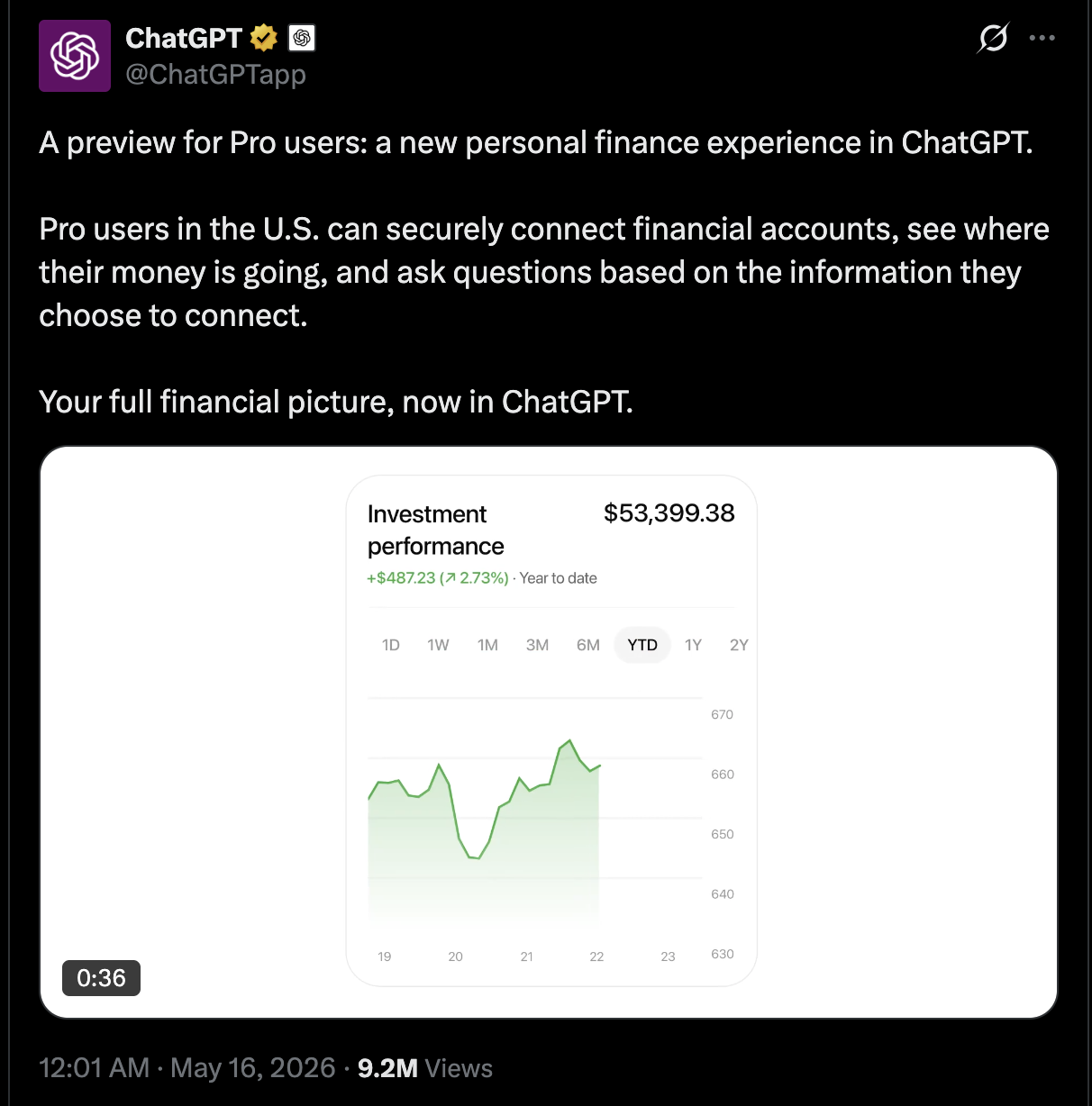

Last night, OpenAI officially launched a new personal finance experience preview for ChatGPT Pro users in the United States.

This feature allows users to securely connect personal financial accounts, view fund flows through a dedicated dashboard, and ask ChatGPT for personalized advice based on their financial situation. Users retain control over core information throughout the process. It is currently being piloted with a small group of users and will be gradually optimized and expanded.

OpenAI stated that conversations with linked financial accounts will follow the same model training settings as regular ChatGPT. This means that unless users opt out, OpenAI can use these conversations as training data.

OpenAI stated that money profoundly affects every aspect of people's lives, from housing choices and family care to future planning, all closely tied to financial status. However, in the current financial management landscape, users often need to consolidate multiple accounts, applications, credit cards, and loan information, even resorting to spreadsheets, just to barely grasp their overall financial picture, let alone make subsequent planning decisions.

So the core highlight of the newly launched personal finance feature is that it combines GPT-5.5's reasoning capabilities with users' actual financial situations, personal goals, lifestyle, and priorities, helping users discover financial patterns, weigh the pros and cons of decisions, and provide more personalized and comprehensive financial planning advice. Users can consult this feature for various specific financial issues, such as consumption change analysis, medium- and long-term savings plan formulation, etc. However, OpenAI explicitly states that this feature is for informational reference only and cannot replace professional financial advice.

OpenAI gave some specific examples:

