There is a precise moment when a bubble stops being an unpopular idea and becomes consensus. For AI, we are there.

Matt Stoller, one of the most widely read economic journalists in the United States, opened his latest piece with a clear observation: it is now consensus that we are in an AI investment bubble, and that this bubble represents a risk to the broader economy. It is no longer a contrarian position. It has become the starting point.

Stoller is not alone. Michael Burry — the hedge fund manager who predicted and bet against the 2008 subprime mortgage collapse, made famous by the film The Big Short — has opened a short position (a bet that prices will fall) on the semiconductor ETF SOXX, expiring January 2027. He has said publicly: “the market has overshot, the end is near.”

The problem is not that these voices do not exist. The problem is that the public debate keeps telling the same story. The spend-vs-revenue gap. The dot-com comparison. Valuations through the roof. All the right pieces, packaged in a way that makes them feel already processed, already priced in, already old news.

What follows is an attempt to go deeper. Not just what the articles say — but what they do not say, and why.

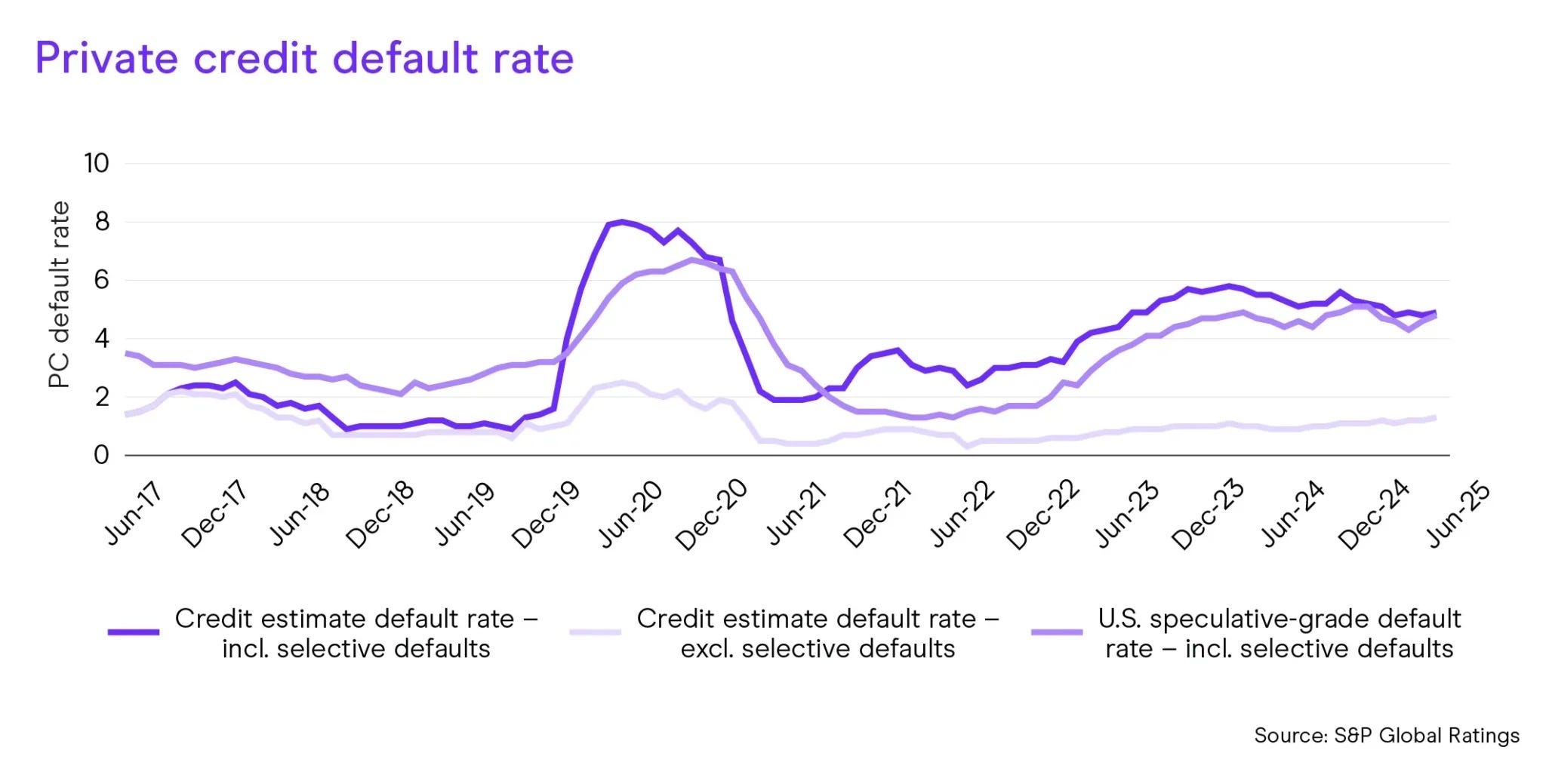

The number you find in every article about AI is this: American companies are spending over $500 billion a year on AI infrastructure. Real consumer AI revenues sit at around $12 billion.

David Cahn, an analyst at Sequoia Capital — one of the most important venture capital funds in the world, the one that backed Apple and Google in their early days — calculated that the AI sector would need to generate roughly $600 billion in annual revenue just to cover the infrastructure it is building. That gap, which was $200 billion in 2023, grew to $600 billion in 2024. In 2026, with spending still accelerating, it is wider still.

But the number nobody actually finishes reading is the one belonging to OpenAI.

