With Howard Kung (LBS) and James Paron (Stanford GSB).

Here is a puzzle. On the days when major AI labs release new frontier models — the kind of news that presumably raises expectations about future productivity growth — nominal and real Treasury yields fall. Andrews and Farboodi (2025) document this pattern across 17 model releases in a fascinating paper. Standard theory predicts that risk-free real rates increase when we expect higher economic growth as some of us try to consume some of that extra future income today by borrowing, thus pushing up rates. The conventional interpretation of these findings is that markets are revising growth expectations down, not up: bad news for AI optimism.

But maybe that’s not the whole story. Howard Kung, James Paron and I think that nominal Treasury yields probably should decline on positive AI news, because Treasury investors are implicitly long productivity growth. Given the structure of the tax code and the composition of government spending, government debt has a large positive productivity beta. If you own a 10-year Treasury, you are, whether you know it or not, making a sizable bet on AI.

Government bonds are ultimately backed by future primary surpluses — the difference between what the government collects in taxes and what it spends on everything except interest, just like a mortgage backed security is backed by the stream of future mortgage payments. So the valuation question is: what happens to that surplus stream when GDP growth accelerates?

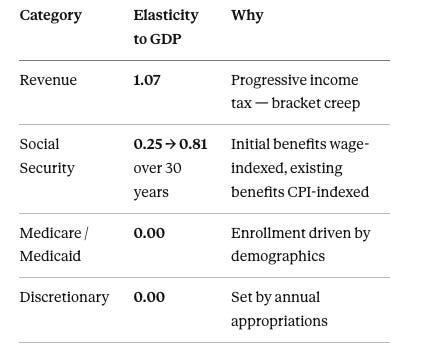

Revenue and spending respond very differently. The CBO publishes “rules of thumb” that quantify the sensitivities, and the asymmetry is striking. If productivity growth runs 0.1 percentage points slower per year over the next decade:

Revenue falls by $572 billion.

Mandatory spending falls by $43 billion.

The cumulative deficit widens by $388 billion.

For every dollar of revenue the government loses when growth slows, spending falls by about eight cents. Translated into elasticities, the CBO’s rules of thumb imply:

The revenue elasticity is modestly above one because the tax code is progressive. When incomes rise, households creep into higher brackets. The CBO calls this “real bracket creep.” It is a relatively small effect — an elasticity of 1.07 means revenue grows only 7% faster than GDP — but it compounds over thirty years into real money. On the spending side, Medicare and Medicaid are driven by demographics — how many people turn 65 — not by how fast the economy grows. Discretionary spending is set by annual appropriations. Neither line item has any automatic link to productivity.

Social Security is the subtle case. Initial benefits are indexed to wages (through the Average Indexed Monthly Earnings formula), but once you start collecting, your benefits are adjusted for inflation, not wages. Over a 10-year window, most beneficiaries are already locked in at pre-shock wage levels, so the effective elasticity is only 0.25. Over a longer horizon, the beneficiary pool turns over: old cohorts die, new cohorts claim benefits indexed to the higher post-shock wage level, and the elasticity ramps up toward roughly 0.81 by year 30. We model this turnover as an exponential process with a calibrated duration of about 18 years — roughly consistent with average claiming age and beneficiary life expectancy.

So when GDP grows faster, the government collects a lot more and spends only a little more. The difference flows straight to primary surpluses. Bondholders are implicitly holding a levered claim on GDP, financed by a short position in an inflation-indexed bond. That is a long productivity position.

How big is this effect? We take the CBO’s 30-year budget baseline, apply the CBO-implied elasticities, and roll the debt forward under alternative growth scenarios. We follow Jiang, Lustig, Van Nieuwerburgh, and Xiaolan (2022) in discounting surpluses at the Treasury yield curve —plus a 2.6 percentage point GDP risk premium—, and we let the real interest rate rise one-for-one with productivity growth in the long run, as the CBO’s own workbook implies.

The results:

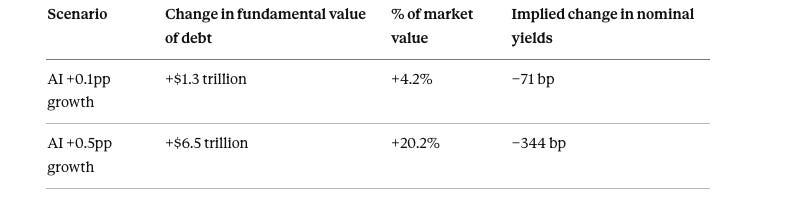

A tenth of a percentage point of extra productivity growth — well within the range of plausible near-term AI effects — raises the fundamental value of U.S. government debt by $1.3 trillion. If markets fully priced this in, nominal Treasury yields would fall by about 70 basis points.

