In May 2026, Amazon launched Amazon Supply Chain Services, opening its multimodal freight, automated warehousing, and last-mile parcel delivery network to any company that wants to use it. The first publicly named enterprise customers are Procter & Gamble, 3M, Lands’ End, and American Eagle Outfitters.

Amazon spent $83 billion in capex in 2024, more than seven times the combined capex of UPS, FedEx, and the U.S. Postal Service. I know. Not all of that is logistics-related.

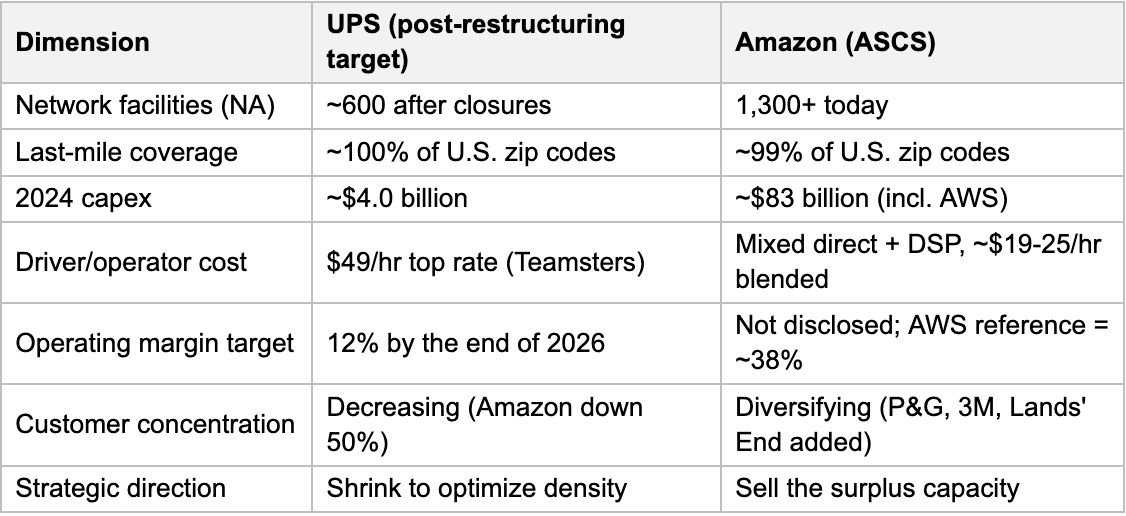

Read it next to the other parcel-economics story of 2026. On UPS’s January 27 earnings call, CFO Brian Dykes told investors UPS would eliminate up to 30,000 positions this year. In February, the company identified 22 union-staffed package facilities for closure, the next tranche of a plan to shut up to 200 facilities by 2030. Across that same window, UPS continued to draw down its Amazon volumes toward a 50% cut by mid-year.

The conventional read of Amazon Supply Chain Services (ASCS), “Amazon expands again,” misses what is happening.

The story is not about logistics.

It is about what Amazon does to its own cost centers, and what that has historically meant for everyone in the cost center next door.

Amazon has built three businesses by accident.

ASCS is the third.

Start with Amazon Marketplace.