Text within this block will maintain its original spacing when published

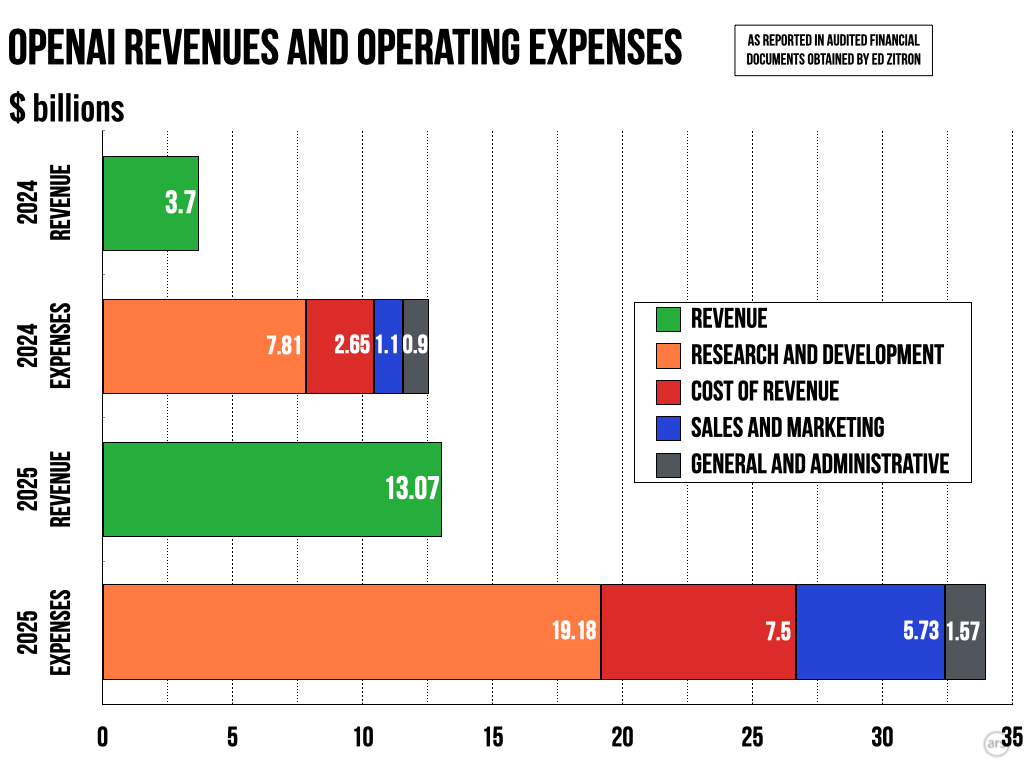

On June 16, 2026, certified financial documents from OpenAI were obtained by journalist Ed Zitron and independently verified by the Financial Times. They were published days before OpenAI filed its confidential IPO prospectus with the SEC.The numbers: in 2025, OpenAI reached $13.07 billion in revenue — more than triple the $3.7 billion of 2024. But total costs reached $34 billion, with $19.18 billion in research and development alone. Operating loss was $20.92 billion. Net loss reached $38.5 billion.

Leaked financial docs show OpenAI is losing billions of dollars a year — Source: ArsTechnica / Kyle Orland

To put this in perspective: for every dollar OpenAI earned, it spent $1.60. And that is already an improvement over 2024, when it spent $2.37 for every dollar it brought in.

Of those $34 billion in costs, $17.2 billion went directly to Microsoft for Azure cloud infrastructure and research compute. Microsoft, in return, paid OpenAI just $303 million. SoftBank paid $867 million. Come back to this when we reach the section on circular financing.

That math does not work even in an optimistic scenario. This is not a timing problem. It is structural.

The comparison with the internet bubble of 2000 is the most effective way to make people feel informed without actually understanding anything. Everyone uses it, in both directions.

Bulls (those who believe prices will keep rising) say: “this time is different, the companies have real revenues.” Bears (those who believe prices will fall) say: “it’s exactly like 1999.” Both are partially right, and that ambiguity is precisely the problem.

Let us start with what makes the current situation less severe than 2000:

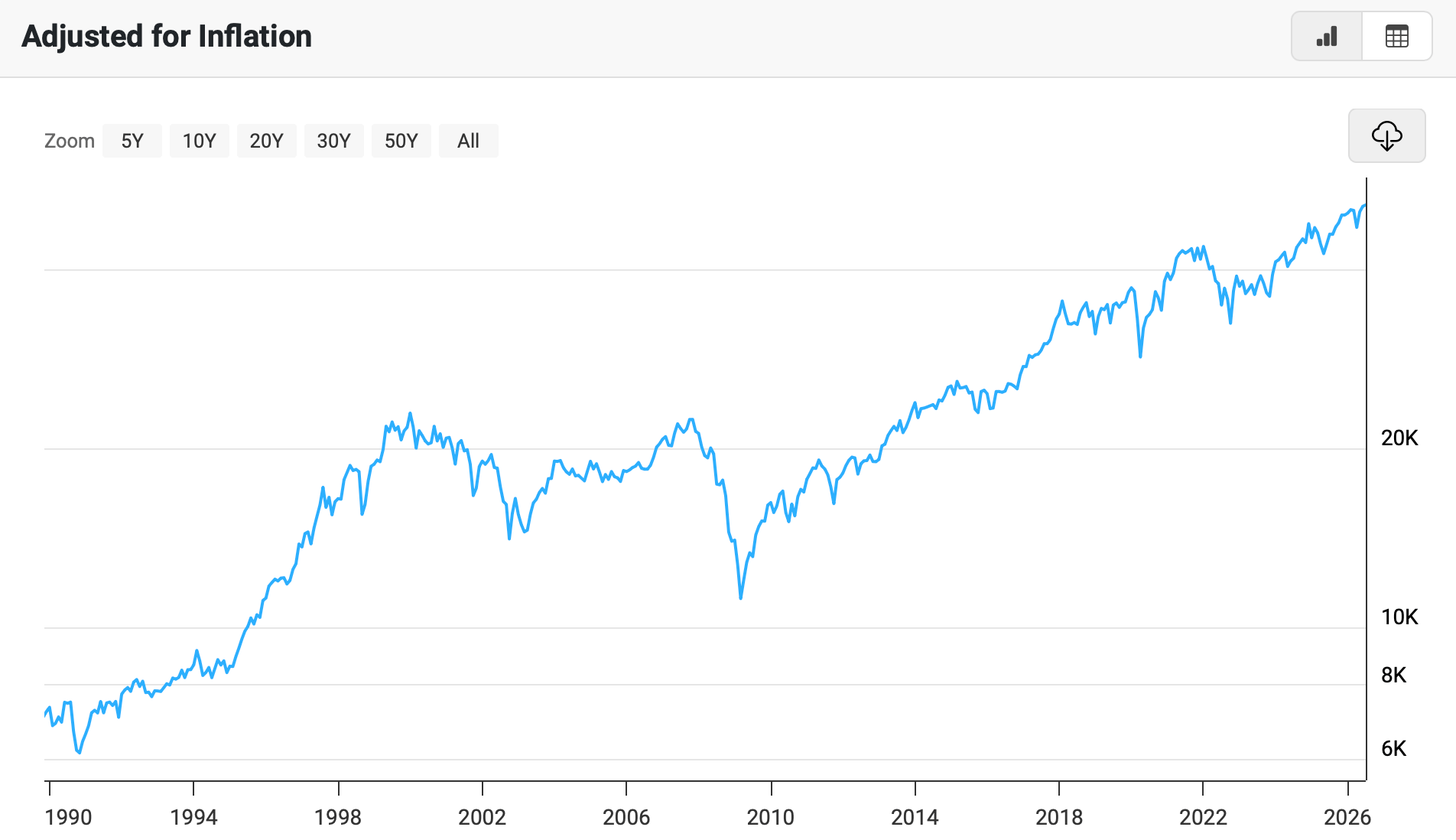

The NASDAQ rose 125% from the launch of ChatGPT to its October 2025 peak. During the dot-com bubble, it rose 700%.

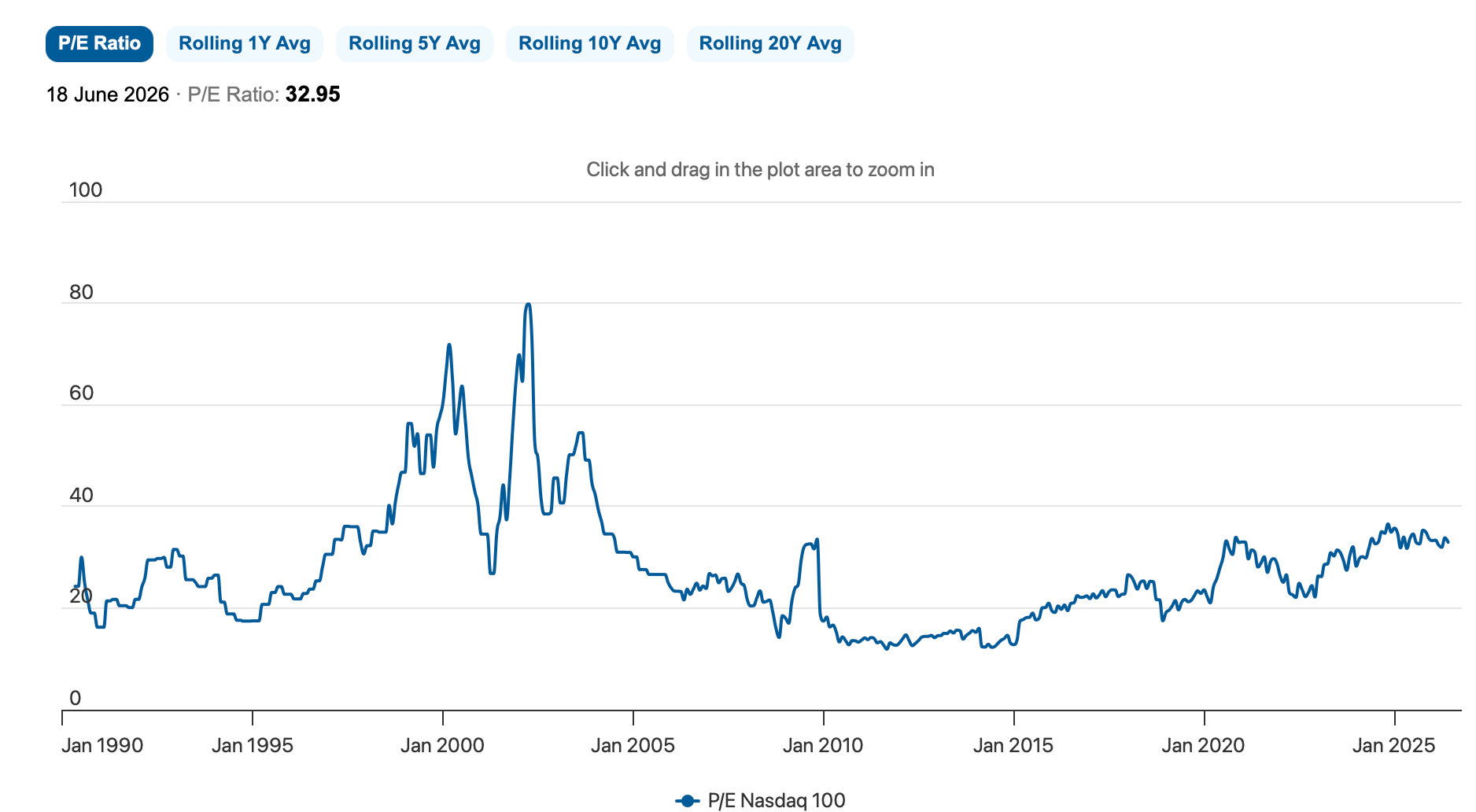

The forward P/E — the ratio between a stock’s price and its expected earnings over the next 12 months, a measure of how much the market is “paying” for future expectations — was at 79x at the dot-com peak. Today it sits around 25x.