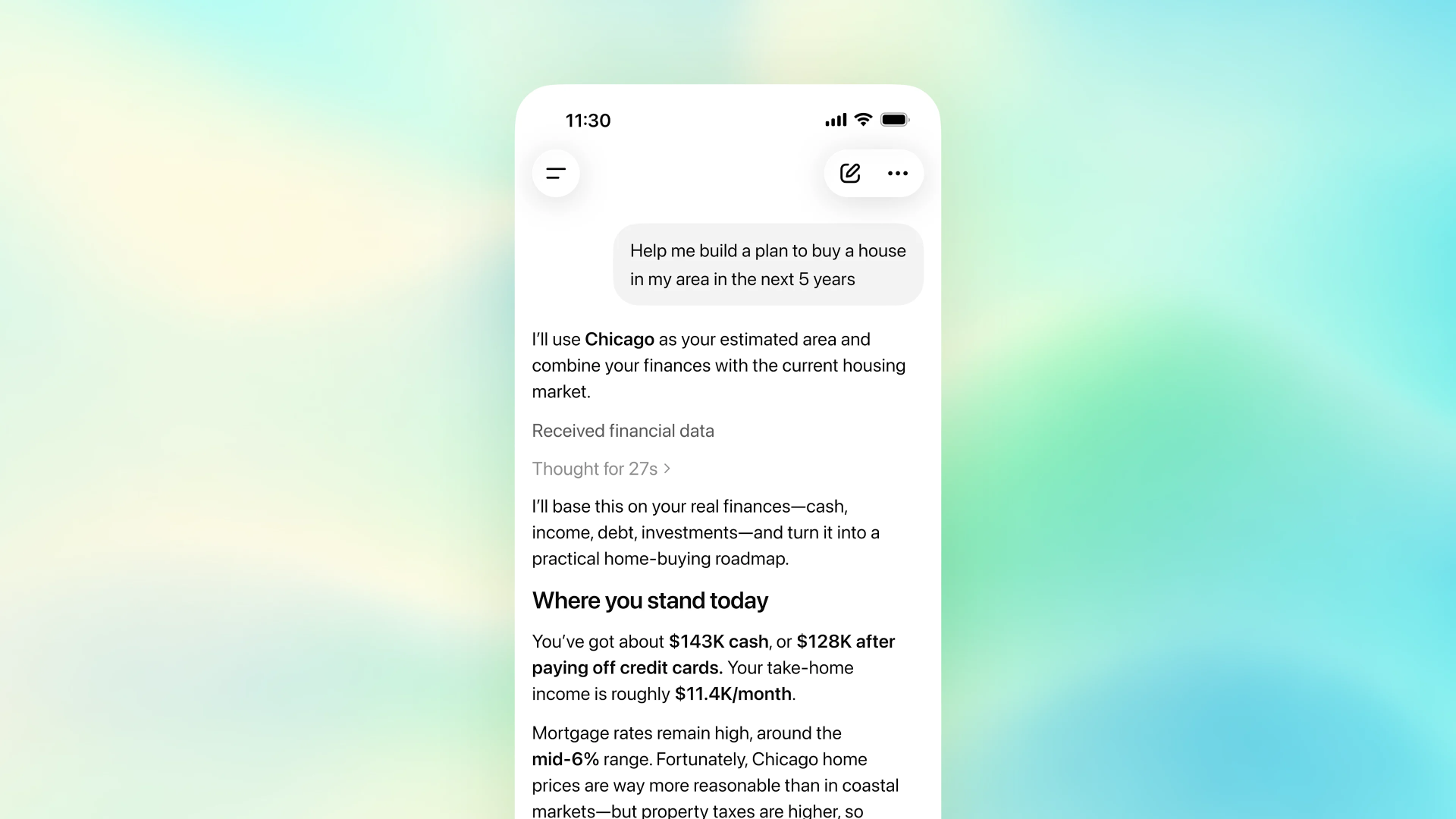

This personal finance assistant can help you plan your expenses. For example, if you want to buy a house within 5 years, you can ask it for advice.

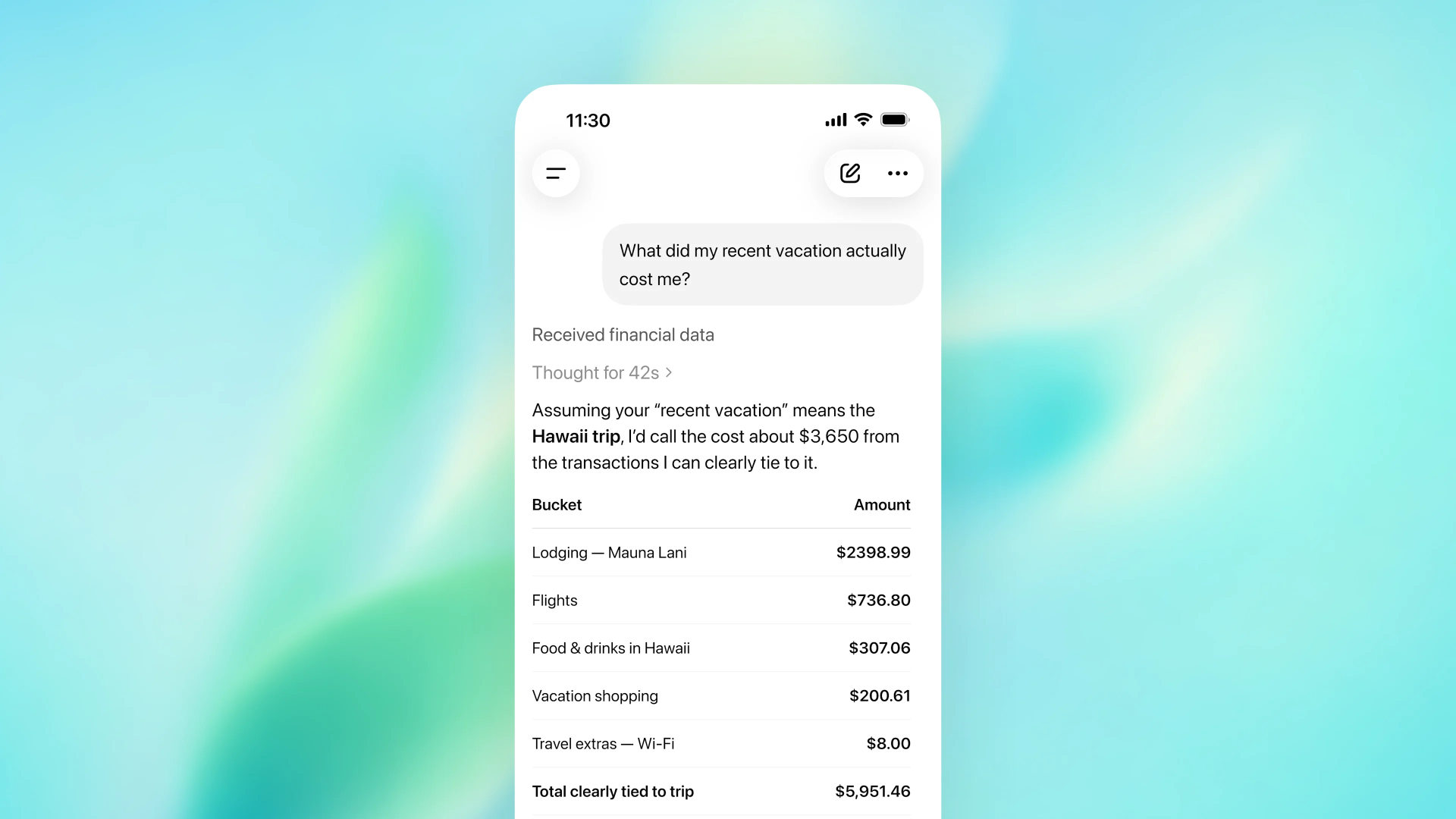

Not sure how much a trip actually cost? It can provide you with a clear bill.

