👋 Welcome to Climate Drift: your cheat-sheet to climate. Each edition breaks down real solutions, hard numbers, and career moves for operators, founders, and investors who want impact. For more: Community | Accelerator | Open Climate Firesides | Deep Dives

Hey there! 👋

Skander here.

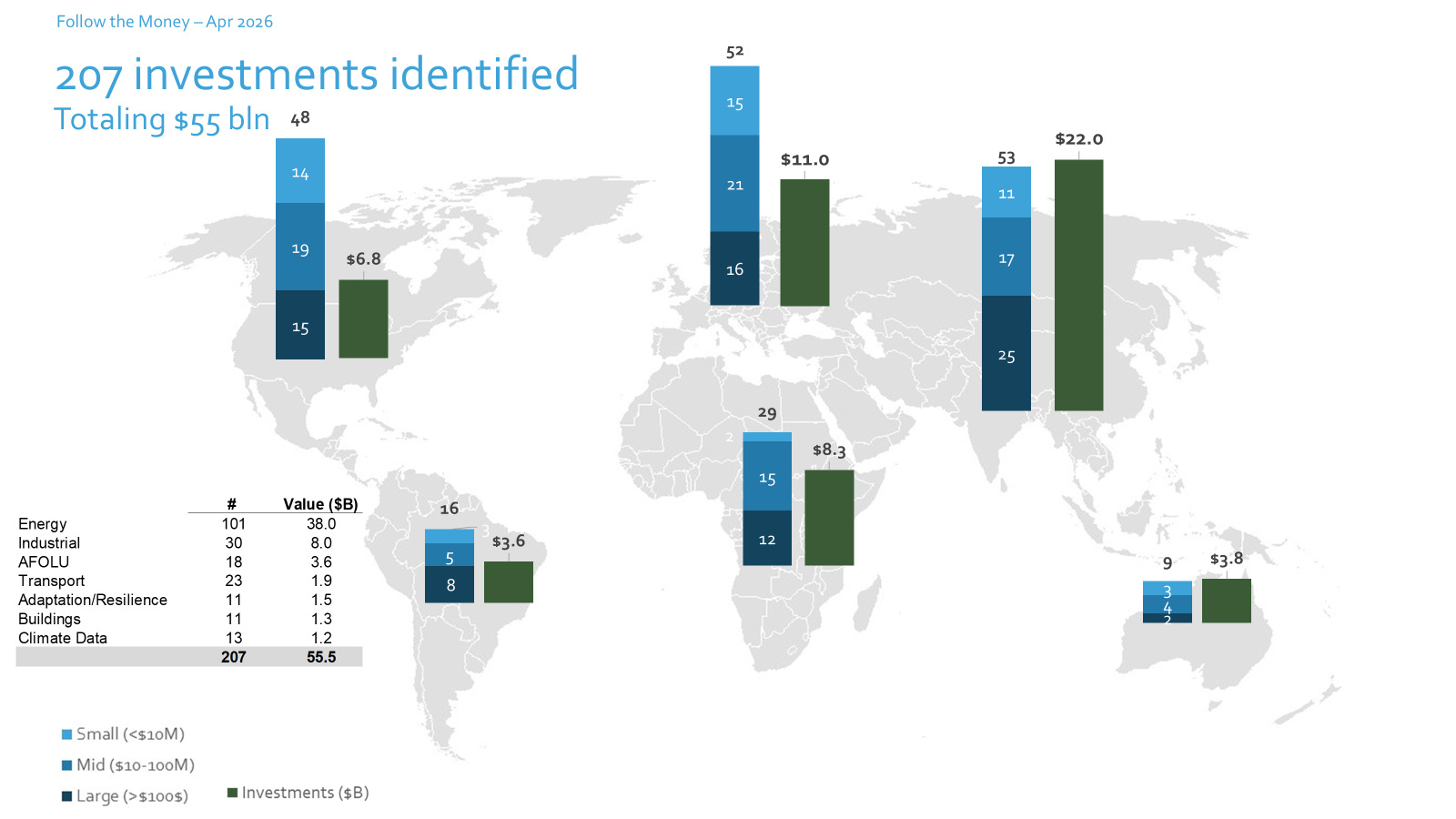

$55 billion across 207 deals. April 2026 reset the ceiling. It more than doubled March’s record and became the biggest month we’ve ever tracked.

Jarek’s latest Follow the Money breaks down where the capital actually went, and the regional splits tell you more than any macro forecast could.

🇺🇸 North America: $6.8B across 48 deals, fewer dollars than Asia or Europe but the sharpest thematic concentration of the month. The U.S. kept buying firm, dispatchable power and hard-to-abate decarbonization. X-energy priced a $1B Nasdaq IPO above range (the first large advanced-nuclear listing of the cycle), Blue Energy raised $380M for prefabricated reactors, and DOE retained $1.2B for direct-air-capture hubs.

🇪🇺 Europe: $11B across 52 deals, blending one giant public-finance package (the $2.3B EIB Clean Energy approval) with one of the deepest mid-stage deep tech layers anywhere. Green steel (Stegra, $1.65B), superconducting cable (Subra), organic flow batteries (CMBlu crossing unicorn), projectile fusion (First Light). First-of-a-kind closes, one after another.

🌏 Asia: $22B across 53 deals, nearly half the month’s global total. China anchored the mega-rounds (CATL’s $5B placement, plus humanoid robotics rounds from X Square, Pudu, and Booster), while India filled the renewables, hydropower, and EV long tail. Single Asian infrastructure deals routinely exceeded entire regional totals elsewhere.

🌍 Rest of World: $15.7B across 54 deals. Africa had an exceptional month at $8.3B, led by Egypt’s $5B Amun green ammonia pledge. Brazil’s BTG Pactual closed the largest reforestation fund to date at $1.24B, the first project globally to issue credits under Verra’s new VM0047 methodology.

A few patterns worth flagging: solar-plus-storage hybrids pulled $9.2B versus $2.9B into pure solar PV, so standalone solar is now the exception. AI-enabled climate solutions showed up in 11 separate raises. Public markets reopened as a growth channel, with X-energy and Sigenergy (which doubled on debut) leading a thick pre-IPO pipeline.

🌊 Jarek breaks it all down below, region by region, theme by theme.

But first: Who is Jarek?

Jarek Dmowski is a global transformation leader who partners with high-growth companies with positive climate impact. He combines industry and climate finance expertise with a strong track record of driving growth—across PE/VC-backed scaleups, ABN AMRO, and BCG.

He scaled a data-driven technology company ~2.5x to ~$25M in revenue and led post-merger integrations that enabled ~6x accelerated growth. At a global financial institution, he spearheaded a $2B capital reallocation toward new energy and mobility. He also developed a comprehensive climate plan that translated the Paris Agreement into actionable targets across sectors and established a $250M program to drive efficiency gains and reduce emissions at an energy utility.

Jarek is passionate about how the climate transition reshapes economies and business models, creating significant opportunities for multi-country growth and impact.

Welcome to the next edition of “Follow the Money” - a monthly briefing on the capital flows shaping the climate transition.

$55B in April. April did not just continue the year’s momentum; it reset the ceiling. We tracked 207 climate-related investment deals totaling ~$55 billion - the highest monthly volume we have recorded, surpassing March’s previous record of $22B.

America is buying atoms while the rest of the world buys electrons. A $5B green ammonia mega-pledge in Egypt, the largest reforestation fund ever closed, and signs that China’s humanoid robotics sector is moving from labs into manufacturing. Public markets are reopening as a growth-capital channel for climate companies. Sovereigns and DFIs are writing large checks for adaptation and infrastructure. Asia’s utility-scale build-out is accelerating at unprecedented scale. And in the West, a deep and increasingly specialized layer of climate deep tech is finally reaching commercial scale. Let’s dive deeper.

Explanation of the approach and source data: The investment list was developed based on disclosures, newsletter monitoring and review of climate news. Although not exhaustive, 207 climate-related investment deals were tracked - amounting to roughly $55 billion (all data in US$), covering all continents and different life stages of companies and development finance programs. Data skew toward early-stage companies and investments, as well as development financing programs. We are continuously working to expand the data sources and coverage of investments.

So, where did the money flow in April 2026?

