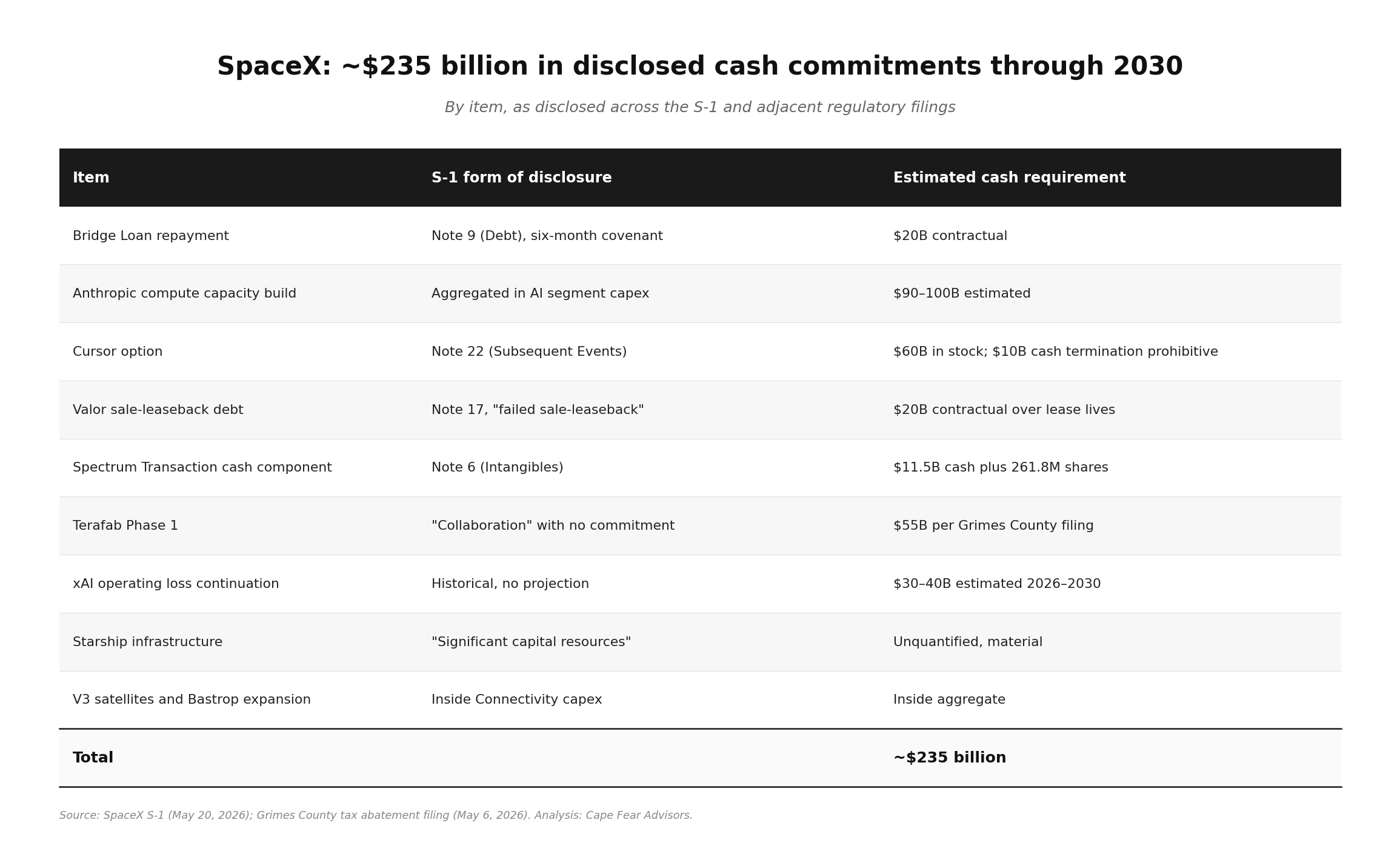

SpaceX disclosed, across the S-1 and adjacent regulatory filings, cash commitments of approximately $235 billion through 2030. The IPO will raise $50 to $75 billion gross. The first $20 billion is contractually committed to debt repayment within six months of closing. The gap is three to five times the raise on items disclosed in the document. Each commitment is correct within its own filing. None are aggregated. The set is not coherent. The question the S-1 does not answer, and that no single forward-looking section is required to address: where this amount of cash can be raised.

Six things came into focus since our May 10 piece on the cash gap:

The S-1 itself, filed May 20, with detailed segment reporting and forward commitment disclosures.

The IPO raise range: $50–75 billion gross. Valuation rumor at $1.75 trillion or above.

The Anthropic contract: $1.25 billion per month through May 2029, 90-day cancellable. $45 billion headline against capacity that does not yet exist.