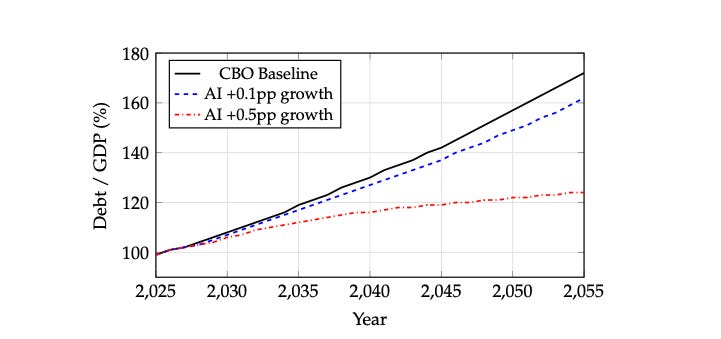

Half a percentage point of extra growth would raise the value of the debt by $6.5 trillion. For context: under the CBO baseline, the debt-to-GDP ratio rises from 100% today to 172% by 2055. Under the +0.5pp scenario, it stabilizes near 124%. Debt-to-GDP stops exploding. That is an enormous change in the fiscal outlook, and it comes from a rate of growth only modestly above the post-2000 average.1

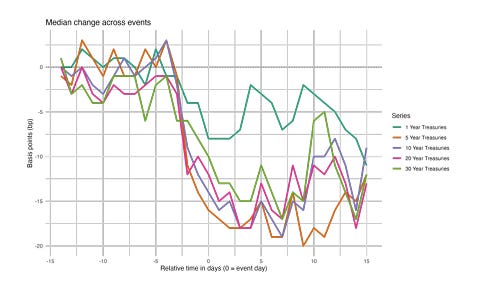

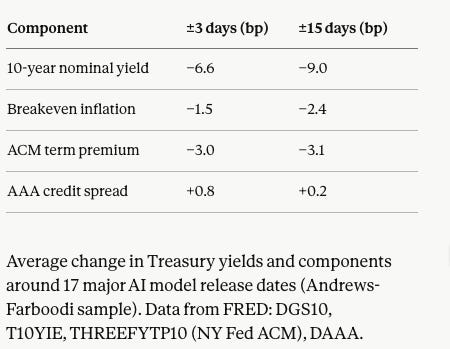

Back to the AI model releases. Around those 17 events, the 10-year nominal yield falls by 6.6 basis points in a three-day window and 9.0 basis points over fifteen days. That is consistent with markets pricing in a small AI-driven improvement in fiscal fundamentals.2

Three pieces line up with the fiscal story. The nominal yield falls. Breakeven inflation falls — consistent with the disinflationary nature of productivity growth and, in a fiscal theory reading, with a better-collateralized debt stock. The term premium compresses, which is what you'd expect if the government's ability to service its debt becomes less uncertain (see work by James Paron and his co-authors “Sovereign Default and the Decline in Interest Rates”, and “Fiscal Redistribution Risk in Treasury Markets”). Convenience yields, measured by the AAA credit spread, increase (a tiny bit), consistent with the decrease in debt/GDP ratios pushing down the supply of safe assets.

So the empirical pattern may not be evidence that investors expect AI to disappoint. It might be exactly what you should see if investors are long growth through their Treasury holdings and are revising growth expectations modestly upward. If you don’t think it’s plausible that bond traders respond to fiscal shocks, take a look at this paper for some high-frequency evidence.

There is a second, subtler point. Because revenue scales as GDP^1.07, the fundamental value of the debt is a convex function of productivity growth. A +1pp growth shock raises value by 108%; a −1pp shock only lowers it by 87%.

That asymmetry means bondholders gain from uncertainty, not just from higher expected growth. If markets become more uncertain about AI’s long-run productivity impact, and that uncertainty is mean-preserving, Treasury valuations should still rise. Holding expected growth fixed, ±0.5pp of growth uncertainty is worth about $0.7 trillion in convexity value. Treasuries embed a long call option on AI, and the option is valuable even when the strike is out of the money.

The obvious risk is the tax code. The whole story runs on the 1.53 revenue elasticity, which depends on the progressive bracket structure. If Congress responds to AI-driven surpluses by cutting rates, flattening brackets, or indexing brackets to wages rather than inflation, real bracket creep goes away and the elasticity falls toward one. That is not a hypothetical: EGTRRA and JGTRRA in 2001 and 2003 dissipated the late-1990s surpluses within a couple of years. The political economy is asymmetric. When growth generates a windfall, there is strong pressure to cut taxes. When growth disappoints, there is almost no pressure to raise them.