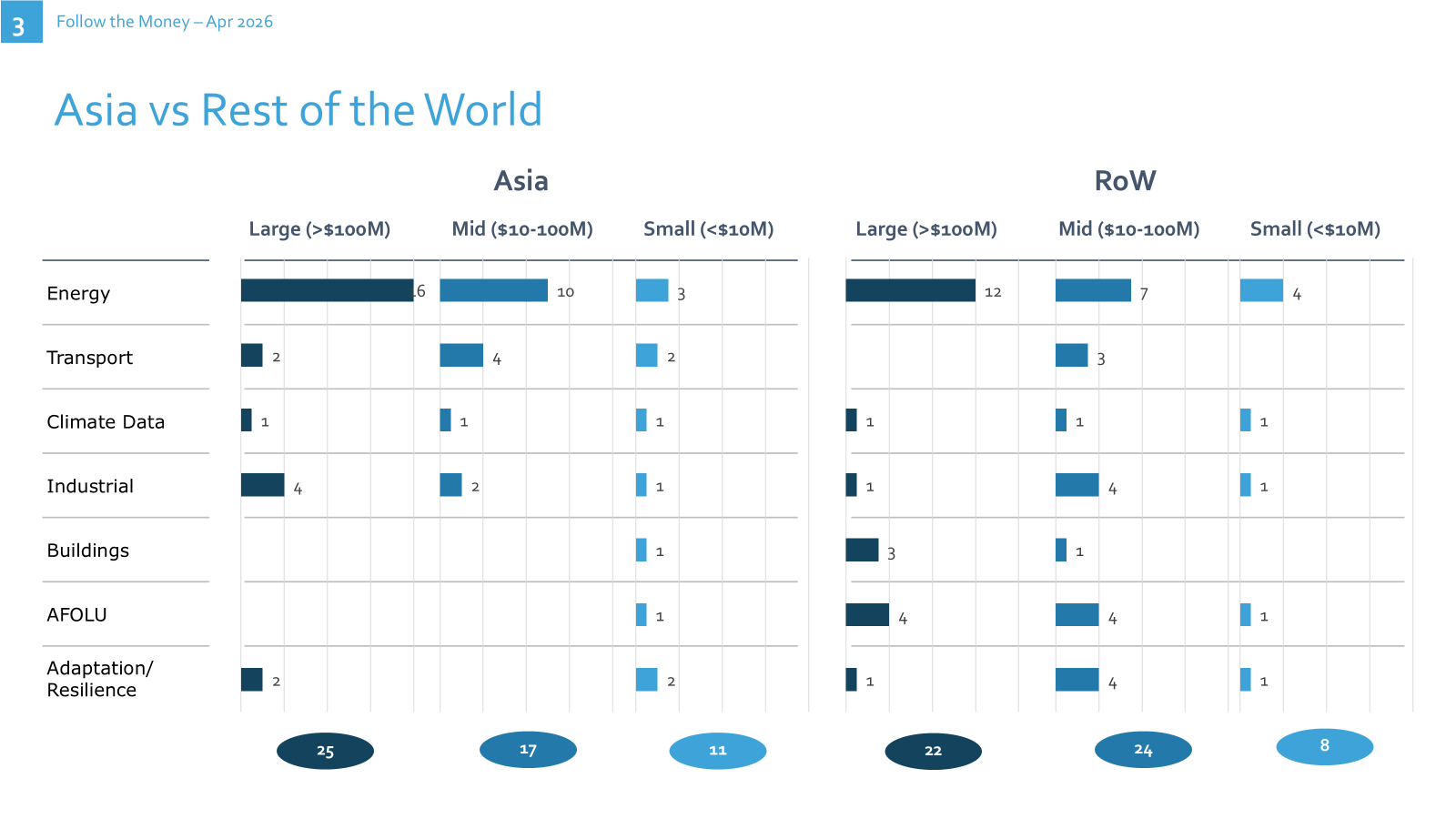

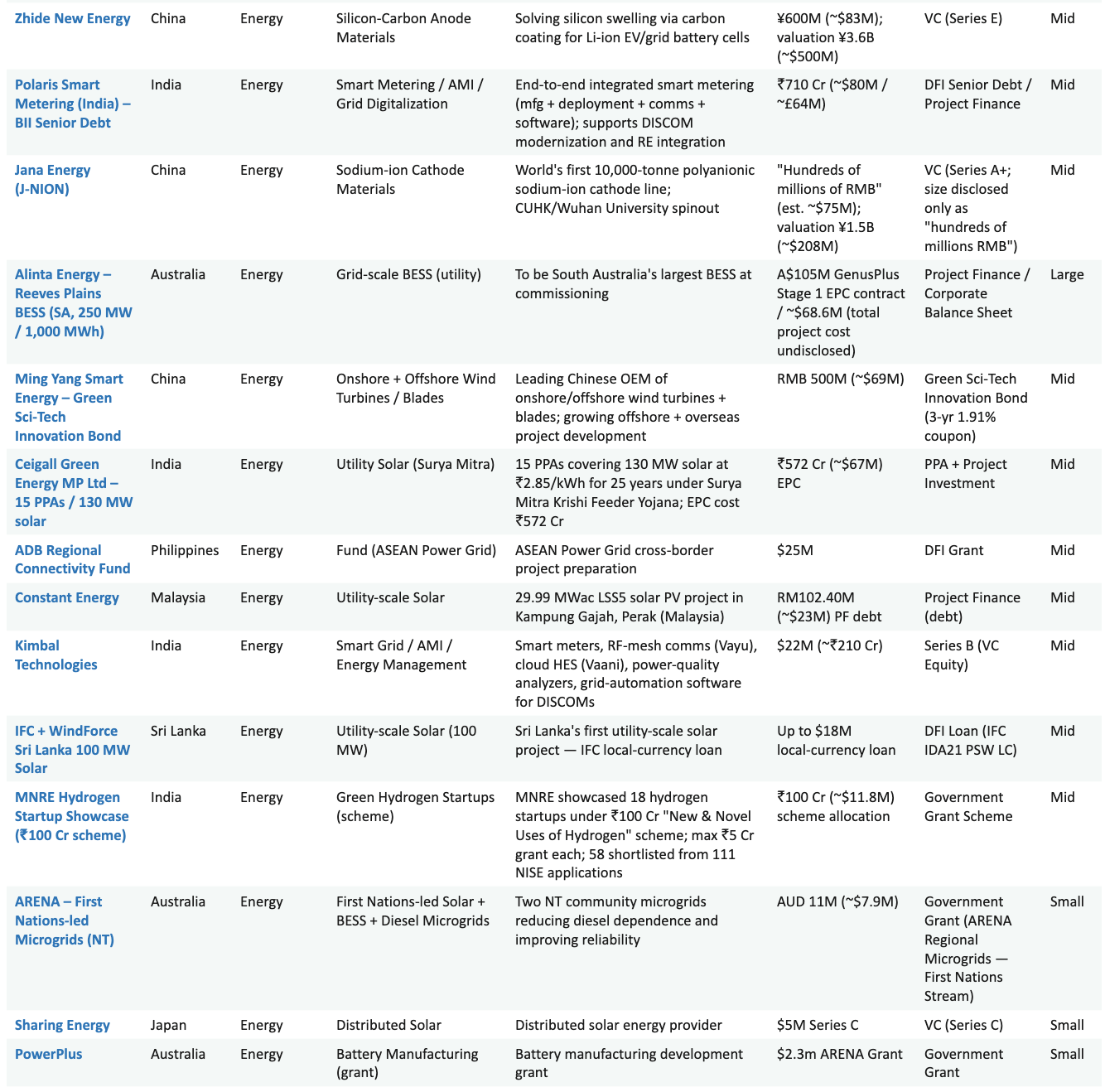

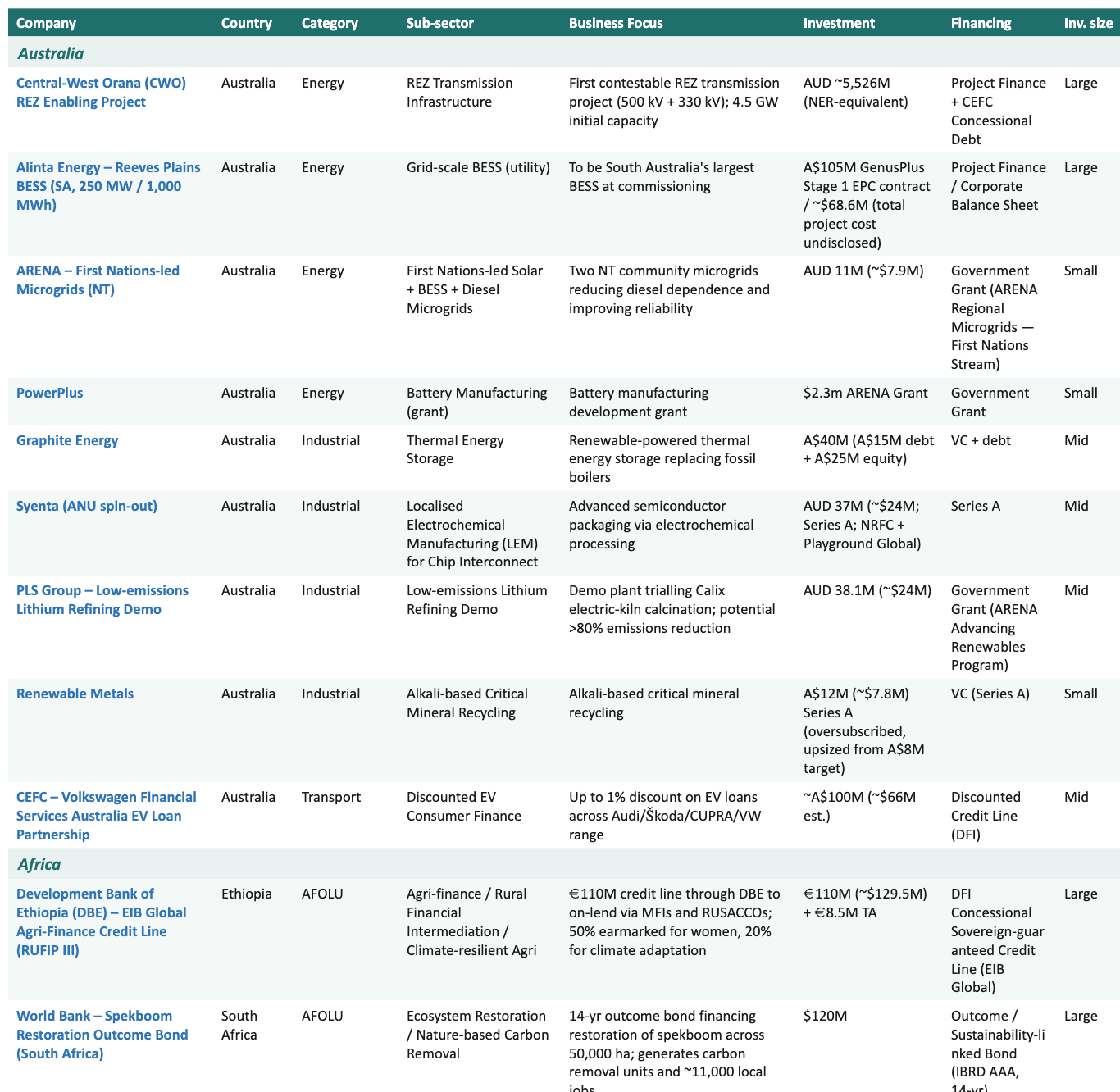

Asia-Pacific led decisively with ~$22B across 53 deals, followed by Europe (~$11B, 52 deals), Africa (~$8.3B, 29 deals), North America (~$6.8B, 48 deals) and Latin America (~$3.6B, 16 deals). Africa’s jump reflects both deeper coverage and a genuinely exceptional month of sovereign and DFI activity.