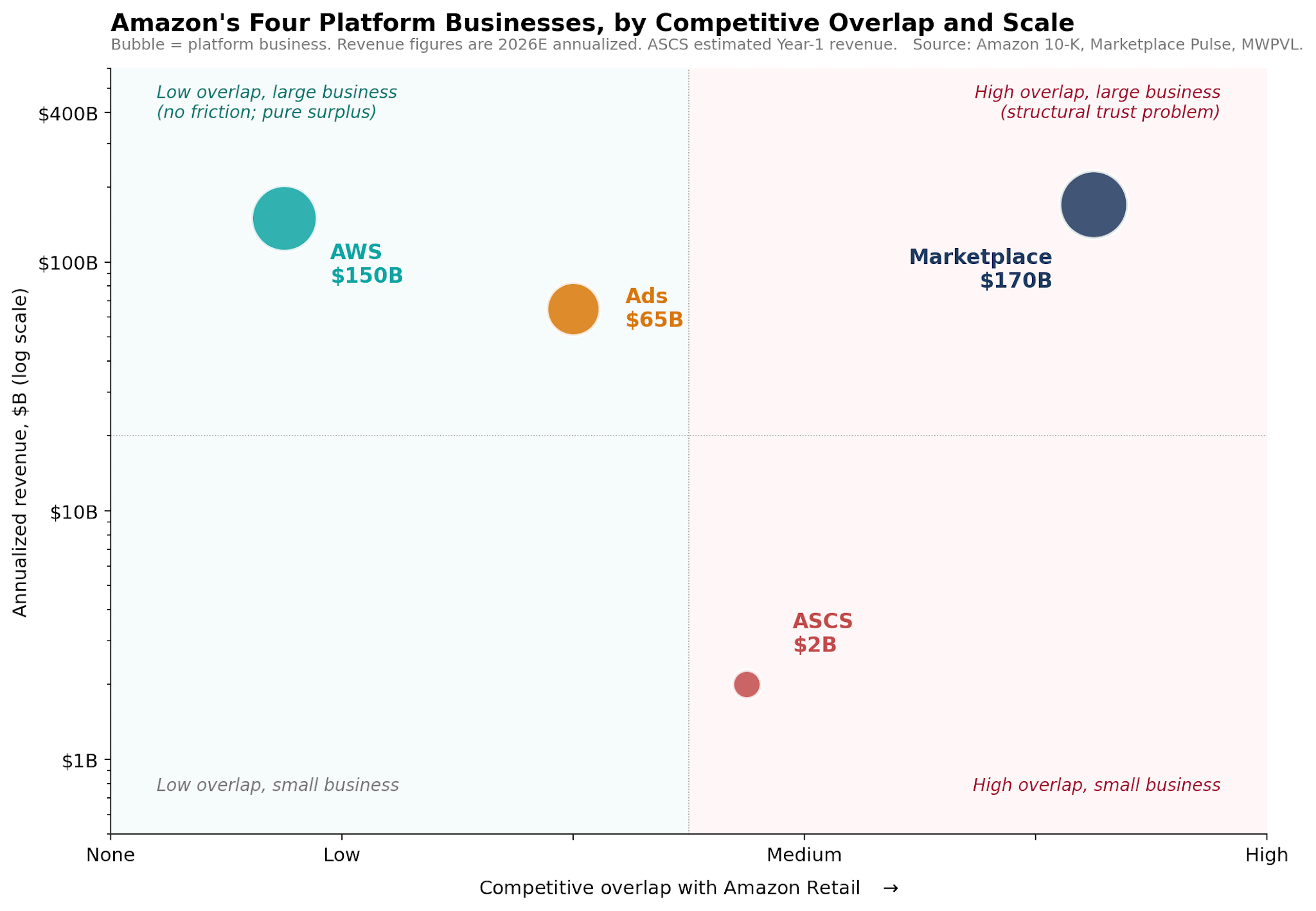

In 1999, Amazon decided to allow third-party sellers to list products alongside its own retail catalog. The internal logic was simple: Amazon had built the front-end to be the best in the world at converting intent into transactions and was not using that capability to its full potential. By the end of 2024, 62% of paid units on Amazon.com were sold by third-party sellers. The marketplace that began as a way to fill the catalog became the catalog.

Then AWS.