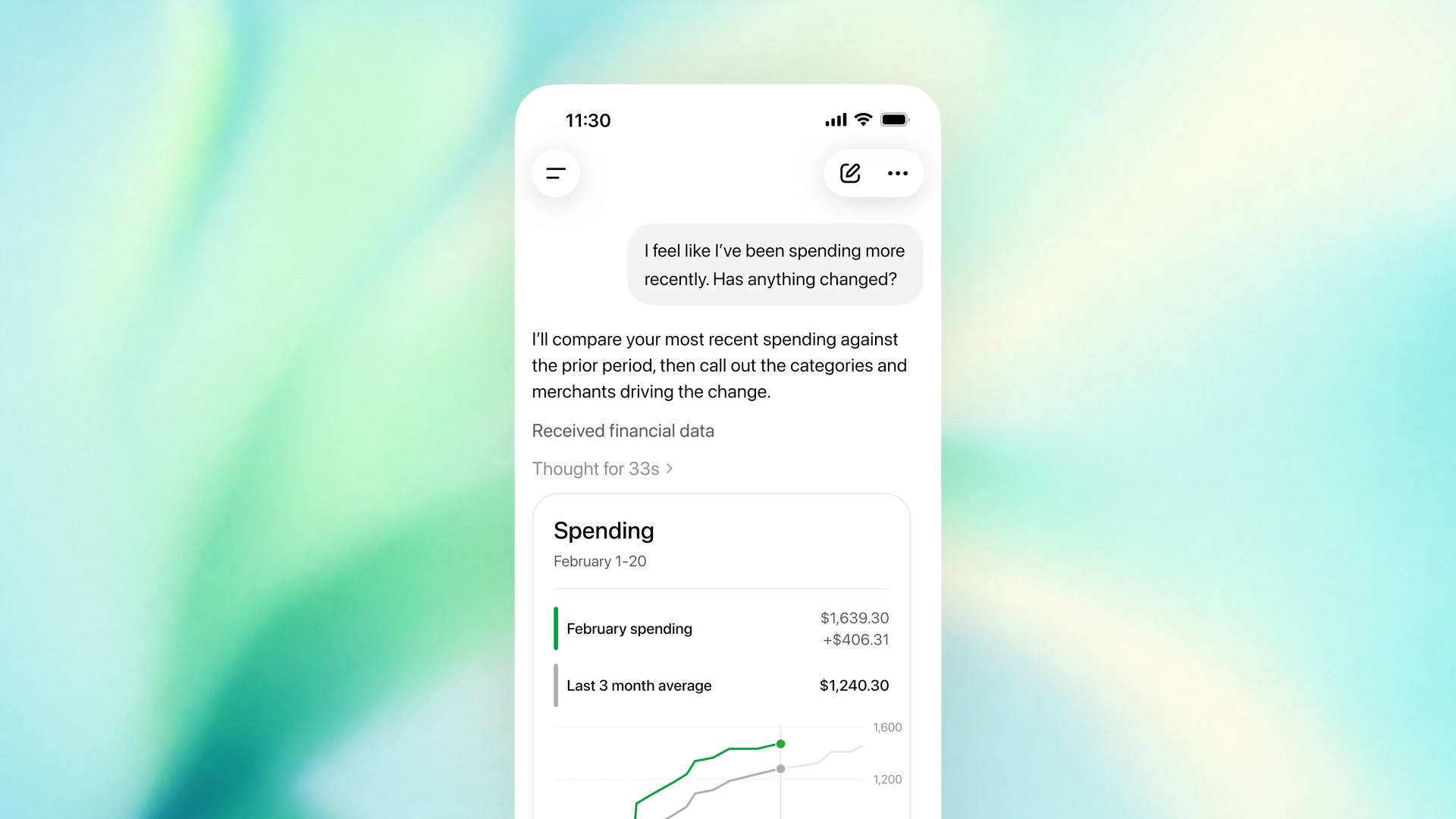

Or if you've been spending too much recently, have it check where you can save.

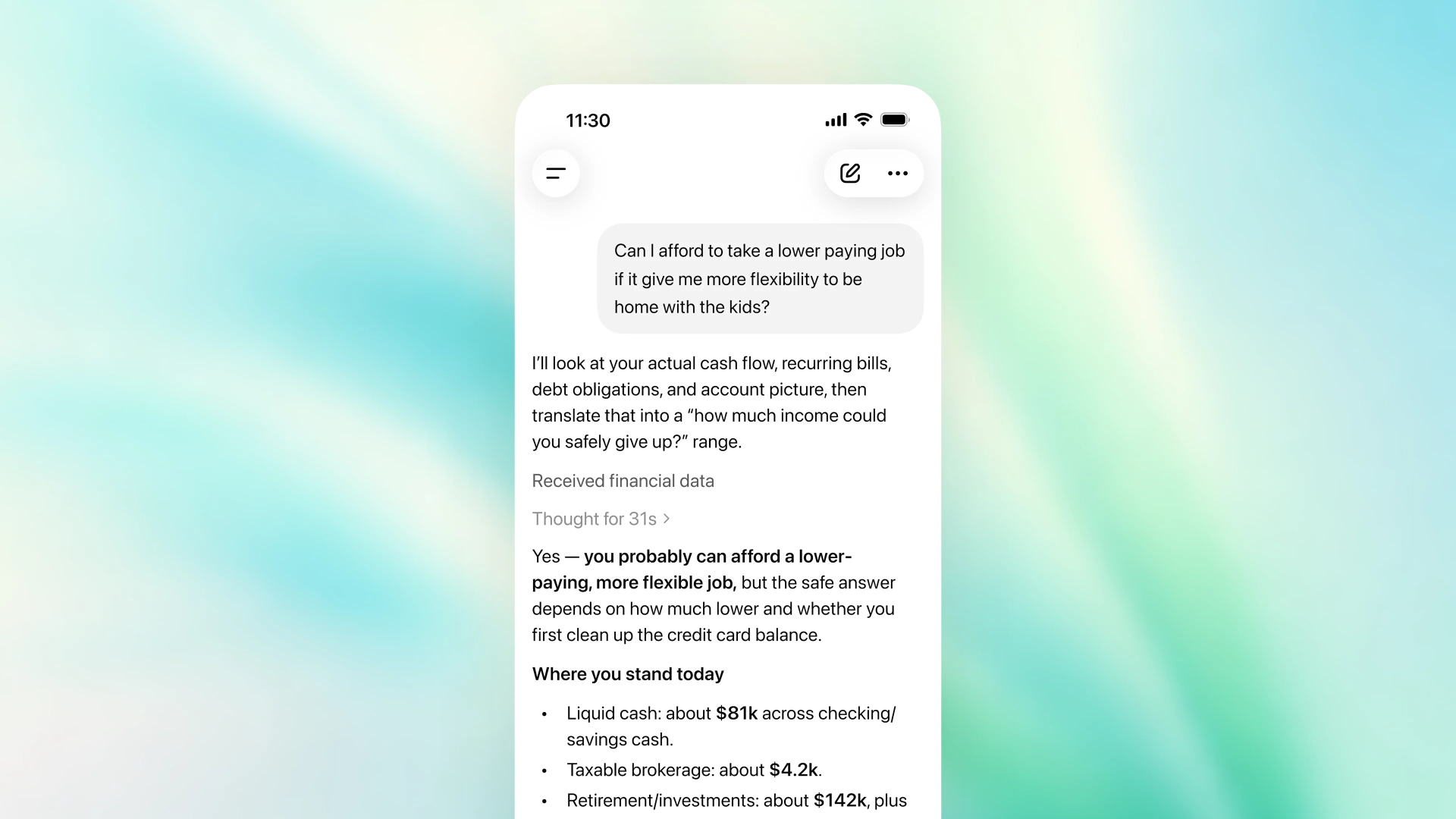

It can also help you set up a financial hypothesis, such as: given my current financial situation, can I take a lower-paying job to have more time and freedom to be with my children?