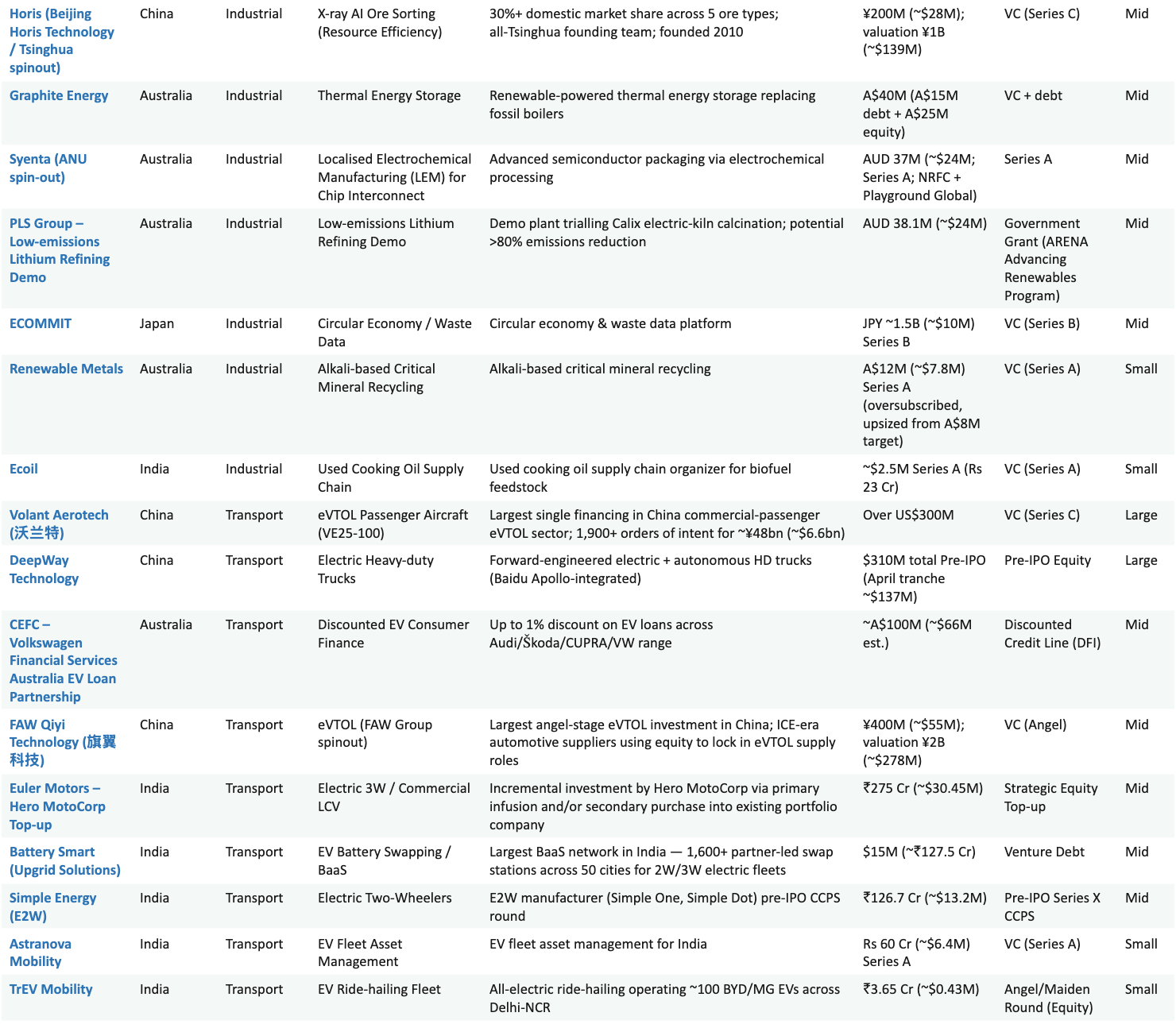

Energy once again dominated, accounting for ~$38B across 101 deals - by far the largest category, month after month. Industrial was a clear #2 (~$8B, 30 deals), followed by AFOLU (~$3.6B), Transport (~$1.9B), Adaptation & Resilience (~$1.5B), Buildings (~$1.3B) and Climate Data (~$1.2B). Buildings remained structurally undercapitalized relative to their emissions share - a persistent gap.

AI’s influence is becoming structural. Roughly 11 AI-enabled climate solutions raised capital in April - from grid intelligence (Verda, WorkOnGrid) to wildfire detection (Satellites on Fire) and food-system optimization (Afresh) - reinforcing AI as an accelerator of deployment, optimization and cost reduction across sectors.

AI’s influence is becoming structural. Roughly 11 AI-enabled climate solutions raised capital in April - from grid intelligence (Verda, WorkOnGrid) to wildfire detection (Satellites on Fire) and food-system optimization (Afresh) - reinforcing AI as an accelerator of deployment, optimization and cost reduction across sectors.

Robotics continued as a tracked category, with humanoid and embodied-AI rounds concentrated in China (X Square Robot $276M, Pudu $150M, Booster $137M) and a notable European cluster in autonomous monitoring (Kelluu, Bubble Robotics, Nature Robots).

Public and development finance anchored the market at scale. Multilateral institutions and government programs supported ~$16B across over 60 deals, with a heavy tilt toward infrastructure, adaptation and on-lending facilities.

Let’s now dive deeper into 2026 watchlist themes (please refer to our December perspective for more details) and across regions to highlight technologies with real scaling potential over the next 3-5 years.

Which (of our 2026) themes were most strongly visible in April?

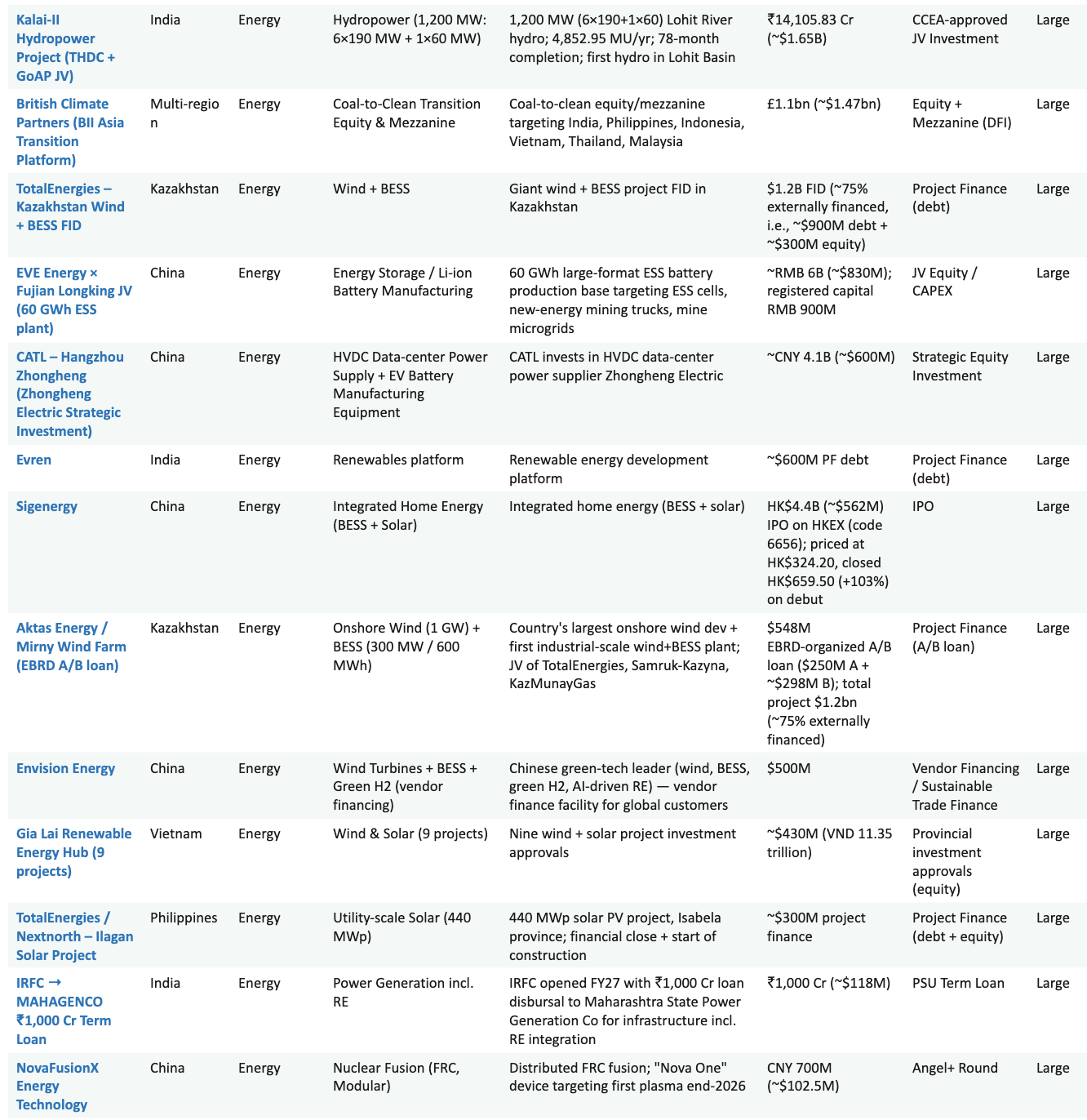

The divergence we have tracked since December hardened in April. In North America, capital concentrated in dispatchable, capital-heavy power for the AI build-out: X-energy priced its Nasdaq IPO above range at $23/share for ~$1B gross (its Xe-100 SMR and TRISO-X fuel platform now public-market funded), Blue Energy raised a $380M Series A for prefabricated reactors targeting data-center offtake, and geothermal developers Zanskar and TerraSpark added new funding. China’s closest comparable bet was NovaFusionX’s $102.5M fusion round - notable, but still fusion rather than deployable fission.

By contrast, Europe, Asia, Africa and Latin America deployed capital into proven, scalable infrastructure - solar, wind, storage and hydro - often at single-deal sizes that dwarf U.S. equity rounds. The clearest signal is that standalone solar is becoming the exception: in April, we tracked roughly $9.2B into solar-plus-storage hybrids versus ~$2.9B into pure solar PV. From Elgin Energy in the UK and Globeleq in Zambia to TotalEnergies × Masdar’s $2.2B solar-wind-BESS platform. The economics now favor pairing almost everywhere: co-locating batteries lets developers firm intermittent output, capture price spreads, and defer grid-interconnection bottlenecks - turning “cheap intermittent electrons” into dispatchable, gridable capacity.

The “cheap batteries + localized electrification” thesis kept widening across air, rail, road and water. The headline was Sigenergy (China), whose HK$4.4B (~$562M) Hong Kong IPO priced at HK$324.20 and closed up ~103% on debut - its SigenStor 5-in-1 PV+BESS+EV-charging system already holds ~28.6% of the global stackable distributed solar-storage market.