So bondholders betting on AI are also betting that Congress will not fully hand the windfall back to voters. Reasonable people can disagree about those odds.

This is why AI matters for Treasurys. It is not just a story about whether faster growth lifts real risk-free rates. It is a story about whether the collateral behind the debt — the present value of future surpluses — is worth what the market is paying for it. The government’s fiscal balance sheet is enormously sensitive to productivity. And so, whether they know it or not, are Treasury investors.

The full paper is here. All calculations replicate from public CBO data.

Andrews, Isaiah, and Maryam Farboodi (2025). “Pricing Transformative AI.” Working paper, MIT.

Gómez-Cram, Roberto, Howard Kung, and Hanno Lustig (2025). “Can U.S. Treasury Markets Add and Subtract?” NBER Working Paper No. 33604. https://www.nber.org/papers/w33604

Gómez-Cram, Roberto, Howard Kung, Hanno Lustig, and David Zeke (2025). “Fiscal Redistribution Risk in Treasury Markets.” NBER Working Paper No. 33769. https://www.nber.org/papers/w33769

Jiang, Zhengyang, Hanno Lustig, Stijn Van Nieuwerburgh, and Mindy Z. Xiaolan (2022). “Measuring U.S. Fiscal Capacity Using Discounted Cash Flow Analysis.” Brookings Papers on Economic Activity 53(2), 157–229.

Miller, Max, James D. Paron, and Jessica A. Wachter (2025). "Sovereign Default and the Decline in Interest Rates." NBER Working Paper No. 34021. https://www.nber.org/papers/w34021

Warsh, Kevin (2026). Testimony before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, April 21, 2026.

The fine print

Those numbers are smaller than they might be, because we make three conservative assumptions worth flagging.

Long-run elasticities collapse to one. The CBO’s rules of thumb give us elasticities over a 30-year horizon. Beyond that, we hold the post-2055 surplus-to-GDP ratio at its baseline level. In other words, we assume that in the long run, both revenue and spending scale one-for-one with GDP. If the short-horizon pattern extrapolated forever — revenue growing at ε=1.07, spending largely inelastic — the fiscal windfall from AI would be larger. Our terminal value grows with the GDP level, but not more than proportionally.

This matters because a lot of the market value of Treasuries sits beyond the 30-year horizon. Under the CBO baseline, the present value of surpluses inside the next 30 years is negative $12.5 trillion. The entire $32 trillion market value of the debt is backed by a terminal value — a claim on what happens after 2055. By assuming unit elasticity in the terminal, we are saying that the long-run fiscal adjustment (whatever form it takes) scales with the economy. This is conservative.

Real rates rise with productivity. In each AI scenario, we let the real interest rate rise with productivity growth using the CBO’s own pass-through. In the long run, this is roughly one-for-one (∆r ≈ ∆g). Higher discount rates partly offset the cash flow improvement. If we instead held discount rates fixed at the baseline, the +0.1pp scenario would deliver $2.5 trillion of extra value instead of $1.3 trillion, and the +0.5pp scenario would deliver $13.3 trillion instead of $6.5 trillion. We use the pass-through version because it is consistent with the CBO’s own view of how growth maps to rates.

The terminal value is calibrated to current prices. Following Jiang et al. (2022), we pick the post-2055 terminal value so that the baseline valuation equation reproduces the actual $32.1 trillion market value of debt today. We are not making a claim about whether Treasurys are correctly priced in absolute terms — only about how valuations should move when the growth outlook changes. Investors are implicitly assuming some future fiscal correction or financial repression that our calibration absorbs into the terminal.

With those assumptions in hand, the decomposition of the +0.1pp case is instructive. The entire $1.3 trillion gain comes from within-horizon surpluses, which improve from −$12.5 trillion to −$11.2 trillion. The terminal value is essentially flat at $44.6 trillion: the higher GDP level lifts the nominal terminal surplus, but higher discount rates reduce its present value by almost exactly the same amount. Essentially all of the fiscal windfall from a permanent productivity acceleration shows up in the first thirty years of cash flows.

Using Gómez-Cram, Kung, and Lustig (2025)’s decomposition of yield responses to CBO cost estimates, the 101bp move implied by our +0.1pp scenario would split into roughly 39bp of lower expected inflation, 44bp of compressed term premium, and 17bp of higher convenience yields. All three channels are moving in the observed data.