Nasdaq 100 Index: current P/E Ratio - World PE Ratio

These numbers seem reassuring. But they obscure something important.

The total value of the US stock market today approaches $80 trillion. That is roughly twice what it was at the dot-com peak. It is 2.5 times the size of the entire American economy. Economist Dean Baker has calculated that a simple return to the long-run historical average would strip, on average, $300,000 in paper wealth from every American household.

Dow Jones - 100 Year Historical Chart - MacroTrends

The most important structural difference from 2000 is real: today’s major tech giants fund AI investments primarily from existing cash flows. In 2000, many dot-com companies had no real revenues at all. That distinction matters.

“This time the companies have real revenues.” True. But the total market is twice the size of the dot-com peak. The fall — when it comes — can be much slower, and much longer.

During the internet boom of the 1990s, a practice called vendor financing became increasingly common. It worked like this: telecom companies wanted to buy network infrastructure but had no money. So the suppliers — like Lucent Technologies — lent them the money to buy it. At its peak, Lucent had over $15 billion in these loans to its own customers, against an operating cash flow of just $300 million. Lucent then went bankrupt.

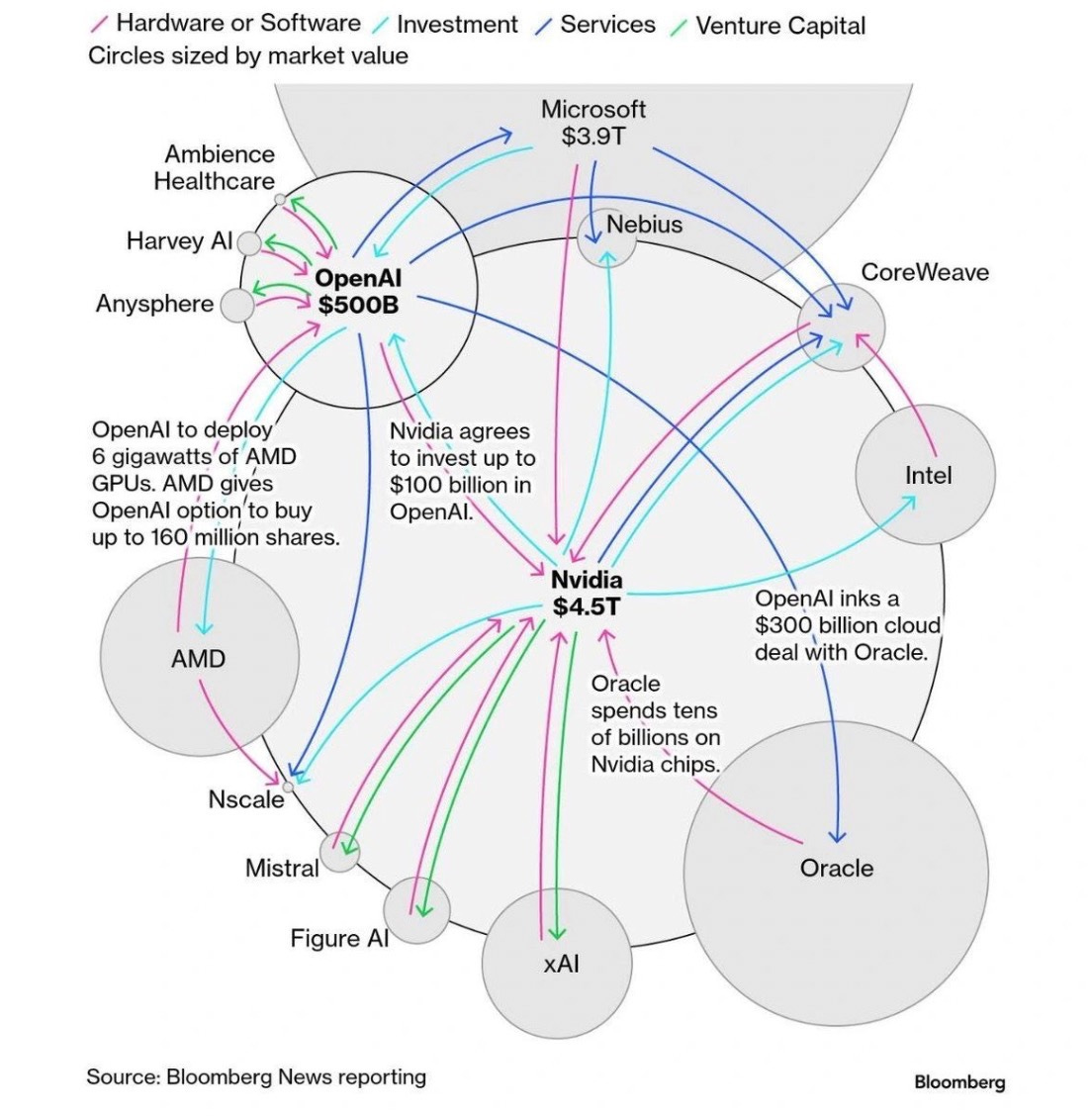

Today the structure is identical, but the numbers are vastly larger — and the loop is tighter.