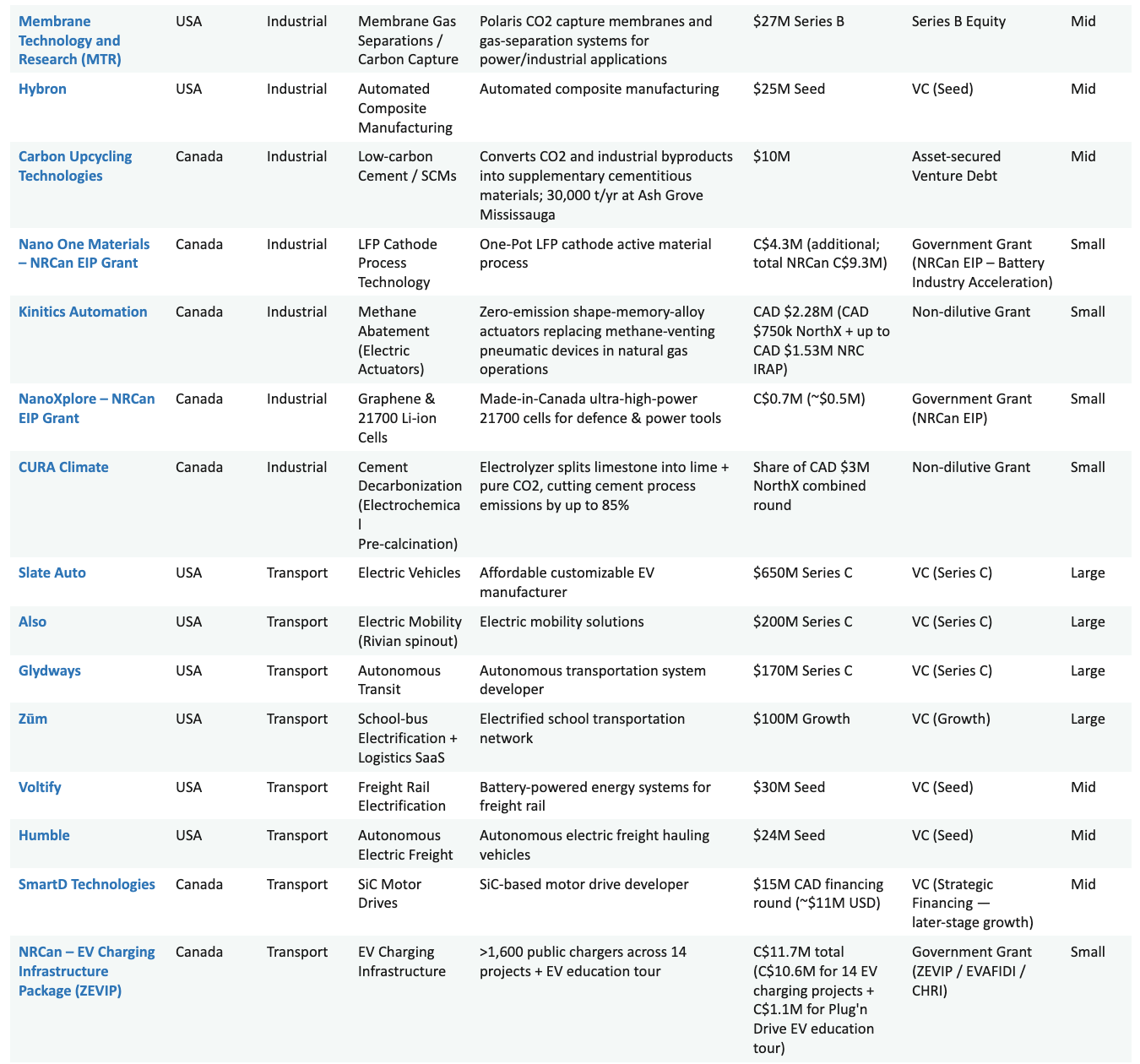

Road mobility was the deepest layer: Slate Auto (USA, $650M Series C, Bezos-backed) on an affordable customizable EV pickup; Also (USA, $200M, a Rivian spinout) on small EVs with DoorDash; Zūm (USA, $100M, $1.7B valuation) electrifying school transport; DeepWay (China, $137M) and Humble (USA, $24M) on electric/autonomous heavy freight; and a dense Indian and African layer - Simple Energy, Astranova Mobility, TrEV Mobility and Ethiopia’s Dodai (e-motorbikes).

The supporting infrastructure scaled too: robotic and ops-layer charging from ROCSYS (Netherlands, $13M) and &Charge (Germany, €5M), plus drivetrain enablers SmartD Technologies (Canada, SiC motor drives) and Ayr Energy (USA, grid transformers). Beyond the road, electrification reached new modes: Volant Aerotech (China, >$300M) and FAW Qiyi (China, ~$55M) on passenger eVTOL, and Voltify (USA, $30M) on battery-electric freight rail. Different markets, same physics: localized, electrified, battery-led.

The month’s defining lesson was structural: the companies clearing the “valley of death” are the ones engineering blended capital stacks, not chasing a single instrument. Stegra (Sweden, formerly H2 Green Steel) reached an agreement in principle on a €1.4B (~$1.65B) equity-led mixed round - Wallenberg Investments forming a new lead consortium with Temasek and IMAS - to push its 740 MW green-hydrogen DRI steel plant through to operation. Sedron Technologies (USA) secured up to $500M of staged growth equity from Ara Partners to scale its Varcor biosolids/manure-upcycling system. And on the venture-debt end, CMBlu Energy (Germany) crossed the unicorn line with a €50M Series C first close (Samsung Ventures joining) for non-lithium organic flow batteries backed by a 5 GWh Uniper framework.

Robotics is now a permanent fixture in the climate-capital map, with a clear geographic division of labor. China led the embodied-AI mega-rounds: X Square Robot (~$276M Series B, Xiaomi and HongShan co-leading, cumulative funding >$400M), Pudu Robotics ($150M, service and commercial robots) and Booster Robotics ($137M, humanoids). Europe owned the direct, in-the-field niche: Kelluu’s monitoring airships, Bubble Robotics (Switzerland, $5M, autonomous ocean monitoring), Nature Robots (Germany, $5M, precision-ag autonomy) and All3 (Switzerland, $25M, robotics+AI for construction productivity).

IPOs - Public Markets Reopen as a Climate Growth Channel: One of the clearest shifts in April was the return of the public market as a climate-growth instrument. X-energy priced a ~$1.0B Nasdaq IPO (XE) above its range and opened +31% - the first large advanced-nuclear listing of the cycle. In Hong Kong, Sigenergy’s ~$562M HKEX IPO more than doubled on its debut (+103%), with cornerstone investors including Temasek and Hillhouse. CATL tapped the H-share market for a ~$5.0B secondary offering to fund battery-capacity expansion. Behind the listed names, a thick pre-IPO pipeline formed: Spacety (~$190M, SAR satellites) and Chang Guang Satellite (~$70M, optical EO) prepared STAR Market filings; DeepWay ($137M tranche) and Pudu Robotics ($150M) raised ahead of HKEX listings; and India’s Simple Energy ($13.2M CCPS) lined up a pre-IPO round. The message: for capital-heavy climate hardware that has reached commercial traction, the exit window is open again.