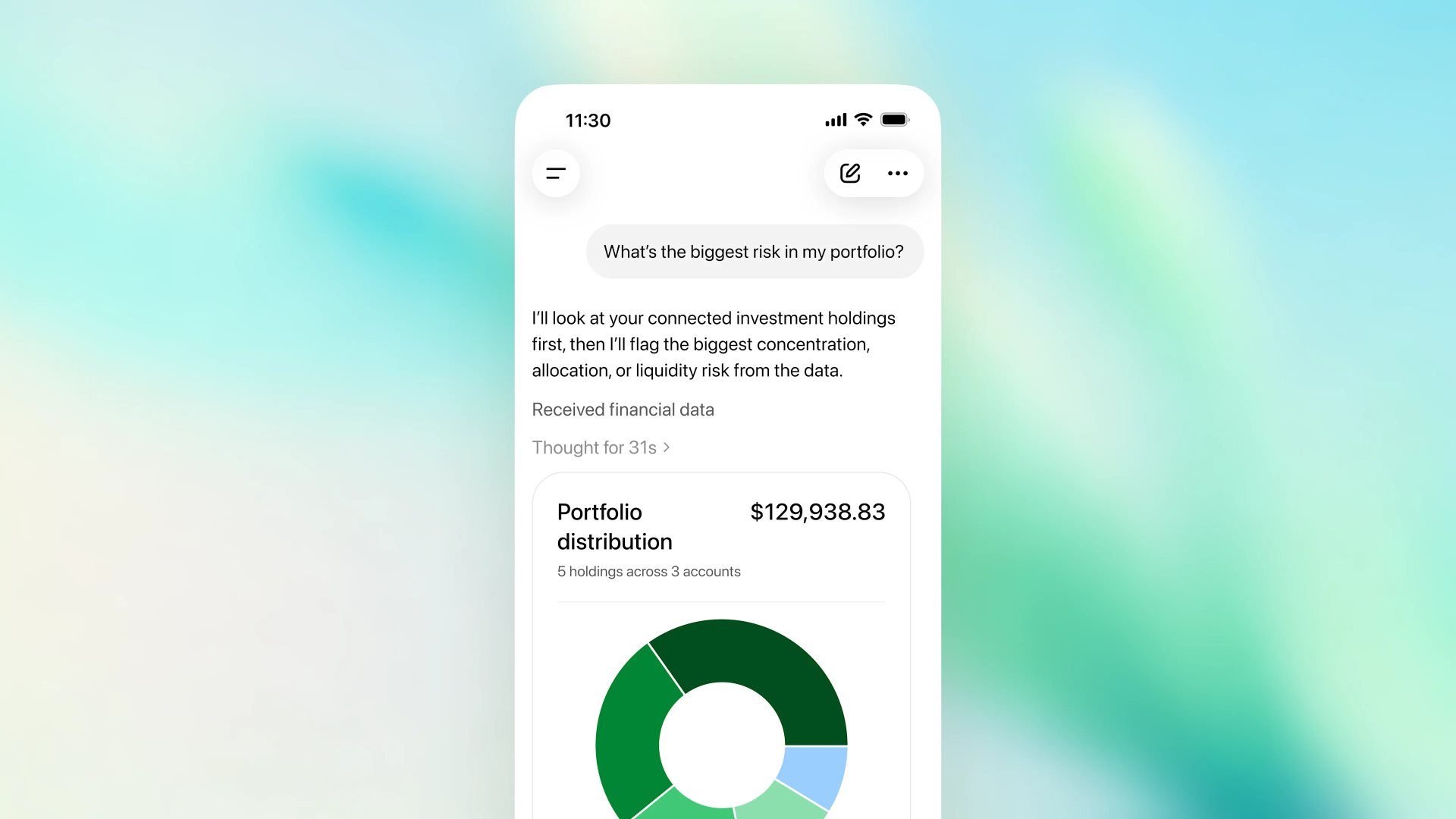

It can even give you warnings about investment risks in daily life.

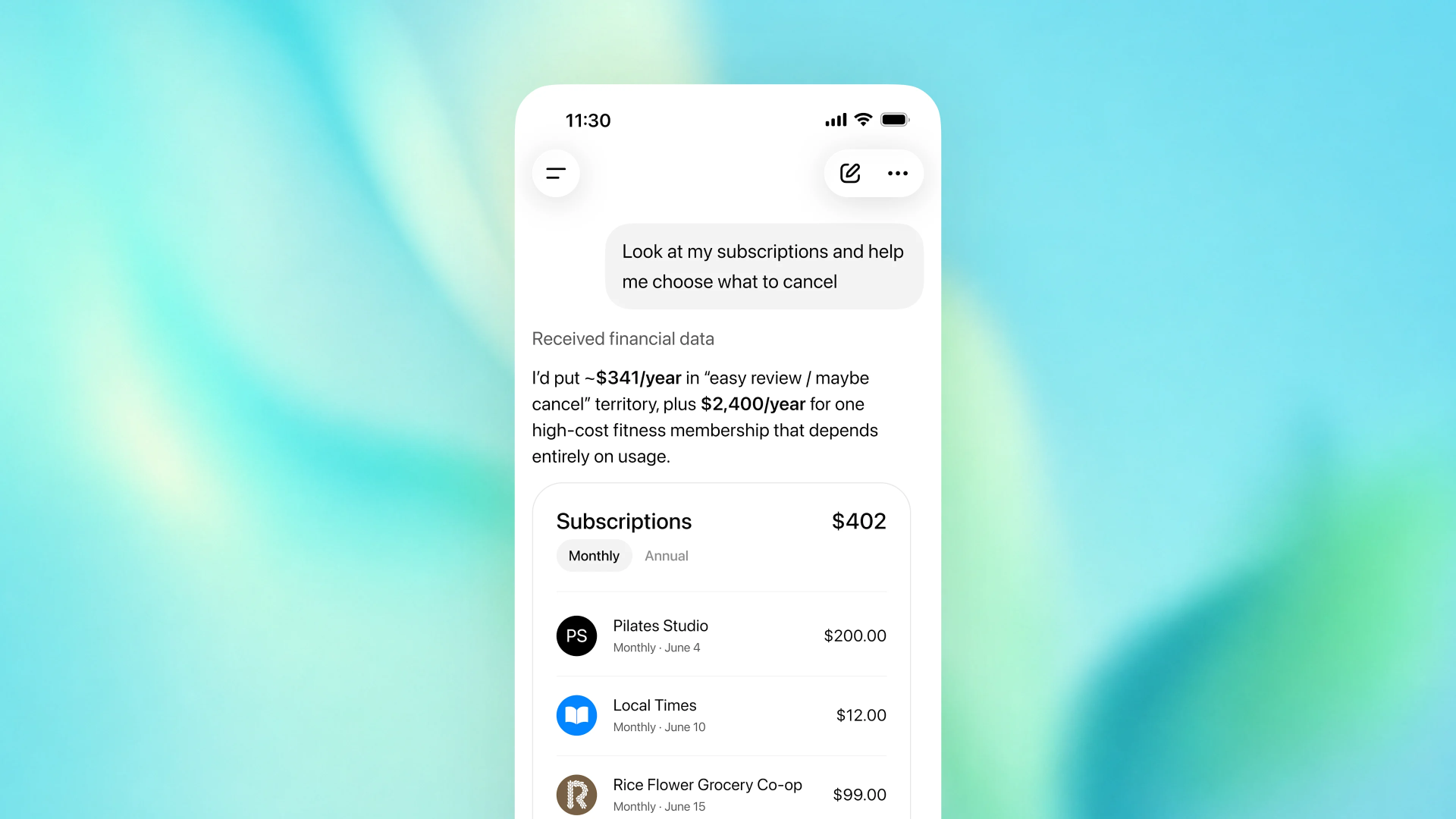

It can also help you review which subscription services you are wasting money on.

According to statistics, over 200 million users per month already use ChatGPT for budget planning, investment advice, investment path comparison, and future financial goal planning. The latest progress of the GPT-5.5 model has further enhanced ChatGPT's ability to handle complex, contextual issues in the personal finance domain, laying the technical foundation for this new feature launch.

It is reported that this financial feature has been simultaneously launched on the ChatGPT web version and iOS version, currently only open to Pro users in the United States, supporting account connections for over 12,000 financial institutions.

OpenAI plans to continuously optimize the experience based on early user feedback, and will gradually roll it out to Plus users, eventually achieving the goal of making it available to all users.

The launch of this feature comes just one month after OpenAI acquired the team of personal finance startup Hiro in April this year. The financial expertise of the Hiro team provided support for the development of this feature.

So, how is ChatGPT's new feature different from existing budgeting platforms (such as Rocket Money and Monarch)?