LOOP

Nvidia invests $100B in OpenAI → OpenAI buys Nvidia chips to build data centers → Nvidia guarantees its own future demand by investing in its primary customer → the cycle begins again.

And then there is the Microsoft dynamic that emerges from the leaked OpenAI financials. OpenAI pays Microsoft $17.2 billion to use Azure cloud infrastructure. Microsoft owns roughly 27% of OpenAI. It is simultaneously OpenAI’s largest investor, largest supplier, and largest cost. Every dollar OpenAI spends on Azure flows back to Microsoft partly as profit, and partly as appreciation of its own investment in OpenAI.

The central problem, as David Cahn of Sequoia argued, is downstream from all of this: the companies that use data centers — those training models or running inference — are not economically sustainable at current compute costs. They are paying for processing power hoping that one day revenues will cover costs. Those data centers were built on the assumption that OpenAI will pay them billions in the future. If OpenAI cannot grow revenues fast enough, the companies that built those centers will find themselves underwater.

This is probably the most underappreciated point in the entire discussion — and it is underappreciated deliberately, because its implications are uncomfortable for too many parties.

Those financing AI data center construction — banks, insurers, pension funds, private credit vehicles — believe they are financing long-lived infrastructure assets, comparable to commercial real estate or utility plants. Their models assume a useful life of 7 to 15 years for these assets, with stable cash flows and recoverable collateral value in the event of default.

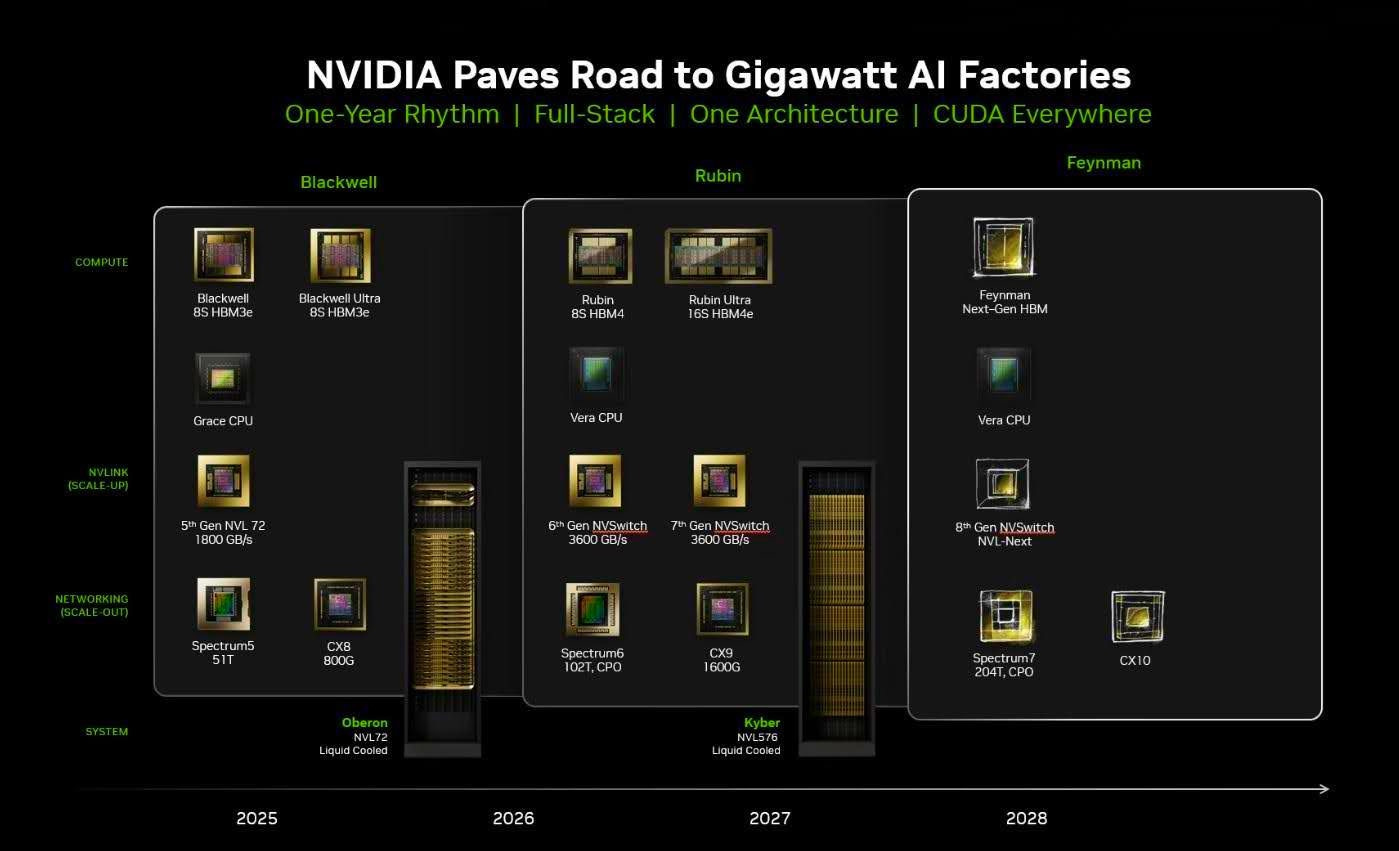

The problem is that the real economic life of a GPU — the specialized graphics card that powers every AI data center — is roughly one year. A data center full of Nvidia H100 chips in 2024 is already at a competitive disadvantage against one running Blackwell chips in 2025.

Nvidia chip roadmap — GTC 2025: Blackwell → Rubin → Rubin Ultra → Feynman. New generation every ~18 months.