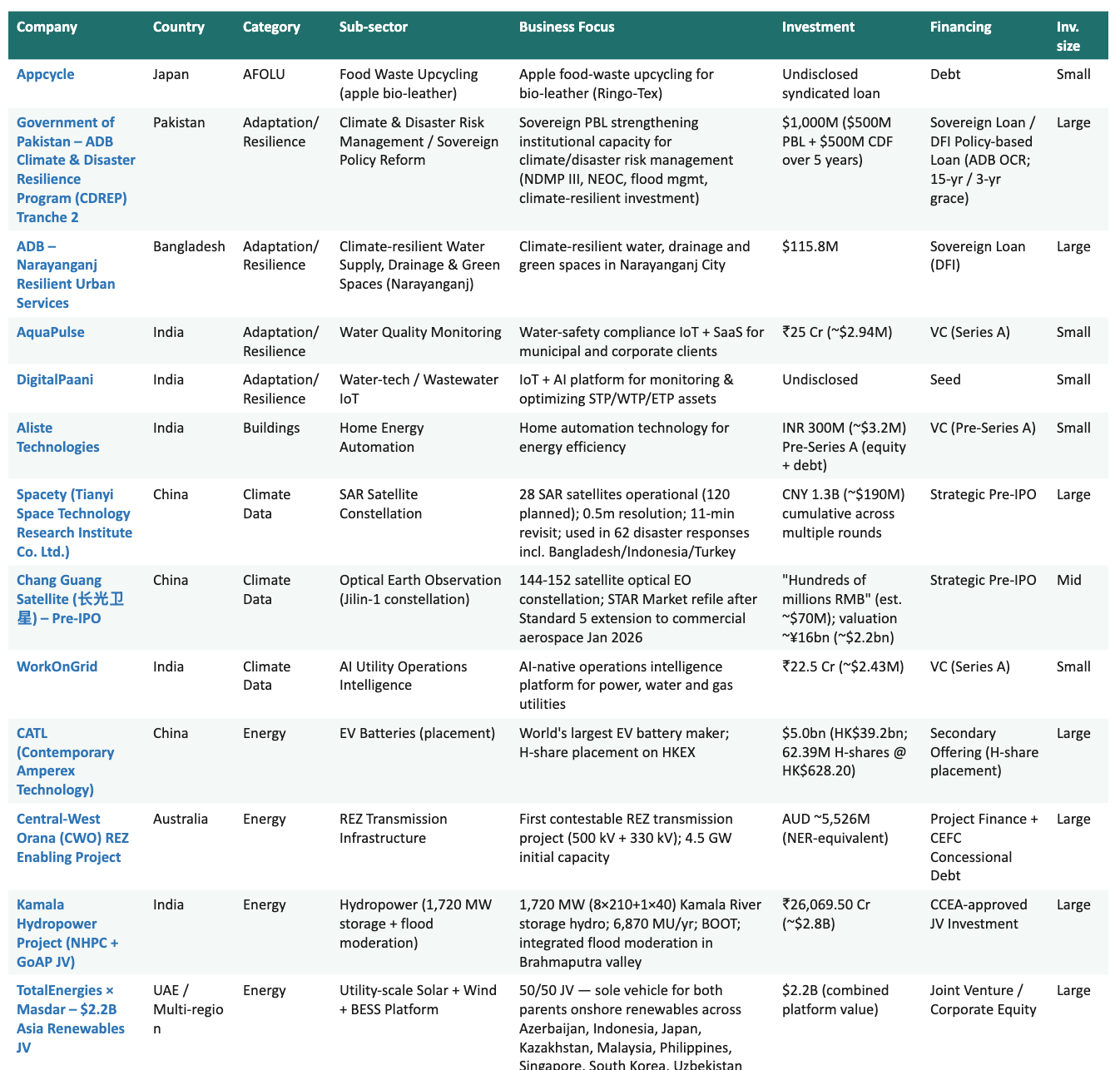

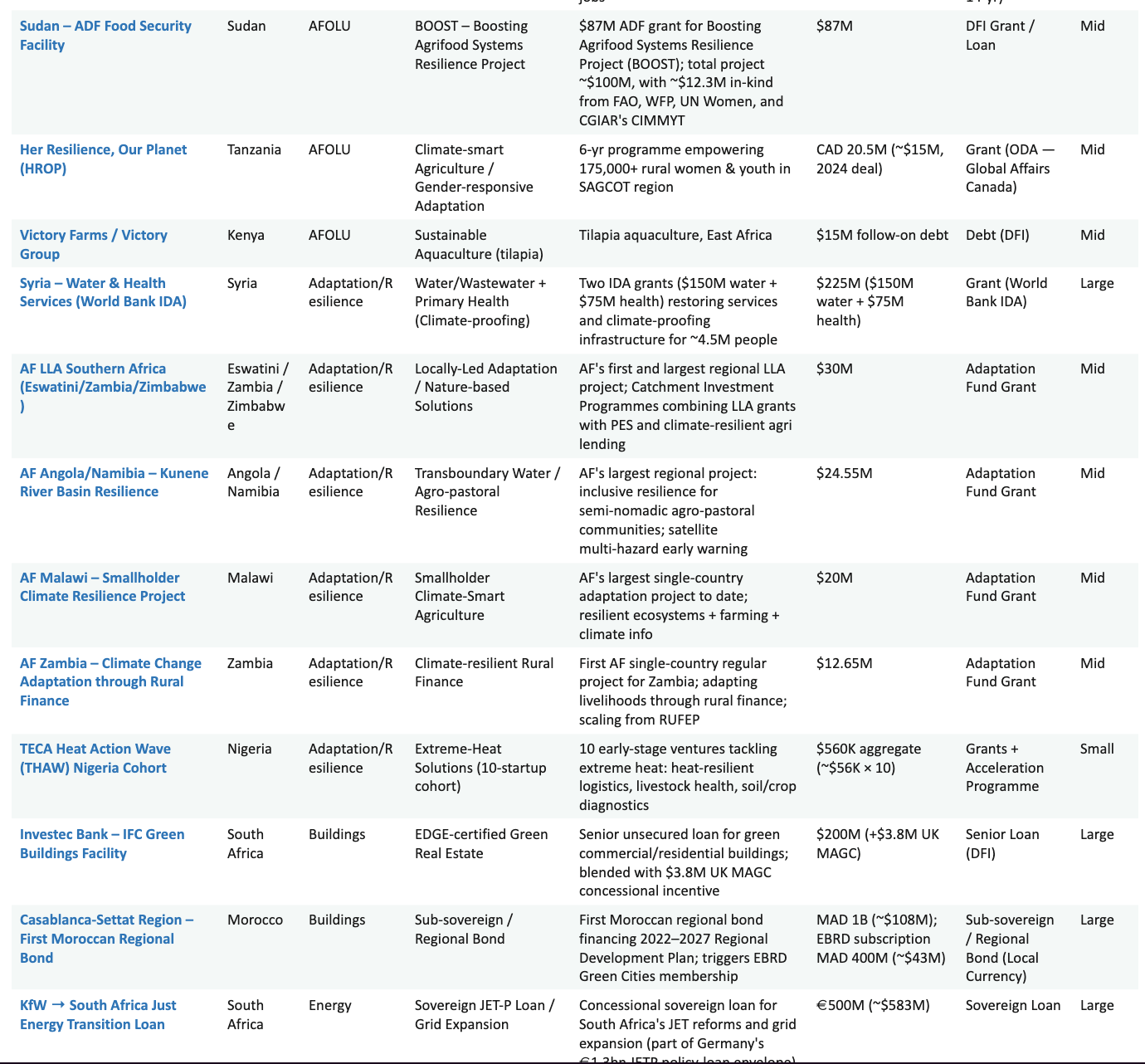

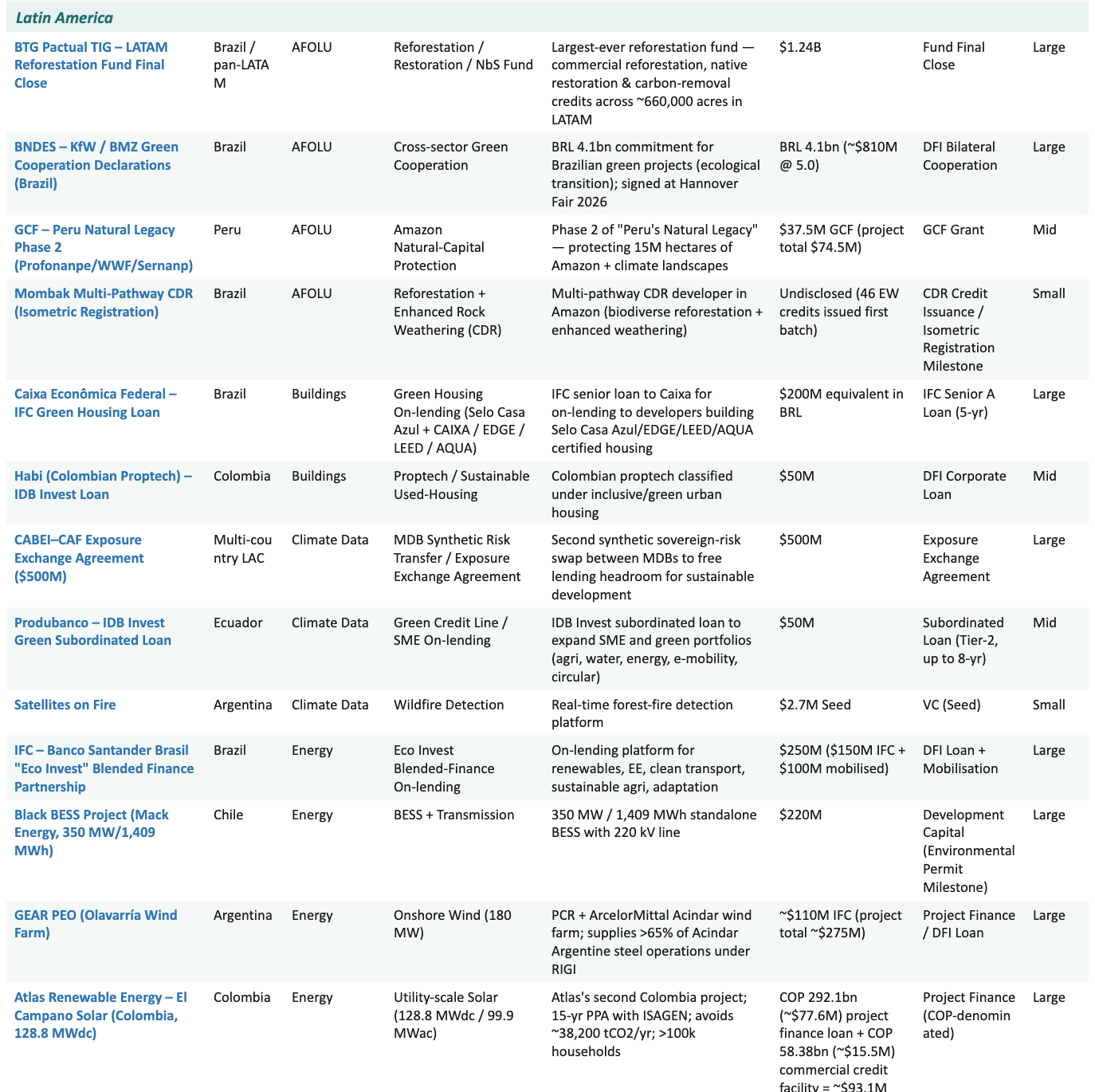

Nature Based Solutions: Nature had its strongest month on record. BTG Pactual Timberland Investment Group held the final close of the largest reforestation fund to date at $1.24B, targeting ~660,000 acres across Latin America - and its Brazil Cerrado 1 project was the first globally to issue credits under Verra’s VM0047 ARR methodology. The World Bank priced a $120M, 14-year Spekboom Restoration Outcome Bond in South Africa, while Living Carbon × Octopus ($513M) and Brazil’s BNDES–KfW/BMZ green declarations (~$810M) added scale.

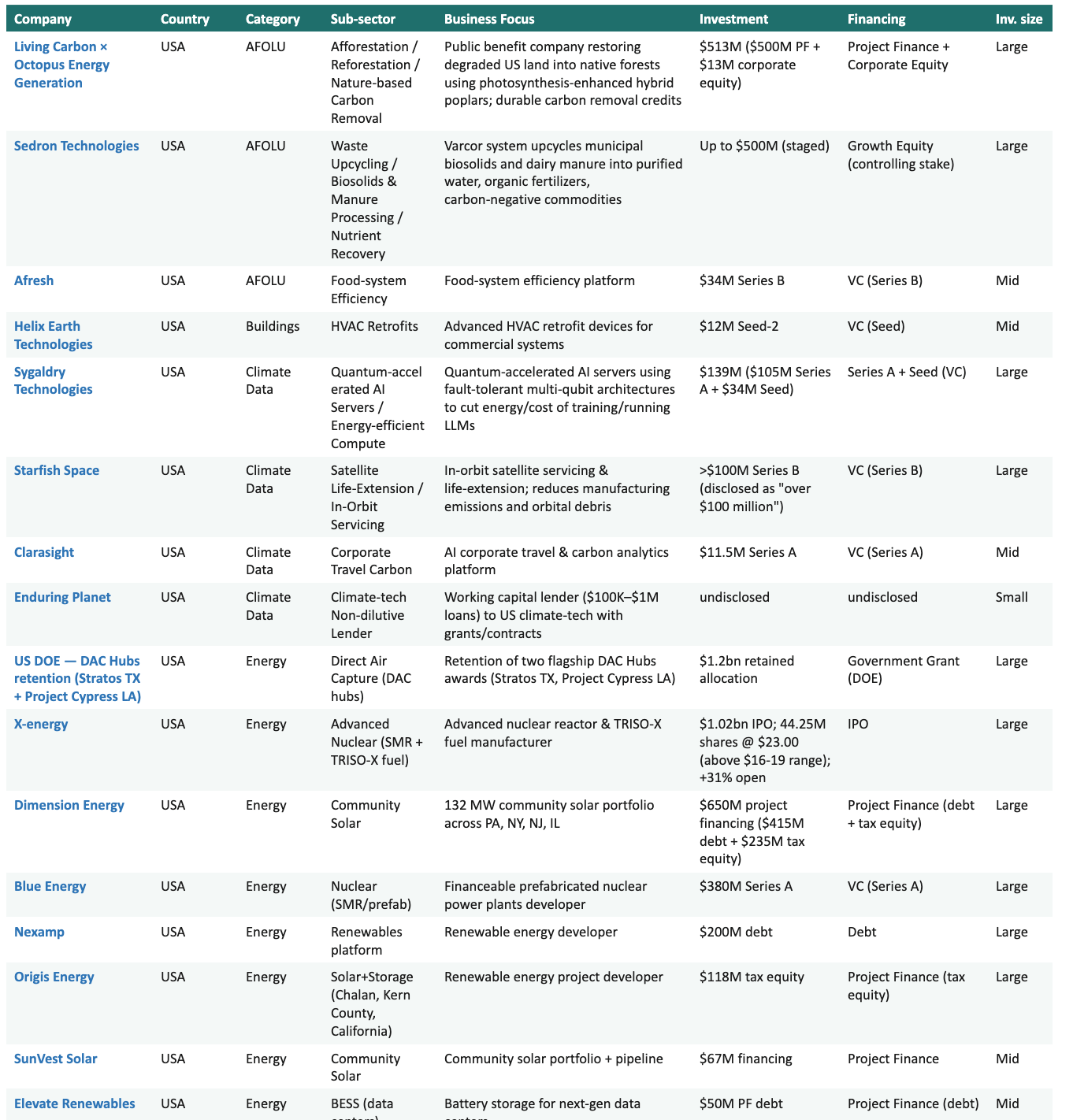

Biogas & Biomethane: The Quiet Workhorse of Hard-to-Abate: Biogas rarely makes headlines, but April showed it doing real work. GMT (UK) raised the category’s largest cheque - a ~$248M project-finance facility for biomethane. In Brazil, Tropical Bioás Edéia (bp bioenergy, ~$52M) produces biomethane from sugarcane vinasse, and the São Paulo Green Corridor / TransJordano project (~$28M) builds a refuelling corridor for heavy trucks. At the frontier, Hydron Energy (Canada) won non-dilutive NRC IRAP backing for single-step landfill-gas-to-RNG upgrading, and Nirova (USA, ~$3M) advanced anaerobic digestion.