In a nutshell, ChatGPT remembers important user information and keeps it in mind when answering questions, but does not perform any actions.

OpenAI product manager Ty Geri said in a briefing that these new features will help “connect your personal financial situation with your broader personal life situation.”

Geri said that if you ask ChatGPT to find unnecessary subscription services, the assistant will use the information it already has about you to make recommendations.

In the briefing, OpenAI emphasized that ChatGPT only has permission to read users' financial information; it can only analyze data, not actually handle users' funds, such as making investments or canceling subscriptions. These actions still need to be done by the user.

So how do you use it?

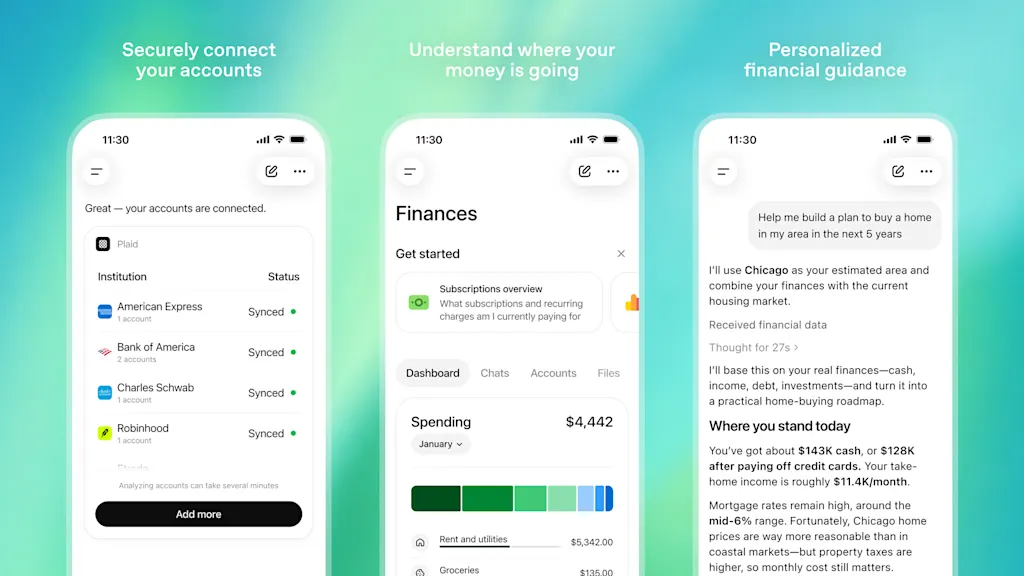

According to OpenAI, starting this financial experience is very straightforward. Users can open the "Finances" option from the ChatGPT sidebar and select "Get Started", or type "@Finances, connect my account" anywhere in the conversation to initiate the process. ChatGPT will guide users to securely link their financial accounts through the Plaid platform, with support for the Intuit platform coming later. After identity verification is complete, the system will sync and categorize the user's financial data, a process that takes approximately a few minutes.

The company stated in a press release that ChatGPT will be able to "access users' balances, transaction history, investments, and liabilities to help them better understand their financial situation or answer their questions."

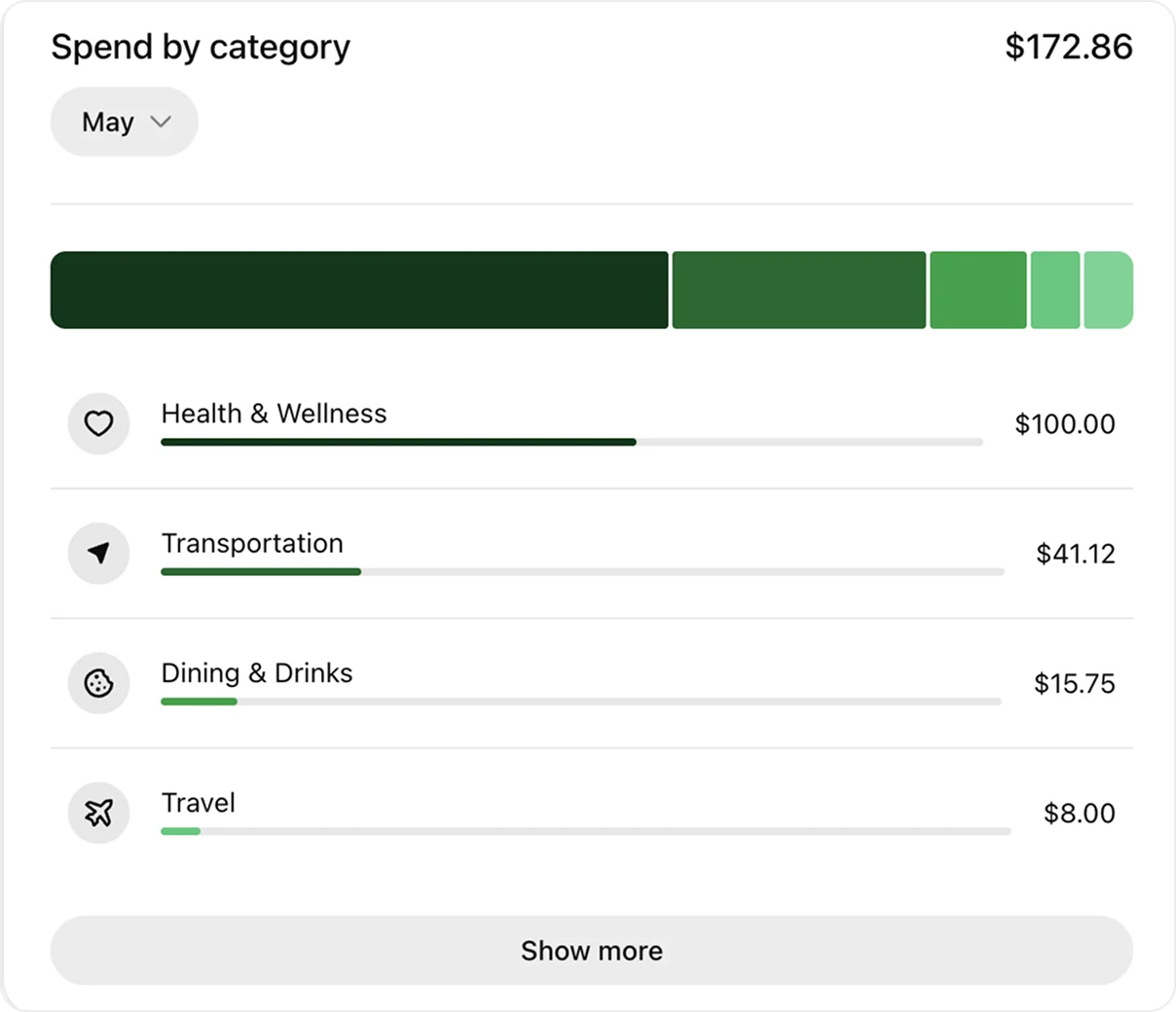

Once the account sync is complete, users can view core financial information in real time through a dedicated dashboard, including investment portfolio performance, spending details, subscriptions, and upcoming payments.

In addition to linked accounts, users can also proactively share personalized financial information such as mortgage details, savings goals, and planned large expenses. This information will be saved in "Financial Memory" for reference in future conversations, allowing ChatGPT to provide more targeted guidance by combining account data with user needs.