Amazon has quietly acknowledged this: it reduced the depreciation period for its servers from six years to five, explicitly admitting in its 10-K that it retired servers and network equipment ahead of schedule in 2024.

Banks are lending money on 15-year timelines for assets that lose competitive value in 12 months.

If the previous point is the hidden risk in credit, this is the hidden risk in credit you cannot even see.

Tech giants including Oracle, xAI, CoreWeave, and Meta have moved roughly $120 billion in data center spending into Special Purpose Vehicles — SPVs — off their main balance sheets. An SPV is a separate legal entity created specifically to hold debt outside a parent company’s primary accounts. It is legal, regulated, and common across many industries. The problem is not legality. The problem is visibility.

Text within this block will maintain its original spacing when published

The subprime mortgages that triggered the global financial crisis were also held in off-balance-sheet vehicles. Off the radar of rating agencies. Off the radar of regulators. Until they weren’t.The Federal Reserve has noticed. Its Spring 2026 Financial Stability Report explicitly identifies the growth of AI-related private credit among the primary risks to the financial system.

The global tech sector issued $428 billion in bonds in 2025 — meaning companies borrowed that amount from investors in debt security form. The US drove the majority, with $341.8 billion. Most of that commitment is allocated to AI capex.

Source: Withinitelligence

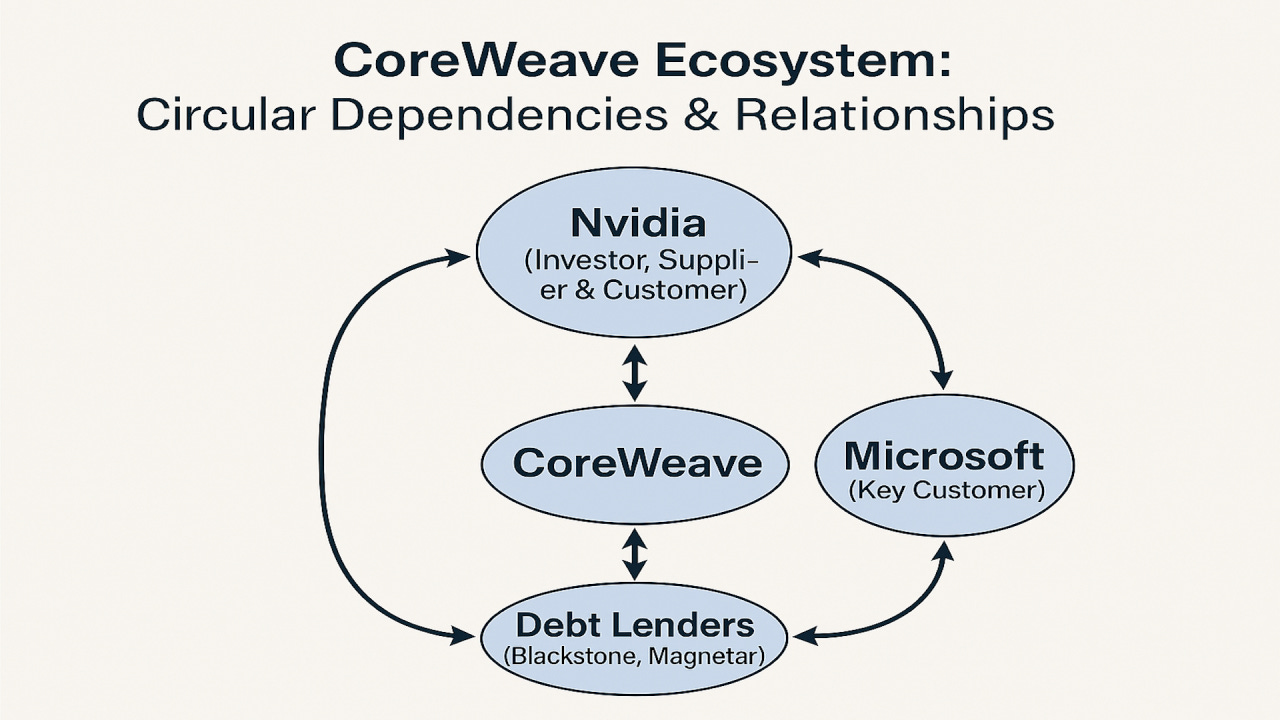

If you want a single concrete company that embodies every risk described above in one publicly traded entity, it is called CoreWeave. It rents AI compute capacity — essentially leasing GPUs to companies that want to train or run AI models without building their own data center.

The growth has been explosive: from $16 million in revenue in 2022 to $1.9 billion in 2024. An impressive number. But beneath the surface:

It has operating losses — it spends more than it earns

At end of 2024, its cash burn rate would have sustained operations for roughly 9 months without new financing

It carries $24.5 billion in total debt, including off-balance-sheet operating leases

It faces $7.5 billion in interest payments by end of 2026

62% of its revenues come from a single customer: Microsoft

CoreWeave financial structure: circular dependencies between Nvidia, Microsoft, and private debt lenders.

CoreWeave survives as long as Microsoft keeps paying. If Microsoft reduces its AI spending, CoreWeave has months, not years.

It is a small company relative to Nvidia or Microsoft. That is why it does not make front pages. CoreWeave liquidity crisis would not make news because of its size — it would make news because it would make visible to everyone the structural problem affecting dozens of companies built on the same blueprint.

Matt Stoller asks the right question: not whether the bubble will burst, but how it will propagate when it does. The answer requires understanding what financial contagion actually means — how a shock in one part of the system transmits to others.

Form 1 — Balance Sheet Contagion: The 2008 Model

When a leveraged bet goes wrong, the mechanism is always the same: you cannot repay the loan → the lender cannot meet its own obligations → whoever lent to that lender cannot recover their funds → and so on, in a long chain. The net effect is that everyone tries to sell whatever they can to cover debts, triggering a massive asset liquidation.