Climate Observation & Data: A Cluster of Financings: As climate volatility rises, the businesses that own the data layer are attracting real capital. The standout was Xoople (Spain, $130M Series B). Around it: Sygaldry Technologies (USA, $139M, energy-efficient AI servers); Starfish Space (USA, >$100M, in-orbit life-extension); China’s Spacety (~$190M SAR) and Chang Guang (~$70M optical); Kelluu (Finland) and Bubble Robotics (Switzerland) on airborne and underwater monitoring; WorkOnGrid (India, ~$2.4M); Clarasight (USA, $11.5M); and Satellites on Fire (Argentina, $2.7M).

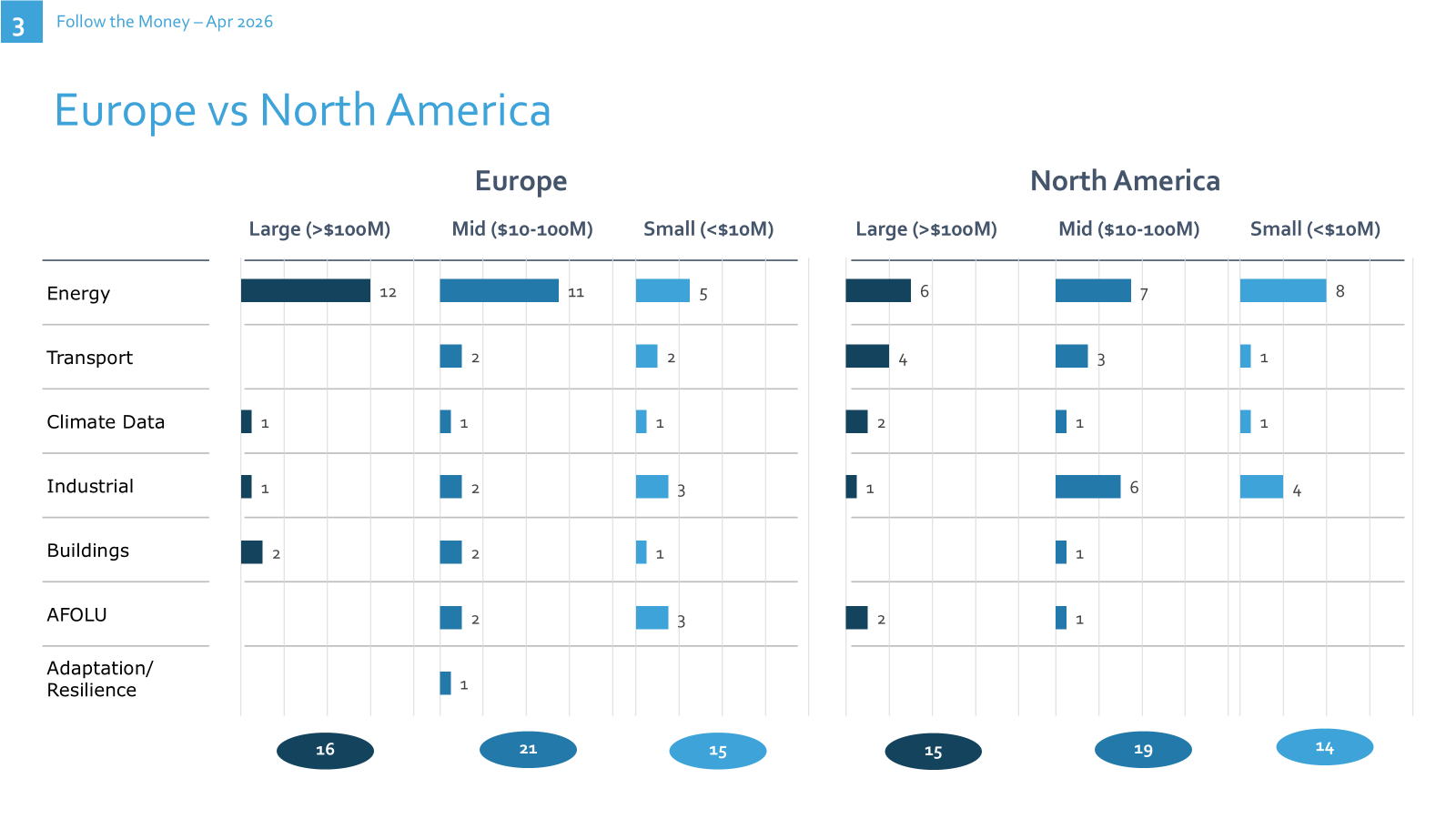

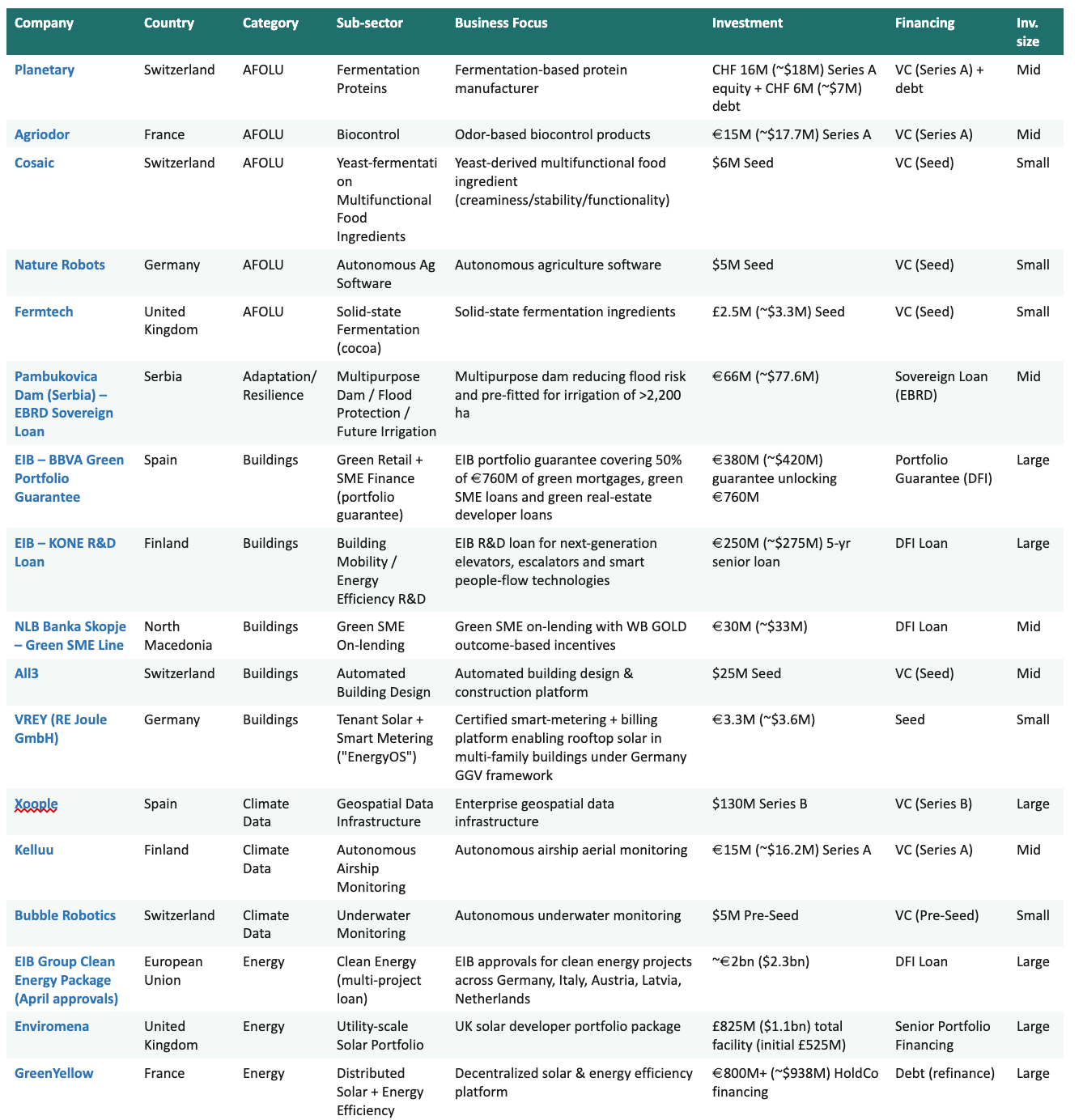

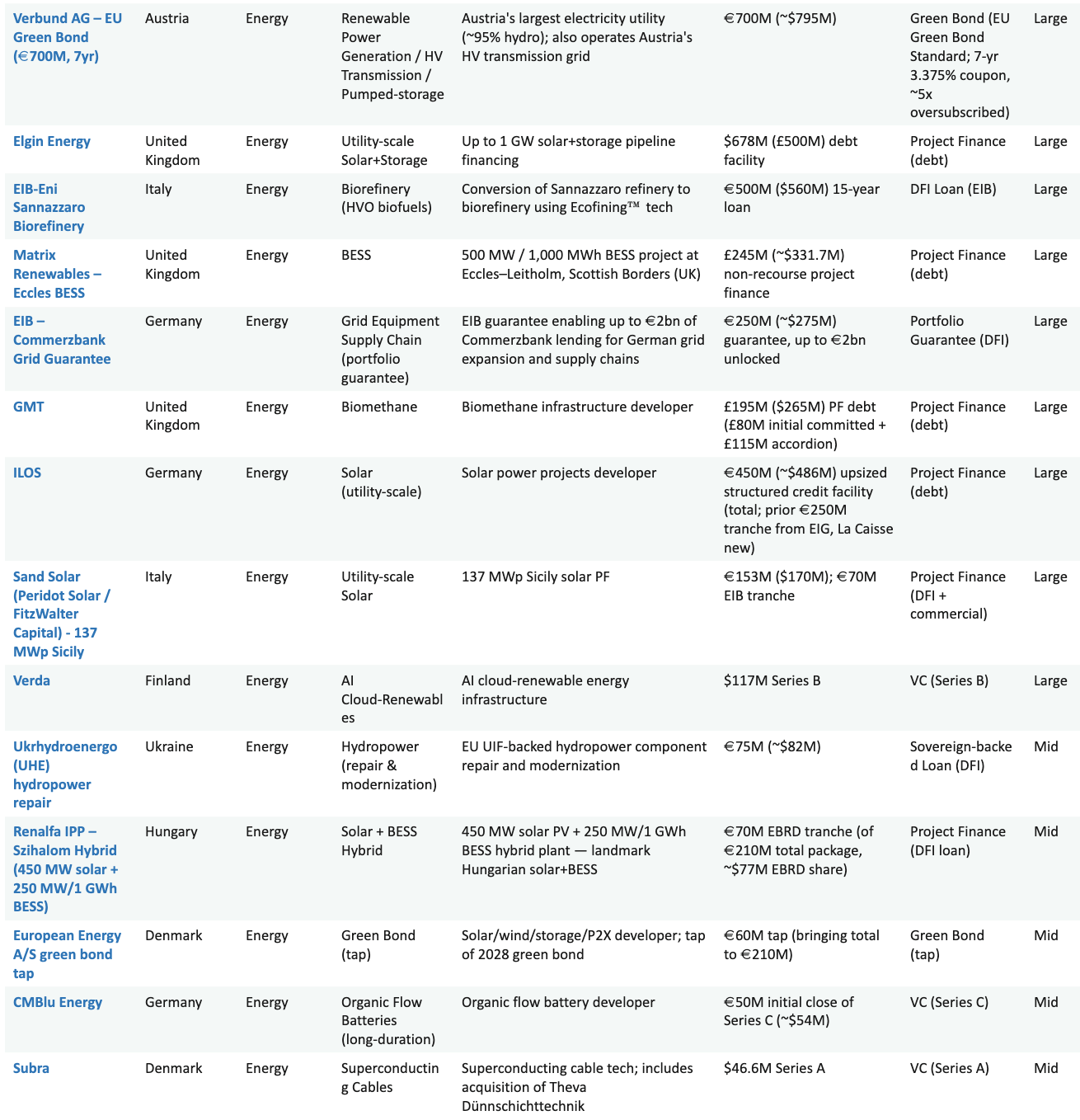

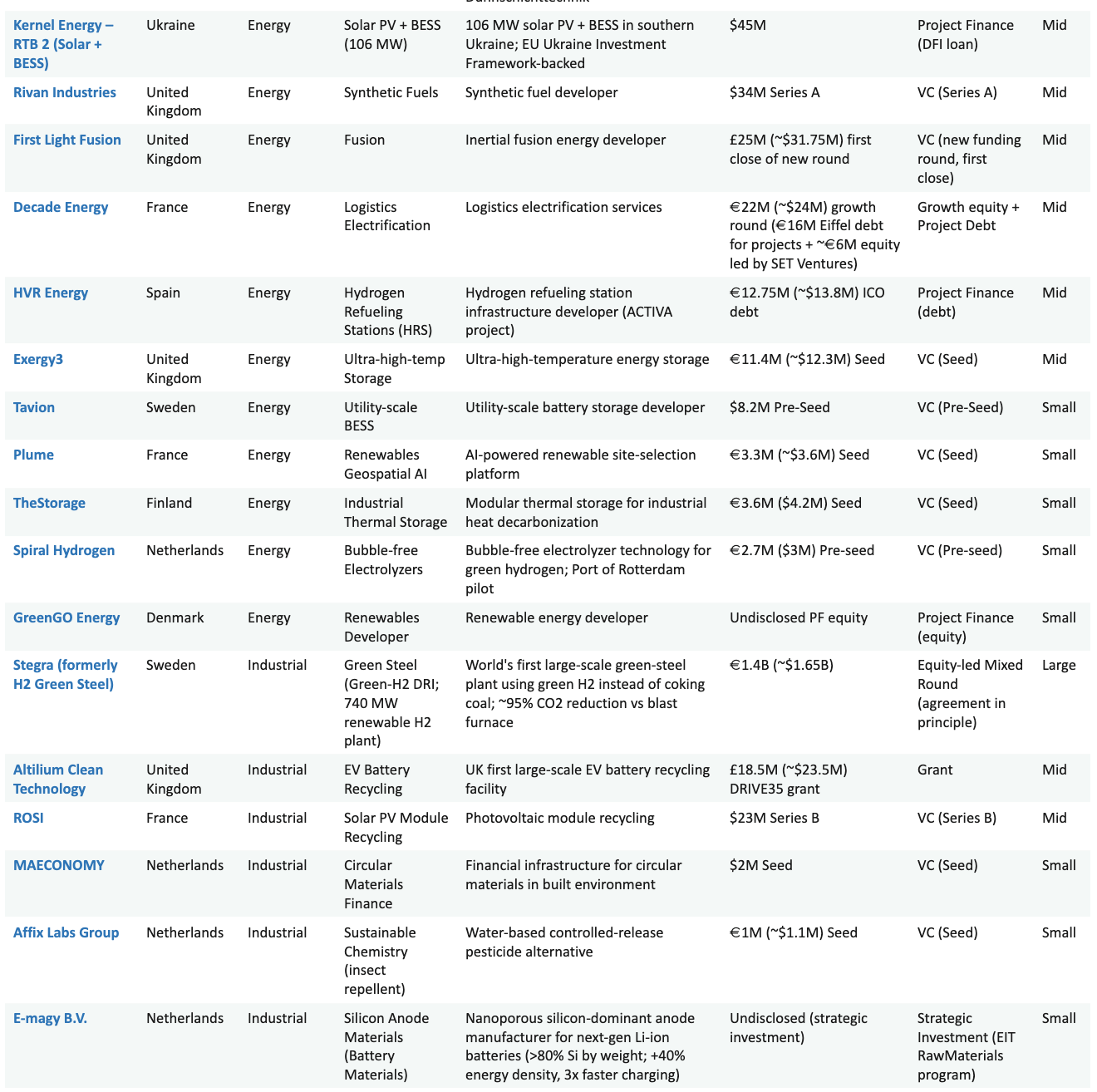

Europe recorded ~$11B across 52 deals, blending a single very large public-finance package with one of the deepest mid-stage deep-tech layers in the world - green steel, superconductors, flow batteries, fusion, geospatial intelligence and a thick fermentation/biocontrol stack.

The structural anchor was the EIB Group Clean Energy Package (~$2.3B of multi-project lending approved in April), reinforcing the pattern of European public finance underwriting deployment while private capital concentrates on first-of-a-kind technology. Below it, Europe produced an unusually rich crop of investable deep tech.

Selected April financings:

Stegra (Sweden) - ~$1.65B equity-led mixed round (agreement in principle); Wallenberg-led consortium with Temasek and IMAS to complete its 740 MW green-hydrogen DRI steel plant.

Xoople (Spain) - $130M Series B (Nazca Capital lead); a satellite-based “Earth’s System of Record” for AI applications; total funding reaches $225M.

Verda (Finland) - $117M Series B; cash-flow-positive AI cloud infrastructure (formerly DataCrunch) on 100% renewable power; an NVIDIA Preferred Partner.

CMBlu Energy (Germany) - €50M Series C first close, crossing a $1B+ valuation; non-lithium organic flow batteries with a 5 GWh Uniper framework.

Subra (Denmark) - €40M (~$46.6M) Series A led by Novo Holdings; high-temperature superconducting cable, paired with the acquisition of Germany’s THEVA.