The Bridge Loan terms: $20 billion at SOFR plus 0.75–1.75%, effective rate 4.58% as of March 31, 2026, executed March 2 to retire xAI and X debt at 9.5–12.5%. Covenanted to be repaid within six months of IPO proceeds receipt. Cost of the swap in Q1 2026: $1.163 billion in cash prepayment penalties and a $1.526 billion accounting loss on extinguishment.

The Cursor option mechanics: 30-day call window opening seven trading days after IPO completion or September 30, 2026, whichever is earlier. Exercise consideration $60 billion in Class A common stock per the disclosed terms. Termination consequence $1.5 billion termination fee plus $8.5 billion deferred services fee in cash.

The Grimes County tax abatement filing, May 6: Terafab Phase 1 at $55 billion, full buildout to $119 billion. Filed fourteen days before the S-1 disclosed no contractual Terafab commitment.

Putting every commitment in the same currency — necessary cash through 2030:

Total: approximately $235 billion in known cash and equity deployment through 2030.

The raise: $50–75 billion headline gross. After fees and Bridge Loan retirement, net usable in the $30–50 billion range.

The gap is 3 to 5 times the raise on these items alone.

Each item above is disclosed. None are aggregated. Each appears in a different section of the document, structured in a different form.

The Bridge Loan repayment is in the debt footnote. Use of Proceeds, where investors read about what the IPO funds, omits it. Investors reading only Use of Proceeds will not know that $20 billion is contractually committed to debt repayment within six months of closing.

The Anthropic contract is presented as forward revenue. The capex required to deliver the capacity Anthropic has purchased is folded into AI segment capex aggregated at $12.7 billion for 2025 and $7.7 billion for Q1 2026. Current COLOSSUS plus COLOSSUS II capacity is roughly 1.0 gigawatt total — supporting approximately 510,000 GPUs at 80 percent utilization. The S-1 says COLOSSUS II is being expanded to train Grok 5. Fulfilling Anthropic requires hundreds of thousands of additional GPUs of capacity, financed by capex the IPO is supposed to fund, against a contract Anthropic can cancel at 90 days.

The Cursor option is presented as an upside acquisition opportunity. The economic substance is something different. Exercise consideration is $60 billion in Class A common stock — equity dilution, not cash. Termination consequence is $10 billion in cash, payable as a $1.5 billion termination fee plus an $8.5 billion deferred services fee. Both outcomes are material. Whether the company can pay the termination amount in cash is the binding constraint that determines which outcome occurs.

Working from the March 31, 2026 balance sheet: $15.85 billion in cash plus $7.82 billion in marketable securities, against a $20 billion Bridge Loan repayment due within six months of IPO proceeds receipt, plus an $11.5 billion Spectrum cash component closing November 2027, plus Valor lease payments at approximately $3.4 billion per year, against a Q1 2026 free cash flow run rate of negative $36 billion per year. The $10 billion termination fee, added on top, is not comfortably payable in cash.

Which means the exercise decision is effectively pre-determined by cash constraint, not strategic merit. The 30-day call window opens seven trading days after IPO closing, expiring no later than the end of October 2026. Exclusivity prevents Cursor from accepting competing bids during the window, so SpaceX faces no competitive pricing pressure. Exercising in stock uses the newly-IPO’d equity currency at the IPO’s establishing valuation; declining requires paying $10 billion in cash the balance sheet does not comfortably support. The architecture makes the stock exercise the rational outcome on cash-constraint grounds, regardless of how the Cursor acquisition itself is judged on strategic grounds. The option, structurally, is a forcing function for the first major deployment of the IPO equity, on a schedule that ensures the acquisition prices at the IPO’s establishing valuation before the market has time to test the valuation against operating performance.

The Valor sale-leaseback is filed under the technical accounting classification “failed sale-leaseback.” The substance is $20 billion of related-party debt financing from the CEO of a private equity firm who sits on the SpaceX board. The classification does the work of describing related-party debt in the language of an accounting technicality.

The Spectrum Transaction is presented as an intangible asset acquisition for $19.6 billion, of which $11.5 billion is cash (debt payoff plus loans to EchoStar’s trust through November 2028). The equity consideration of 261.8 million Class A shares at a fixed $42.40 per share post-split price was set in November 2025; at the rumored $1.75 trillion valuation, EchoStar receives a markup on the equity consideration on top of the cash. The capex to deploy the spectrum into a revenue-generating network is folded into Connectivity segment capex.

Terafab is a “collaboration” with Tesla. The S-1 states “neither Tesla nor Intel are obligated to remain a part of the project, and we may not enter into any such definitive agreements.” The same project was filed with Grimes County two weeks earlier at $55 billion Phase 1, scaling to $119 billion. Same project, same officer, same fourteen-day window. The tax abatement filing represents the maximum credible project budget because the abatement scales with budget. The S-1 represents only what is contractually committed because forward capex commitments scale negatively against cash available for disclosed growth uses. Both filings are correct within their incentives. The set is not coherent.