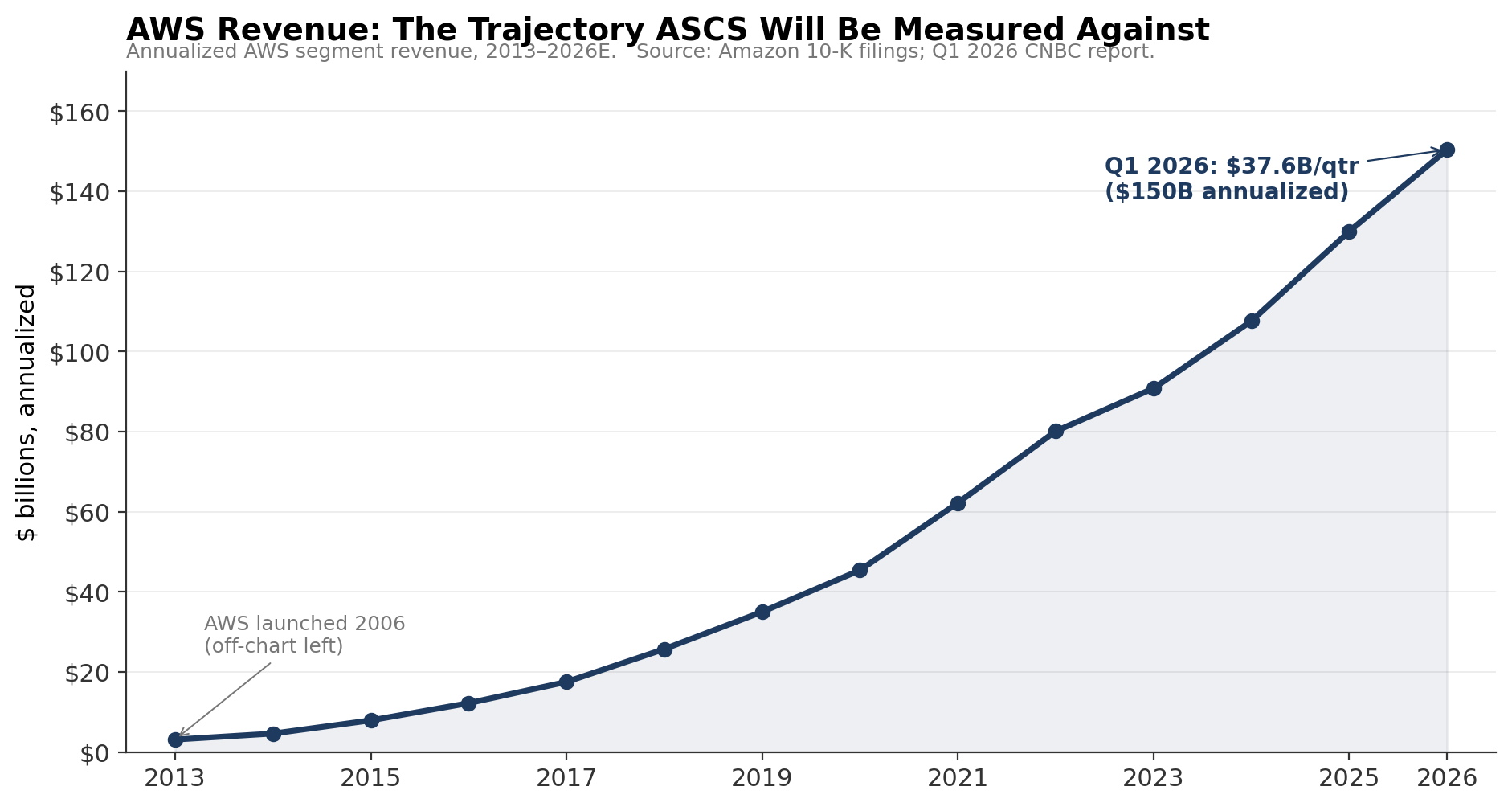

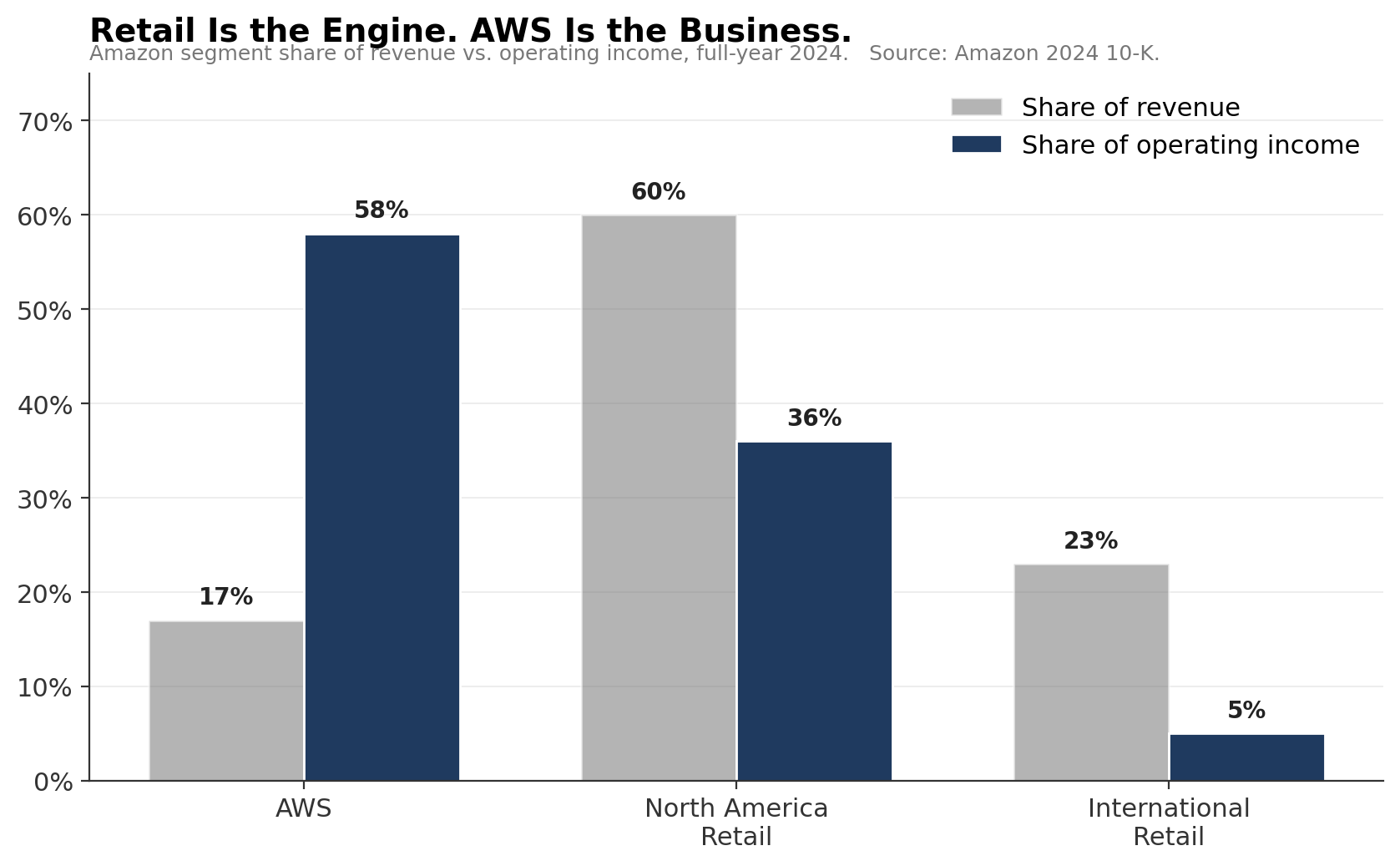

In 2006, Amazon launched what is now AWS, exposing the internal compute, storage, and database services its retail group had built. The internal pitch was identical to Marketplace seven years earlier. The marginal cost of letting a startup, then a bank, then a federal agency run workloads on the same fabric was a tiny fraction of what those institutions would pay to do it themselves. AWS in Q1 2026 reported $37.6 billion in quarterly revenue, roughly $150 billion annualized, with $14.2 billion in segment operating income and an operating margin near 38%.

Now ASCS.

The internal logistics network Amazon spent 15 years and more than $200 billion in cumulative capex building, including more than 1,300 facilities, an in-house air cargo operation, and last-mile delivery in 99% of U.S. zip codes, is being turned into an external service. The first enterprise customers are running per-unit cost comparisons against the alternative and discovering that the math does not add up.

The pattern is quite simple.