First Light Fusion (UK) - £25M first close led by East X Ventures’ Starmaker One, with UK Atomic Energy Authority strategic capital, for its FLARE projectile-fusion concept.

Planetary, Cosaic, Agriodor & Fermtech - a clustered ~$45M across Switzerland, France and the UK in precision fermentation, food ingredients and biocontrol.

Exergy3 & TheStorage - $12.3M (UK, ultra-high-temperature 50–1,200°C storage) and ~$4.2M (Finland, modular industrial thermal storage).

Decade Energy (France) - ~$24M (€16M Eiffel project debt + ~€6M equity, SET Ventures lead) for a zero-capex logistics-electrification model.

ROSI & E-magy - $23M (France, high-purity solar-PV module recycling) and a strategic EIT RawMaterials investment (Netherlands, silicon-dominant battery anodes).

Plume, ROCSYS & All3 - Plume (France, €3.3M, AI renewable site-selection), ROCSYS (Netherlands, $13M, robotic EV charging) and All3 (Switzerland, $25M, construction robotics).

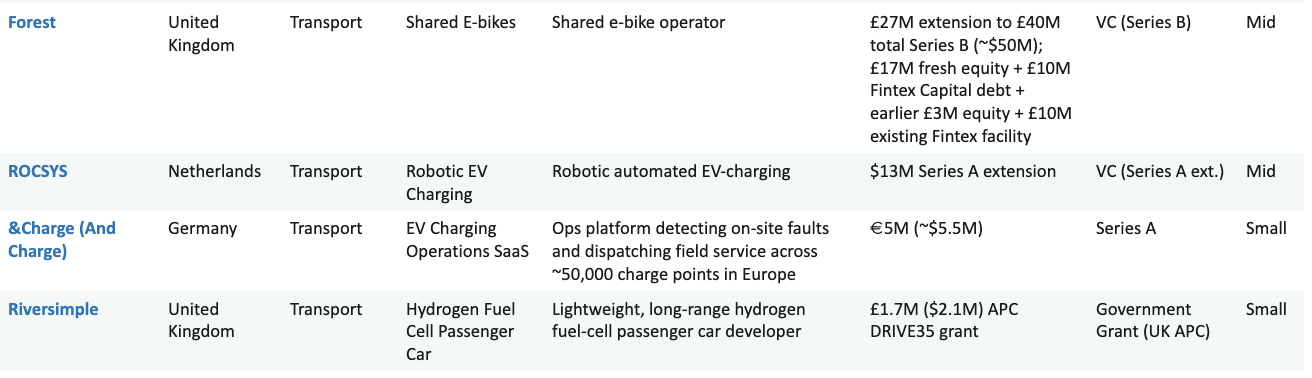

North America recorded ~$6.8B across 48 deals - fewer dollars than Asia or Europe, but the sharpest thematic concentration of the month. The defining narrative is now unmistakable: the U.S. is buying firm, dispatchable power and hard-to-abate industrial decarbonization - nuclear, geothermal, industrial heat and durable carbon removal - at a pace and conviction no other region matches.

Selected highlights:

X-energy (USA) - ~$1.0B Nasdaq IPO (XE), priced above range at $23.00 and opening +31%; Xe-100 SMR plus TRISO-X fuel - the first large advanced-nuclear public-market raise of the year.

Blue Energy (USA) - $380M Series A (VXI Capital lead); MIT spinout building prefabricated reactors with a first Texas project targeting up to 1.5 GW of AI/data-center offtake.

Living Carbon (USA) - $513M ($500M PF + $13M equity) from Octopus Energy Generation; photosynthesis-enhanced poplars targeting up to 50 Mt CO₂ removal.

Sedron Technologies (USA) - up to $500M staged growth equity (Ara Partners); the Varcor system upcycles biosolids and manure into clean water, fertilizer and carbon-negative commodities.

US DOE — DAC Hubs (USA) - ~$1.2B retained for direct-air-capture hubs (Stratos TX and Project Cypress), keeping the U.S. at the frontier of engineered removal.