For the purpose of realizing the financial service closed loop "from answers to actions", OpenAI is joining hands with ecosystem partners such as Intuit. With the technical support of Intuit, users can complete a series of operations within the ChatGPT platform, ranging from credit card recommendations, approval probability inquiries, and application submissions, to stock sale tax impact consultations, tax estimations, and scheduling real-time consultations with local tax experts, thus achieving a seamless connection between financial advice and actual actions.

Regarding the privacy and security of financial data, OpenAI has made a clear commitment to put user control first. After linking accounts, ChatGPT can only access the user's account balance, transaction records, investment and liability information, but cannot view the full account number, nor perform any operations on the account.

To further explain its security, OpenAI also stated that users can disconnect the account connection at any time through "Settings">"Apps">"Finance" or the "Finance" page. After disconnection, the synced account data will be deleted from the OpenAI system within 30 days, and it will not affect the financial information in the conversation history. Users can also delete the relevant conversations individually.

At the same time, users can view or delete content in the "Financial Memory" on the "Finance" page; when using the temporary chat feature, ChatGPT will not access the linked financial accounts, and temporary chat records will not be retained. In addition, users can enable multi-factor authentication (MFA) to further enhance account security.

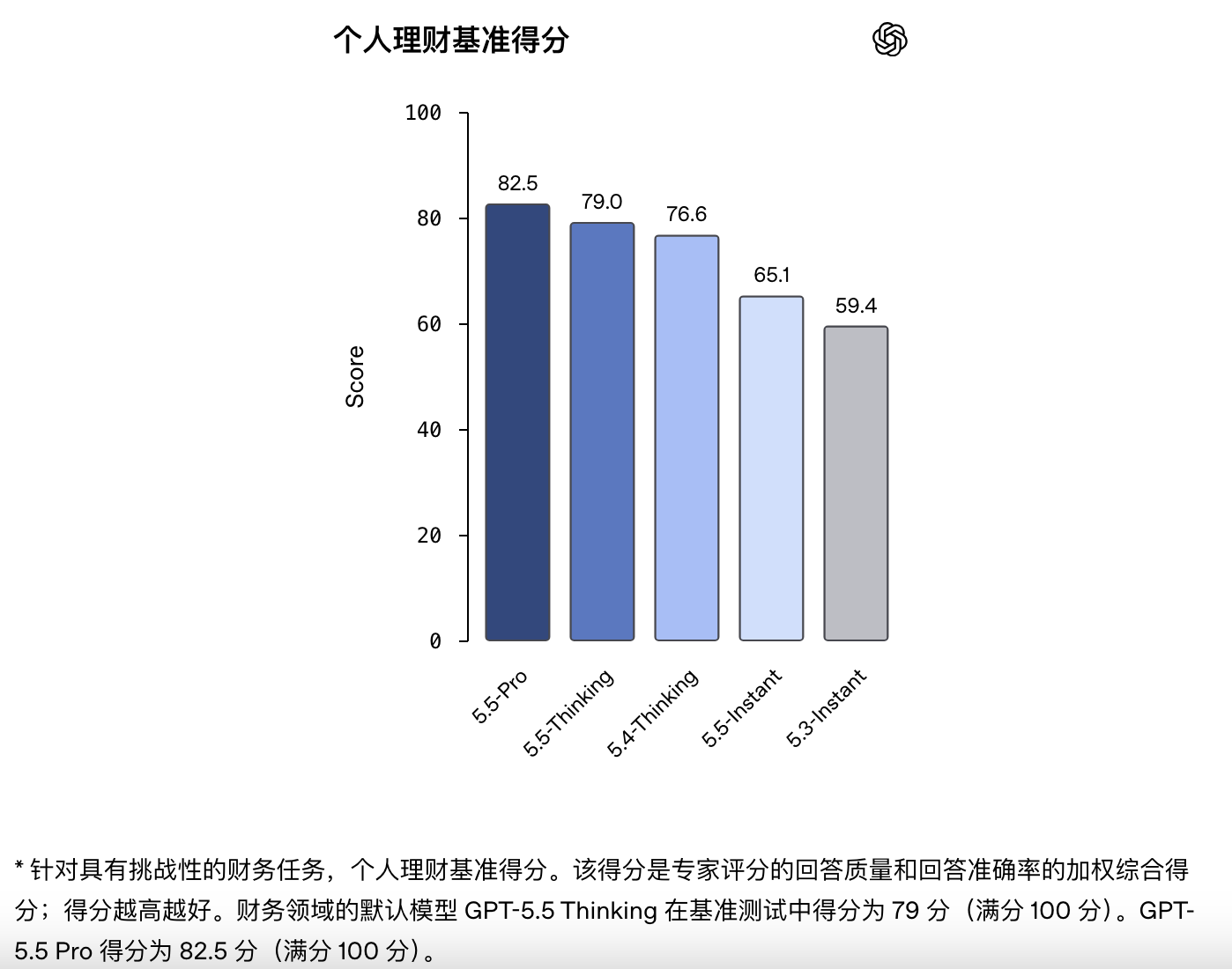

To ensure the accuracy and quality of financial advice, conversations related to linked financial accounts default to using the GPT-5.5 Thinking model—OpenAI's latest reasoning model. OpenAI has also established an internal evaluation benchmark, collaborating with over 50 financial professionals from leading institutions to comprehensively assess ChatGPT's performance on complex personal finance tasks.

Finally, OpenAI also emphasized that the model underpinning this new feature is its most advanced GPT-5.5 Thinking model.

Evaluation results show that GPT-5.5 Thinking outperforms previous models in complex financial tasks, with the GPT-5.5 Pro model available to ChatGPT Pro users performing the best.

In a benchmark test for personal finance on challenging financial tasks, GPT-5.5 Thinking scored 79 out of 100, while GPT-5.5 Pro scored 82.5 out of 100, with the score being a weighted composite evaluation by experts based on answer quality and accuracy.

After ChatGPT launched its personal finance feature, the internet quickly split into two camps over the idea of "letting AI take over your wallet."

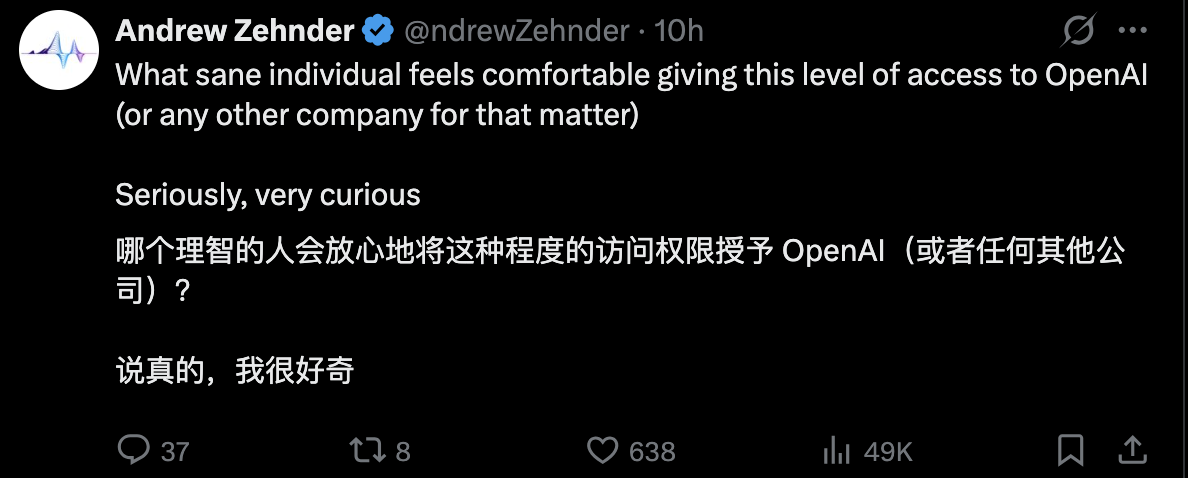

One camp's first reaction was almost instinctively wary. Some bluntly said: "Handing over bank account permissions to AI seems crazy to me. Thanks, but no thanks. Some data should just stay private forever."