In the AI context, this risk is concentrated in private credit and the SPVs described above. Less visible than 2008, when the problem was enclosed in the mortgages of millions of American families. But not less real.

Form 2 — Paper Wealth Contagion: The Dot-Com Model

When an AI company goes public — as OpenAI and Anthropic are about to — it creates enormous theoretical new wealth for early investors: employees, universities, pension funds, endowments. These institutions become dependent on the value of that stock. If shares fall, they must restructure their balance sheets, cut spending, and those effects cascade into other sectors.

American universities in particular have invested heavily in AI through their endowment funds. A collapse would directly hit their finances — and with them, research programs, scholarships, faculty.

Form 3 — Stranded Infrastructure Contagion

This is the slowest, but perhaps the most persistent. AI infrastructure cannot be repurposed. A data center full of GPUs cannot be converted into something else if AI fails to generate the expected revenues. You cannot “switch it off and wait for better times” — it carries enormous operational costs (power, cooling, maintenance) even when idle.

This is the slowest form of contagion: not an immediate collapse, but years of stranded assets — data centers costing billions to maintain, generating insufficient revenues, impossible to repurpose, and weighing on the balance sheets of whoever financed them.

If the AI bubble bursts in the US, the damage would be concentrated there: dramatic cuts to hyperscaler capex, reduced funding for research labs, waves of layoffs among researchers, and years of political caution around AI as a theme for public investment.

China does not have an equivalent AI bubble because its ecosystem is structured differently: fewer public speculative markets, more direct state mandate, private valuations not subject to Wall Street mood swings. There is no Chinese equivalent of a CoreWeave — publicly traded, burning cash, dependent on a single client.

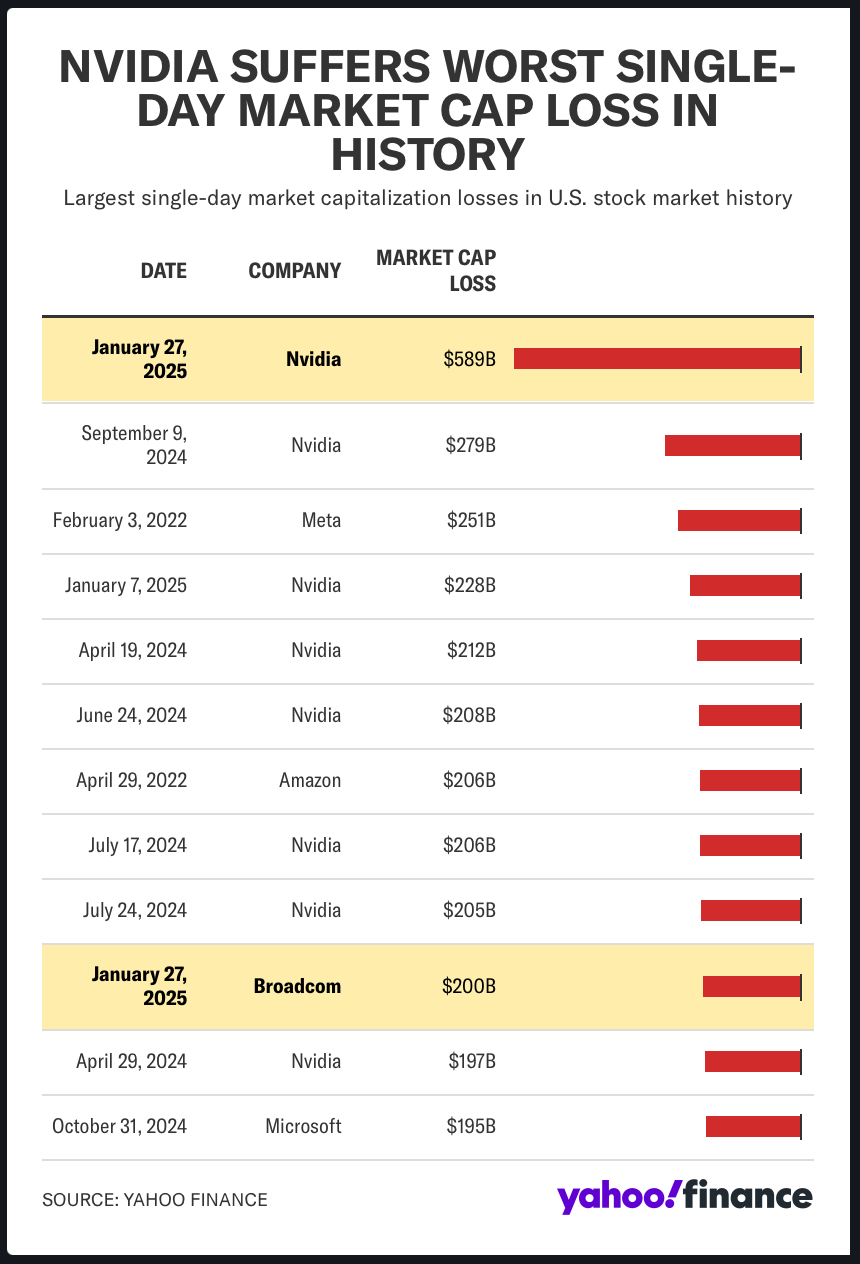

DeepSeek already demonstrated this. On January 27, 2025, the release of its R1 model — developed for just $5.6 million in reported compute costs, against the hundreds of millions spent by American labs — wiped $588.8 billion in Nvidia market capitalization in a single day.