Build infrastructure to serve internal operations at a scale no rational external buyer would justify. Optimize it to a level that drives marginal cost below the buyer’s internal alternative. When the surplus capacity is too large to write off, open the API and sell it.

Each iteration, at launch, looked like a bad idea:

Marketplace would cannibalize retail margin.

AWS would expose infrastructure to competitors.

ASCS puts Amazon’s logistics network in the hands of brands that compete with Amazon.

Each time, Amazon decided the surplus capacity was worth more than the cannibalization risk.

Three things have to be true.

Scale that an external buyer cannot match: AWS spends $15-20 billion per quarter on cloud capex and runs higher utilization than any single tenant can; ASCS operates 1,300+ facilities, an air fleet, and same-day reach in almost every zip code.

Surplus capacity the parent cannot consume: AWS scaled externally because retail could not absorb the data-center commitments; ASCS launches now because retail growth has normalized, and the network was built for a holiday peak that has softened.

Cultural willingness to sell to competitors: P&G makes Pampers; Amazon Basics makes diapers. Most companies will not put their freight on the rails of a direct retail competitor. Amazon will, because by 2026, it has done it twice already, and the strategic math has worked both times.

The deeper question for any operating company is whether it has anything in its cost center that, run at an unreasonable scale and with the willingness to sell to a competitor, could attract external buyers. For most companies, the answer is no, because the cost center never reached the necessary scale.

That is the real moat: not the surplus, but the decades-earlier willingness to build the cost center at the scale that eventually produced the surplus.