Zanskar (USA) - $40M non-recourse development facility (scalable to $100M; Just Climate, Spring Lane) to bridge greenfield geothermal pipelines to bank project finance.

Glydways & Also (USA) - $170M and $200M Series C rounds for autonomous transit pods and Rivian-spinout small EVs (with DoorDash).

Slate Auto & Zūm (USA) - $650M Series C (Bezos-backed affordable EV pickup) and $100M growth (TPG Rise, $1.7B valuation, school-transport electrification).

Voltify, SmartD & Humble (USA/Canada) - freight and drivetrain electrification: Voltify ($30M, freight rail), SmartD (~$11M, SiC motor drives) and Humble ($24M, autonomous Class 8 hauler).

Critical Loop & Ayr Energy (USA) - $26M and ~$12M for the grid-bottleneck layer: relocatable microgrids and domestic HV/MV transformers (>20 GW of US contracts).

Helix Earth & Afresh (USA) - $12M (commercial-HVAC retrofit) and $34M Series B (AI grocery operations preventing 200M+ lbs of food waste; Just Climate co-lead).

Sora Fuel, Disa & Nano One (USA/Canada) - Sora Fuel ($14.6M, single-step DAC-to-SAF), Disa Technologies ($33M, critical-mineral processing) and Nano One’s NRCan grant for one-pot LFP cathode.

Starfish Space, Sygaldry, Clarasight & Cloneable (USA) - in-orbit servicing (>$100M), energy-efficient AI servers ($139M), corporate-travel carbon ($11.5M) and AI infrastructure inspection ($4.6M).

TerraSpark, Hydron Energy & Nirova (USA/Canada) - early-stage decarbonization tech: geothermal subsurface AI (~$5.7M), landfill-gas-to-RNG upgrading and anaerobic digestion (~$3M).

Asia-Pacific recorded ~$22B across 53 deals - nearly half the month’s global total - with China anchoring large battery, robotics and grid rounds and India dominating renewables, hydropower and the mid/small EV-and-water layer. The scale here is simply different: single Asian infrastructure deals routinely exceed entire regional totals elsewhere.

Key highlights from Asia:

CATL (China) - ~$5.0B EV-battery placement, the single largest tracked deal of the month.

Kamala & Kalai-II Hydropower (India) - ~$2.8B and ~$1.65B NHPC/THDC joint ventures in Arunachal Pradesh - large storage hydro returning as firm capacity.

TotalEnergies × Masdar (UAE / multi-region) - $2.2B Asia renewables platform (solar + wind + BESS), plus a separate $1.2B Kazakhstan wind+BESS FID.

Sigenergy (China) - ~$562M HKEX IPO that closed ~103% up on debut; its SigenStor integrated PV+BESS+EV-charging system holds ~28.6% of the global stackable distributed solar-storage market.

X Square Robot, Pudu & Booster (China) - $276M, $150M and $137M into humanoid and service robotics.

Spacety & Chang Guang (China) - $190M and ~$70M pre-IPO rounds for SAR and optical Earth-observation constellations.

Envision Energy & NovaFusionX (China) - $500M (BBVA vendor-finance facility) and ~$102.5M (modular FRC fusion).

Volant Aerotech & FAW Qiyi (China) - >$300M and ~$55M into passenger eVTOL; FAW’s is the largest angel-stage eVTOL round in China to date.

Graphite Energy (Australia) - A$40M (~$26M, debt + equity) for renewable-powered thermal energy storage replacing fossil boilers.

ECOMMIT (Japan) & WorkOnGrid (India) - ~$10M Series B (circular-economy / waste-data; Mercari backing) and ~$2.4M (AI “DiscomGPT” utility intelligence).

India’s EV & water long tail - Simple Energy ($13.2M pre-IPO E2W), Astranova Mobility ($6.4M), TrEV Mobility ($0.43M) and AquaPulse ($2.94M, IoT water-quality monitoring).

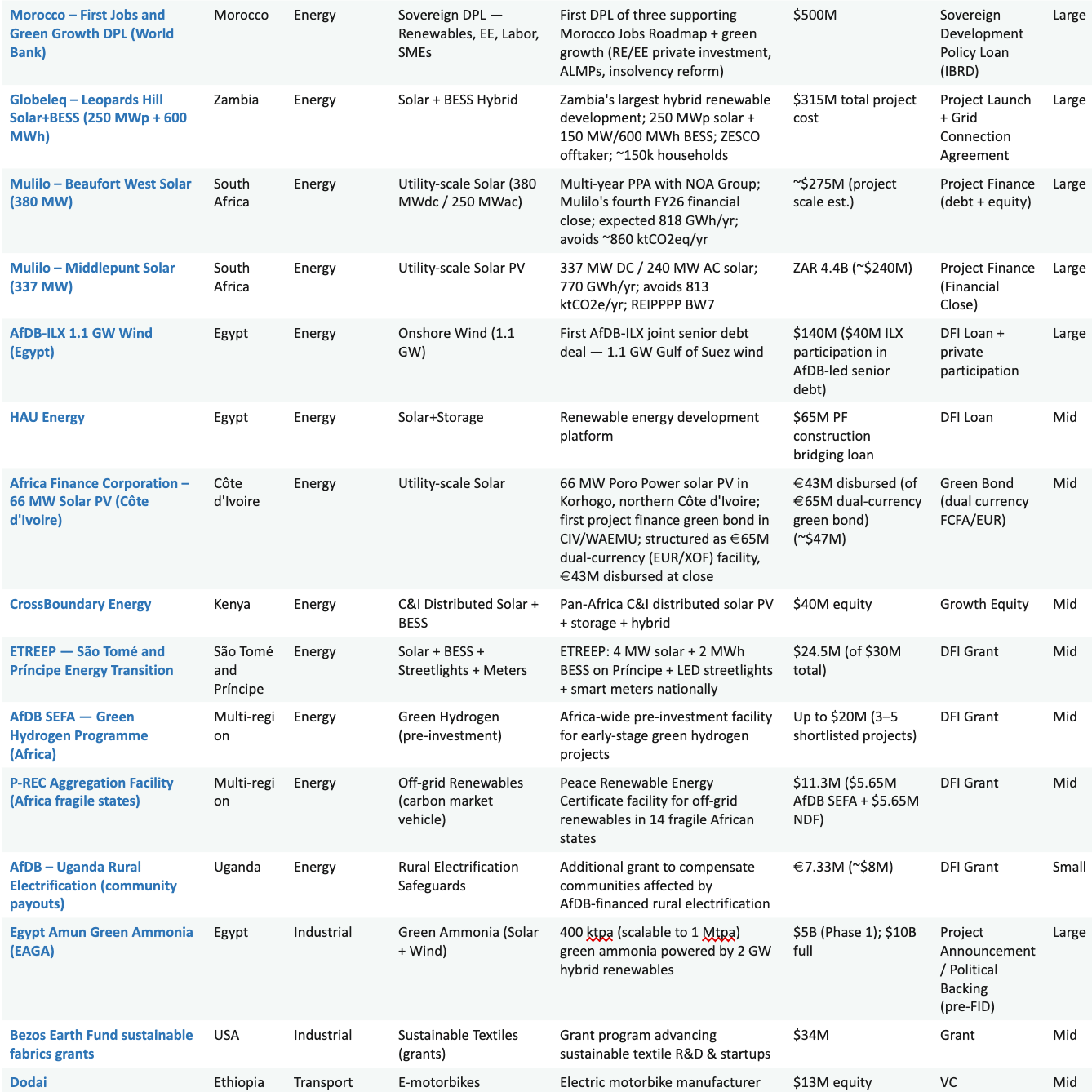

RoW (Africa, South America, Australia) recorded ~$15.7B combined across 54 deals. Africa recorded ~$8.3B across 29 deals, Australia ~$3.8B across 9 deals and Latin America ~$3.6B across 16 deals. As in prior editions, the picture across these markets remains anchored by MDB and DFI interventions and blended-finance structures, while commercial private capital stays comparatively constrained - with two striking exceptions this month: a $5B private green-ammonia pledge and the largest reforestation fund ever closed.

Selected highlights:

Egypt Amun Green Ammonia / EAGA (Egypt) - $5B Phase-1 pledge (scaling to $10B), 400 ktpa green ammonia powered by 2 GW of hybrid solar+wind at Ras Banas.

Central-West Orana REZ (Australia) - ~$3.6B for Australia’s first contestable Renewable Energy Zone transmission project (4.5 GW initial transfer capacity).

BTG Pactual TIG Reforestation Fund (Brazil / pan-LATAM) - $1.24B final close - the largest reforestation fund to date - and the first project globally to issue credits under Verra VM0047.

BNDES – KfW / BMZ Green Declarations (Brazil) - BRL 4.1bn (~$810M) of bilateral green cooperation signed at Hannover Fair 2026.

KfW / World Bank — South Africa (South Africa) - a $540M JET-P grid-expansion loan plus the $120M Spekboom restoration outcome bond and a $200M IFC green-buildings facility for Investec.

Adaptation Fund — Southern Africa (multi-country) - close to $134M approved at the 46th Board meeting, including Malawi’s $20M smallholder resilience project and the transboundary Kunene River Basin project (~$24.55M).

Dodai (Ethiopia) - $13M Series A ($8M equity + $5M BII debt) for locally-assembled electric motorbikes, with expansion planned across West and East Africa.

Tropical Bioás & São Paulo Green Corridor (Brazil) - ~$52M (biomethane from sugarcane vinasse) and ~$28M (biomethane heavy-truck refuelling corridor).

Satellites on Fire (Argentina) - $2.7M seed (Dalus Capital lead) for real-time wildfire detection ~35 minutes ahead of NASA’s FIRMS service.

Q1 set the tone; April redrew the scale. The structure we have tracked all year held - and hardened: firm, capital-heavy power in the U.S.; mass-market and utility-scale electrification across Asia; policy-backed project finance and deep tech in Europe; and blended adaptation and nature finance across the Global South. April did not break the pattern. It supersized it - and added the sharpest nuclear-versus-renewables, nature-based-solutions and robotics signals we have recorded.

May will test whether $55B was a structural step-change or a coverage-and-mega-deal spike. We will be watching whether the themes identified in December continue to deepen:

U.S.: Nuclear and Geothermal vs. Rest of World: Solar and Wind

“Solarpunk” Momentum - electrification beyond cars, powered by cheap batteries

Dual-Use Innovation: Climate + Defense, Supply Chain, Compute

CapEx-Intensive Mid-Stage Tech and the “Valley of Death”

Industrial Heat Electrification

Nature-Based Solutions for Carbon and Biodiversity

AFOLU Innovation - including climate adaptation, robotics, and alternative proteins

The Rise of Climate Robotics

Stay tuned for next month’s edition as we continue to follow the capital shaping the climate transition.