In their view, chat history, search preferences, and daily habits are already enough for platforms to sketch user profiles, but once financial accounts are integrated, AI would grasp not just interests and preferences, but a person's most core asset flows, consumption structures, and even risk tolerance. For many, this has crossed the line from technological convenience into the non-negotiable realm of privacy.

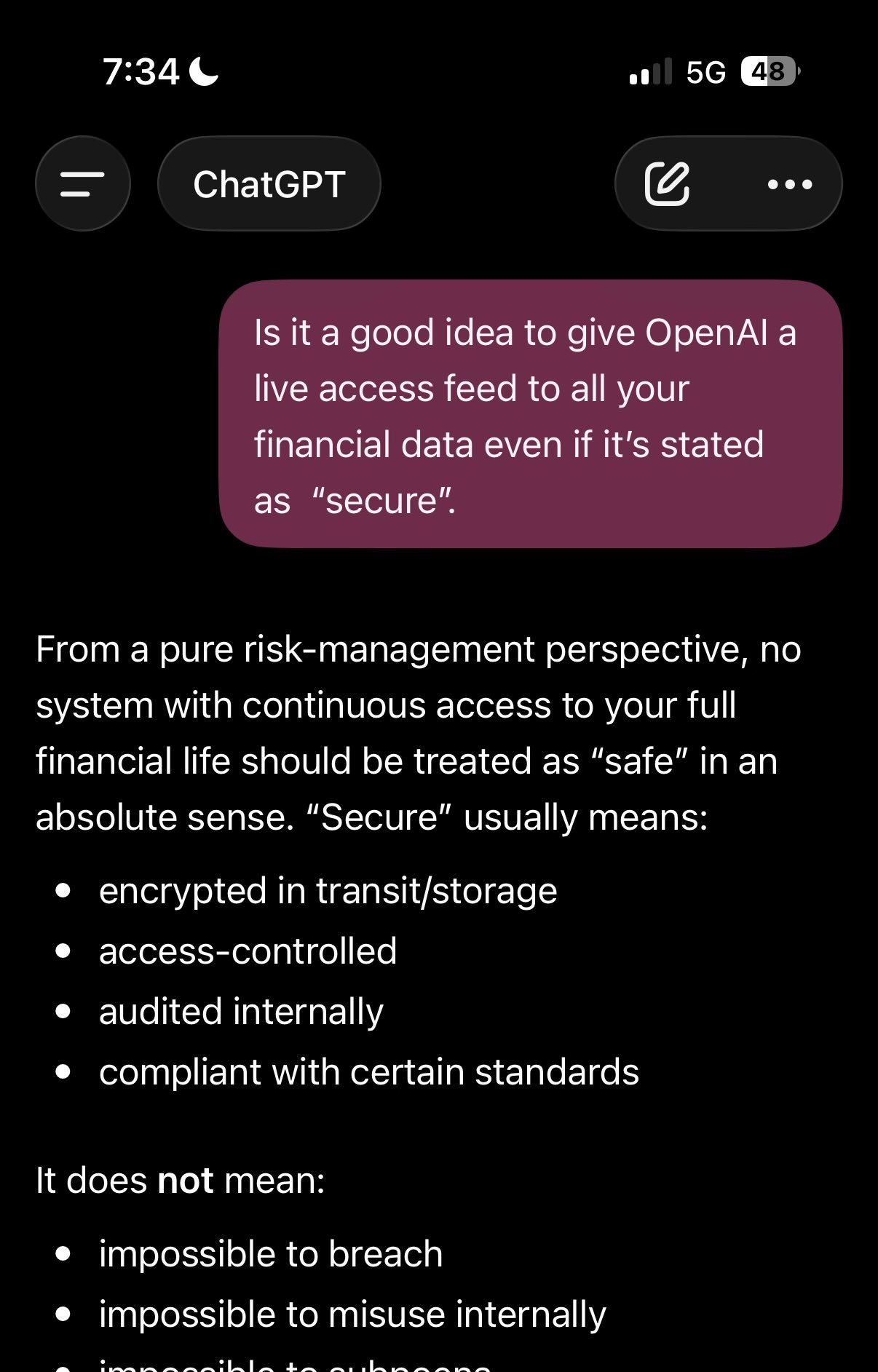

Another user shared a screenshot of his conversation with ChatGPT, in which he asked ChatGPT: Even if it claims to be "safe," is it a good idea to give OpenAI full real-time access to all your financial data?

ChatGPT replied: "From a pure risk management perspective, any system that has continuous access to your entire financial life should never be considered 'safe' in an absolute sense."

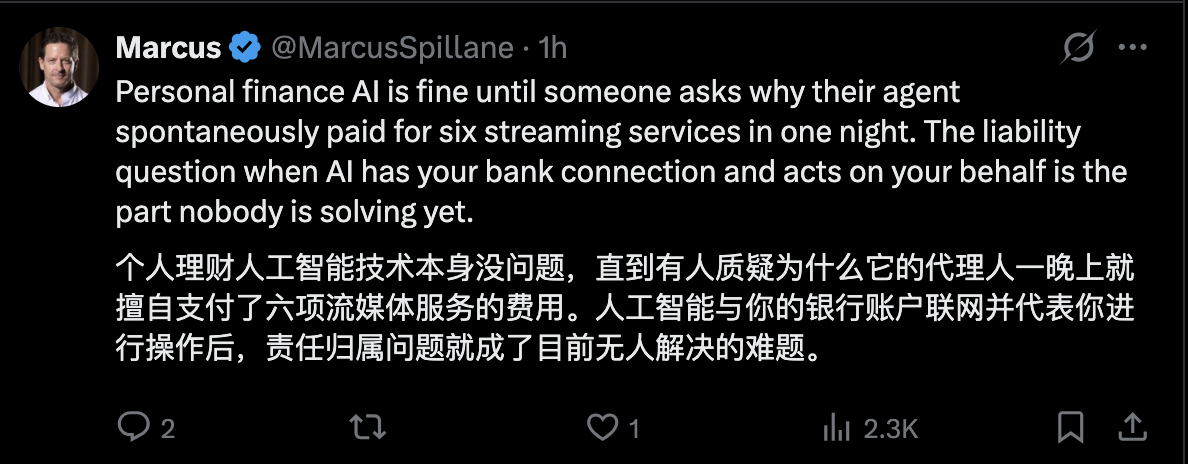

Another more realistic concern focuses on the issue of accountability.

Some commented that the personal finance AI technology itself is not the problem; the real issue is: if one day a user wakes up and finds that their AI assistant has, overnight, signed up for six streaming subscriptions without authorization and even completed the payment automatically, who bears the responsibility? Is it the platform's algorithm, the model's misjudgment, or did the user implicitly accept the risk by granting authorization? When AI no longer just provides advice but directly connects to bank accounts and performs actions on behalf of the user, existing accountability mechanisms are almost unable to cover this new type of scenario.

In other words, technology has already rushed ahead into reality, but the rule system is far from keeping up.