January 27, 2025: DeepSeek R1 erases $588.8B in Nvidia market cap in one day — the largest single-day loss in US stock market history. Source: Yahoo Finance

DeepSeek did not destroy that value by accident. It destroyed it because it demonstrated that the technological moat underpinning the entire American AI ecosystem’s valuation may be far thinner than markets had priced in.

A US AI crash would give China a window — perhaps three to five years — to consolidate as the dominant technological power, at a moment when American labs would be in survival mode and public AI investment would be politically frozen.

Europe is in the worst possible position in an AI bubble scenario: it pays the consequences without having built the underlying asset.

The structural dependency is documented. The vast majority of European cloud spending flows to American providers. Nearly all frontier AI compute depends on chips designed in the US and manufactured in Taiwan. European public AI investment is a tiny fraction of America’s.

But Europe has strategic assets it is not using adequately — and a time window that is closing. Here are four concrete moves, designed specifically for the moment after the bubble bursts, which is exactly when Europe would have maximum leverage at minimum cost.

Move 1 — A European Sovereign Fund That Buys Distressed Assets

When the dot-com bubble burst in 2001, those with liquidity bought internet infrastructure for pennies on the dollar. That same infrastructure became the backbone of Google, Amazon, and Facebook in the following decade.

Europe could create today — before the crash — a fund of €50-100 billion with an explicit mandate to invest during an AI correction: research labs with real technology but exhausted cash runways, physical data centers sold off by companies in distress, and talent — AI researchers and engineers laid off in post-bubble waves. OBSTACLE

Text within this block will maintain its original spacing when published

The US classifies AI as a strategic military asset. The CFIUS — the committee that reviews foreign investments in American companies — could block European acquisitions of US AI labs, particularly after Anthropic’s defense contracts. This strategy works best if accompanied by a credible European military independence plan.Move 2 — Conditional Purchase Agreements With TSMC — Sign Now, Activate Later

ASML, a Dutch company, holds the absolute global monopoly on the machines that produce advanced chips. But it makes the machines — not the chips. The chips are made by TSMC, which is Taiwanese.

If the bubble bursts and major American orders contract, TSMC will have excess production capacity for the first time in years. That moment — and only that moment — is when Europe holds genuine negotiating power for long-term agreements at favorable prices.

The move: negotiate conditional agreements with TSMC today that activate automatically if American orders fall below a defined threshold. It is a financial option applied to chip geopolitics. It costs almost nothing now. It is worth a great deal at the right moment.

Move 3 — Public Options on European Private Data Centers

Between 2026 and 2031, an estimated €176 billion in private investment is expected to flow into European data centers — built by Nebius, CoreWeave Europe, Microsoft Azure, and others. If the bubble bursts, many of these could become enormously expensive, underutilized structures that private operators cannot afford to maintain.

The move: insert public option clauses into the public-private financing contracts of these data centers today. If a private operator runs into difficulty, the state — or EuroHPC — holds a right of first offer to acquire the structure at book value, not at an inflated market price. A potential private default becomes public infrastructure, without paying the speculative premium.

This is exactly the mechanism many European governments used with banks in 2008: not waiting for failure and then conducting a disorganized bailout, but having the legal right of succession already written into the contracts.

Move 4 — The AI Act as an Export Standard, Not a Compliance Cost

The European AI Act enters full effect on August 2, 2026. Most of the debate treats it as a cost burden on European companies. This is the wrong reading.

If trust in American AI models erodes after a bubble burst — for reasons of cost, reliability, or reputational damage — the AI Act becomes a competitive advantage. Companies globally that must choose an AI provider will prefer one certified to European standards: not because they are more enlightened, but because it is defensible to their own boards and regulators.

The move: negotiate mutual recognition agreements for the AI Act with Japan, South Korea, Canada, and Australia before the burst happens. Build a coalition of countries adopting the European standard, so that when the market looks for alternatives to American providers, the European ecosystem is already certified for 1.5 billion people — not just the 450 million of the internal market.

The common thread across all four moves is one: stop playing defense and start treating an American correction as a transfer of opportunity toward those who prepared the ground in advance.

Sources

Matt Stoller, “What Would It Look Like If the AI Bubble Popped?” — BIG Newsletter / Substack

David Cahn, “AI’s $600 Billion Question” — Sequoia Capital (June 2024): sequoiacap.com/article/ais-600b-question

Ed Zitron / Financial Times — OpenAI 2025 financial leak (June 2026): finance.yahoo.com

Nick Wade, “The AI Installation Bubble” — Substack (June 2026): nickwade.substack.com

Dean Baker, “The AI Bubble Monitor” — Center for Economic and Policy Research

Julius Baer, “Beyond the Bubble: Why the AI Investment Cycle Could Be Built to Last”

Janus Henderson, “AI versus the Dot-com Bubble: 8 Reasons the AI Wave Is Different”

INSEAD Knowledge — circular financing analysis, Nvidia/OpenAI

Financial Times, “Tech Groups Shift $120bn of AI Data Centre Debt Off Balance Sheets”

Federal Reserve, Financial Stability Report — Spring 2026: federalreserve.gov/publications/files/financial-stability-report-20260508.pdf

Man Group Research — chip obsolescence vs. loan useful life analysis

ORF Online — geopolitical analysis of AI bubble and China

Calcbench — Amazon 10-K, server useful life change 2024

Seeking Alpha — AI capex and US GDP contribution

Within Intelligence, “Private Credit Outlook 2026”: withintelligence.com

European Commission, AI Continent Action Plan / InvestAI: digital-strategy.ec.europa.eu

⚠️ This article is for informational and journalistic purposes only. It does not constitute financial advice.

Thank you for reading! I’d love to hear your thoughts. If you’d like to read more articles like this, let me know in the comments!

Cheers

Federico Zebele