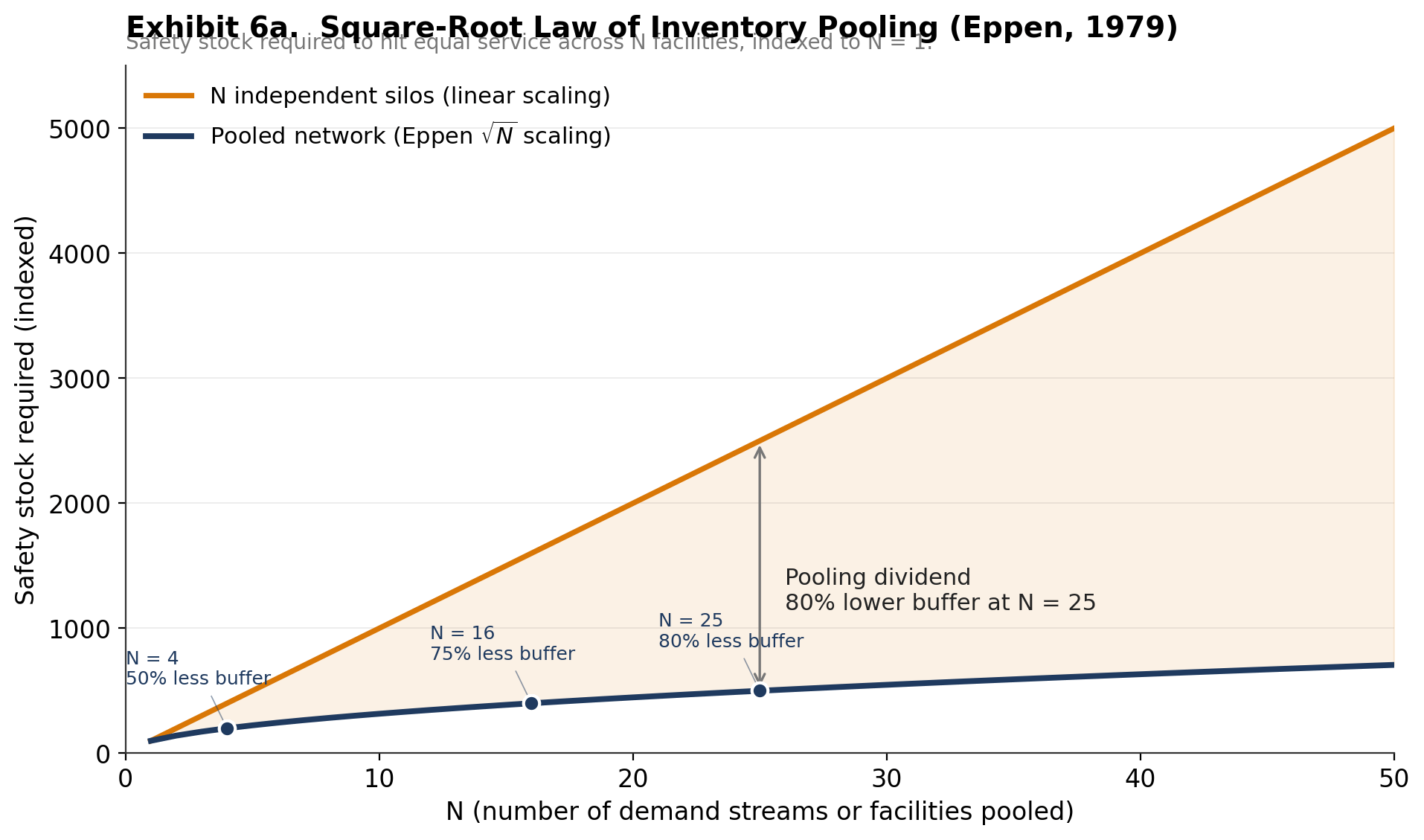

If there is one piece of operations theory that explains why Amazon’s cost-curve gap is structurally durable, it is the square root law of inventory pooling, formalized by Eppen, now standard in any operations textbook (the cleanest derivation can be found in my colleagues Cachon & Terwiesch’s book, Chapter 14 if you are really curious).

The result is simple, and students who took Operations Strategy with me know that I have real joy teaching it.

Take N facilities, each serving independent demand. The safety stock required scales linearly with N: it is proportional to N × σ.

Pool them into one centralized network serving the same demand, and the safety stock drops to √N × σ. The savings ratio is 1 − 1/√N. Quadruple the network and save half the buffer. Multiply N by sixteen, save three-quarters.

At N = 25, the pooled network needs roughly 80% less buffer to serve the same demand at the same service level.

The same √N scaling shows up in last-mile routing. The optimal tour through n stops in a fixed service area scales as √n, so the cost per stop falls as 1/√n.

The Amazon-UPS cost gap is not an operational gap. It is the gap between two points on the same curve.