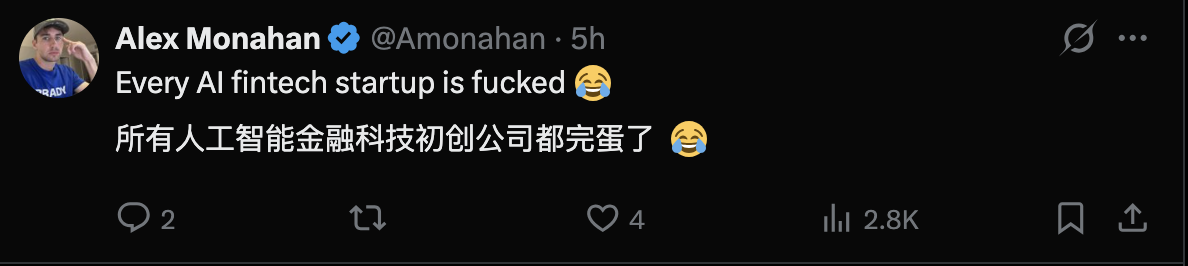

This concern has even led some to further deduce an industry impact. Some directly assert: "All AI fintech startups are doomed."

This is easy to understand. If platform products like ChatGPT begin to venture into personal finance, the moats of AI fintech startups that originally relied on selling points such as "helping users manage money," "helping users budget," and "helping users plan spending" will be rapidly eroded. After all, in the era of large models, users are likely to prefer entrusting their financial permissions to a super-entrance they already use daily, rather than downloading an additional vertical tool.

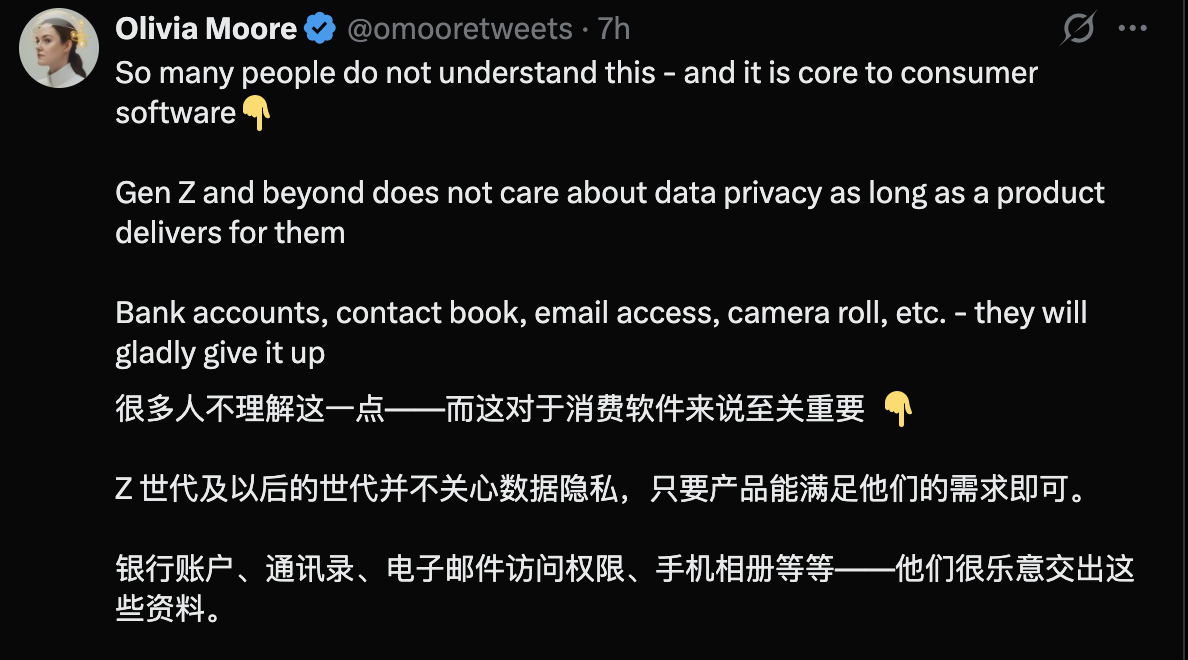

But the voices of supporters are equally strong, and the reasons they give are very clear: the younger generation simply doesn't care that much about privacy.

Some point out that many people don't truly understand the changes in this generation of consumer internet users.

For Gen Z and even younger users, the importance of data privacy is giving way to immediate value. As long as the product can actually solve problems, they are willing to hand over bank account permissions, contact lists, email access, and even phone photo albums. Privacy for them is not an absolute principle but a resource that can be exchanged—as long as the experience exchanged is smooth enough and the efficiency is high enough.

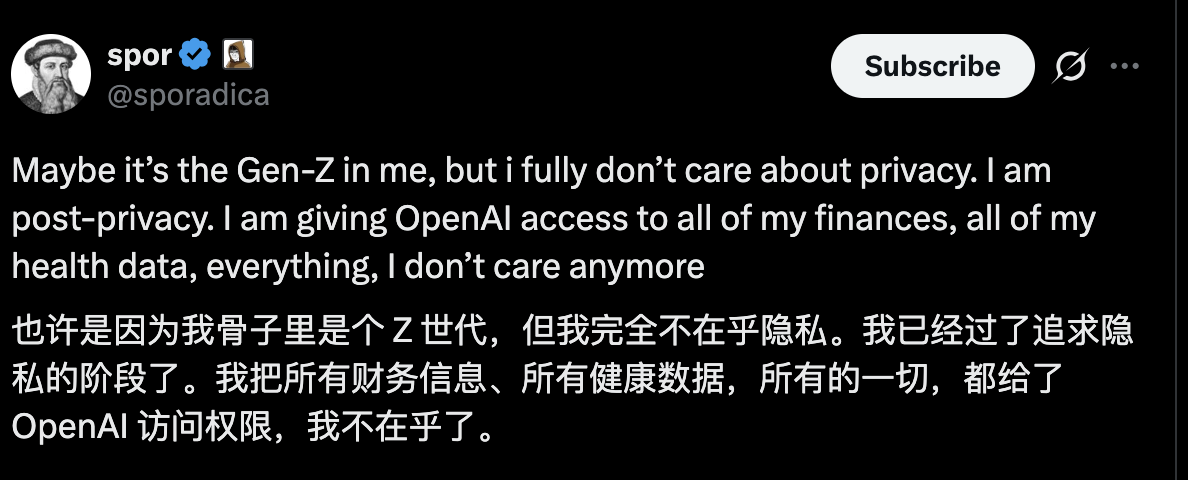

This attitude is even put more bluntly by some younger users. One person confessed: "Maybe it's because I'm Gen Z at heart, but I really don't care about privacy anymore. I'm long past the stage of agonizing over privacy. I've given OpenAI access to all my financial information, health data, almost everything. I don't mind."

Perhaps this is where the controversy truly deserves attention. On the surface, it's just a discussion about a new ChatGPT feature; on a deeper level, it reflects a clash of two digital-era values: one generation insists that "data belongs to the individual and must never be easily surrendered"; another believes that "privacy is essentially a cost of efficiency, and as long as the benefits are high enough, the exchange is completely justified."

And when large language models begin to extend from answering questions and generating content to managing user assets, understanding consumption habits, and even making financial decisions directly for users, a sharper question is already before everyone: When AI starts to pry into your wallet, are humans gaining a smarter assistant, or are they actively handing over their entire fortune?

Reference link:

This content is automatically aggregated by InertiaRSS (RSS Reader) for reading reference only. Original from — Copyright belongs to the original author.