The xAI operating losses are disclosed historically by segment. The forward projection of when those losses close, and the capex required to build the revenue that would close them, is not separately stated.

In substance, the Risk Factors section says:

Capital requirements are significant and ongoing.

The company may not be able to raise sufficient additional capital.

Cash flow has been and will likely remain negative.

Funding depends on continued access to capital markets.

These are qualitative warnings. They are not quantified against the commitments above. Investors are told cash needs are large, funding is uncertain, and operations are cash-flow negative. They are not told that aggregate cash deployment required to fulfill the disclosed operational commitments is approximately $235 billion against a $50–75 billion raise.

The aggregate is in the risk section as a warning. The aggregate is not in the financial sections as a number.

The company also discloses additional unquantified exposures that sit on top of the table above:

A $399 million litigation accrual at March 31, 2026, with the company stating reasonable possibility of additional material losses that are not currently estimable.

The Vidstream patent verdict, $105 million in damages plus $67 million in prejudgment interest, on appeal at the Federal Circuit.

The Pampena v. Musk partial judgment, entered April 3, 2026, against Mr. Musk in his personal capacity on Section 10(b) violations connected to his 2022 Twitter purchase statements. The company discloses this in its own management section as a risk to the company.

The Grok image-generation lawsuit cluster, including the Mayor and City Council of Baltimore complaint filed March 24, 2026, seeking statutory penalties and injunctive relief — claims not quantified.

The European Commission Digital Services Act fine of €120 million, challenged February 16, 2026 in the General Court of the European Union — challenge pending.

The NAACP Clean Air Act challenge to COLOSSUS II turbines, filed April 14, 2026, with a preliminary injunction motion seeking to enjoin operation.

Indemnification obligations to directors, officers, and contractual counterparties, which the S-1 states “may not be subject to maximum loss clauses” and for which the company “has not accrued a liability.”

These exposures are disclosed qualitatively. None are aggregated. None are quantified against the cash bridge. The S-1 states the company believes there is a reasonable possibility it may incur material losses that exceed its estimates. Translated back to cash, these are additional draws against the same constrained pool.

It is disclosed three ways simultaneously:

In the financial statements, as historical results and committed obligations, item by item, in different notes.

In the operational claims, as forward intentions whose capex implications are aggregated or unstated.

In the risk factors, as qualitative warnings that capital needs are large, funding is uncertain, and litigation exposures may exceed estimates.

Putting it all back in the same currency, the three combine: approximately $235 billion in known forward commitments, plus the company’s disclosed additional unquantified exposures, against a $50–75 billion gross raise, against $6–7 billion per year of operating cash flow, against –$36 billion per year of free cash flow run rate. The S-1 contains every input. The S-1 does not perform the calculation.

One pathway is the Tesla acquisition, speculated by Bloomberg, ION Analytics, Walter Isaacson, and the prediction markets, and structurally available given Mr. Musk’s roles at both companies, Tesla’s cash position, and the cross-shareholder mechanics already in place. Even if completed at scale, a Tesla absorption closes a fraction of the gap — Tesla’s approximately $45 billion of cash plus incremental debt capacity addresses a portion of the deployment, not all of it. The S-1 does not address the pathway in any forward-looking section.

A federal commitment pathway would require disclosed CHIPS Act expectations for Terafab and disclosed government contract commitments at TAM scale. Neither is in the document. Customer A (the U.S. government) is 20.9 percent of 2025 consolidated revenue, declining as a percentage from 25.2 percent in 2023.

A subsequent equity issuance pathway is the implicit mechanism: the IPO establishes the currency, the currency funds the gap through additional offerings, strategic transactions priced in the equity, and continued related-party financing. The Cursor mechanism described above is the first scheduled instance of this pathway: convert IPO equity to a strategic acquisition before the market tests the establishing valuation, on a timeline the option mechanics determine. The architecture does not require the company to perform this conversion. The architecture does require the company to pay $10 billion in cash if it does not. Given the balance sheet, the conversion is the cash-conserving outcome.

A continued private capital pathway — Valor leases extending, additional related-party financing, additional sale-leaseback structures — would scale the related-party debt from $20 billion to materially larger figures and would compound the governance asymmetries the controlled-company structure already permits.

Each pathway closes a fraction. None alone closes the gap. The question the S-1 does not answer, and that no single forward-looking section is required to address: where this amount of cash, on the timeline the operational commitments require, can be raised.

This piece continues the analytical work in Adding It Up — The $165 Billion Cash Gap (May 10, 2026), which established the common-currency translation method and identified the eight S-1 disclosure questions this update revisits against the document the company filed on May 20.