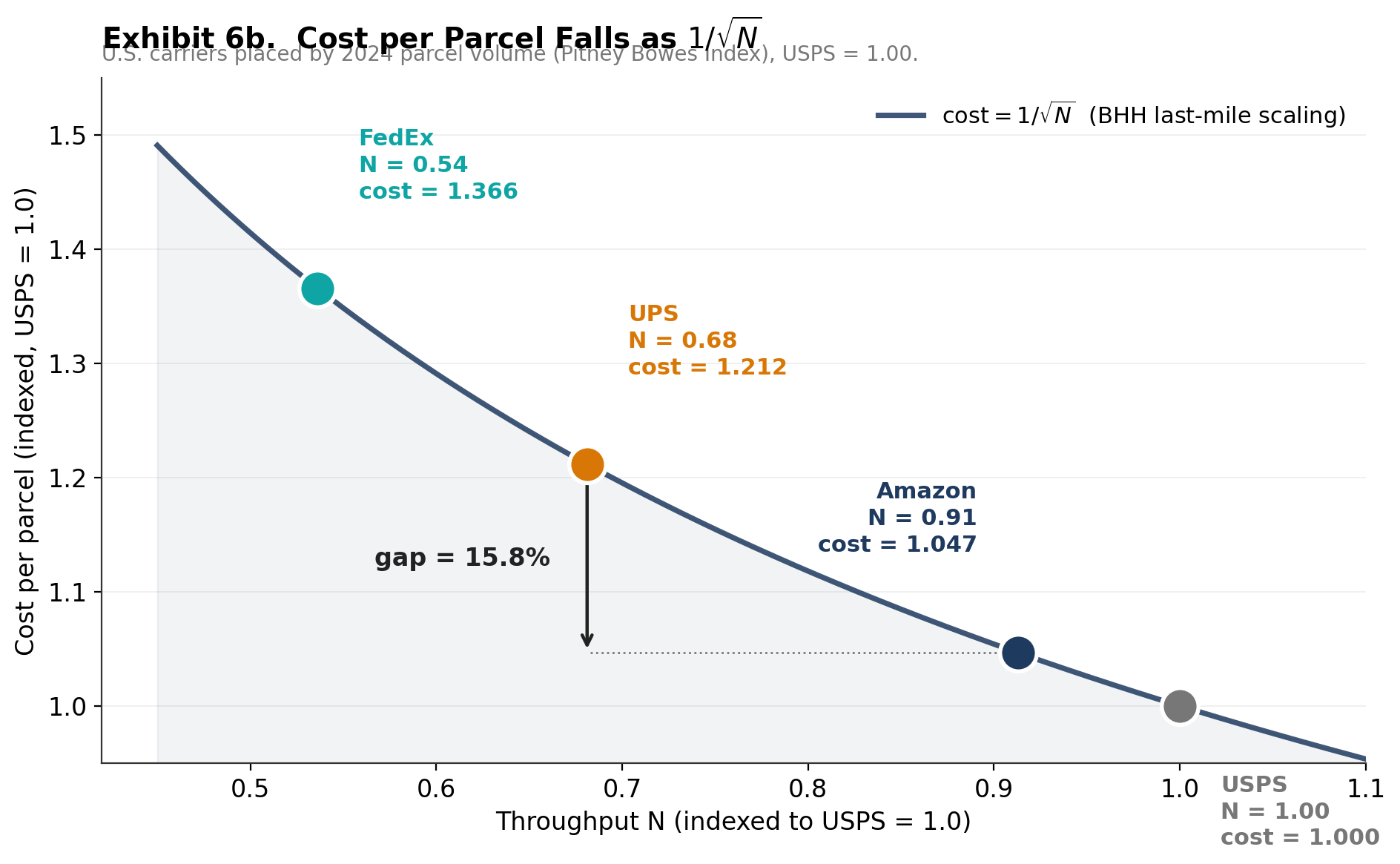

Let’s walk through the math (you can skip the next part, but if you do skip, are you even a real reader? Not judging. Just saying).

Take the 2024 Pitney Bowes parcel volumes: Amazon: 6.3 billion; UPS: 4.7 billion; USPS: 6.9 billion. Index each carrier to USPS = 1.00: N_Amazon = 6.3 / 6.9 = 0.913, N_UPS = 4.7 / 6.9 = 0.681.

Cost per parcel scales as 1/√N, so cost_Amazon = 1 / √0.913 = 1.046 and cost_UPS = 1 / √0.681 = 1.212 on the same index. The ratio is √(N_Amazon / N_UPS) = √(6.3 / 4.7) = √1.340 ≈ 1.158.

UPS pays about 15.8% more per parcel than Amazon for the simple reason that Amazon’s network moves 1.34× the volume across roughly the same geographic footprint.

That 15.8% is the structural floor. It does not depend on Amazon being better-run than UPS, only on Amazon being bigger. If UPS spent the next decade matching Amazon on every operational dimension, the floor would persist as long as Amazon’s volume grew faster, which it has every year since 2018.

The same law generalizes across every Amazon platform business. AWS pools demand variability across millions of customer workloads. Marketplace pools SKU discovery across millions of sellers. Amazon Ads pools impressions across the entire retail surface and Prime Video.

In each case, the marginal cost of serving an additional external customer falls along the √N curve while the marginal revenue is roughly linear. The gap is the operating margin.

ASCS productizes these effects in physical logistics. Adding P&G’s freight to a network already moving 6.3 billion Amazon parcels does not require a new network; it only adds throughput to a cost curve that improves as √N. P&G pays Amazon for a margin uplift, largely already generated by existing at that scale.

The cost gap is not subtle.

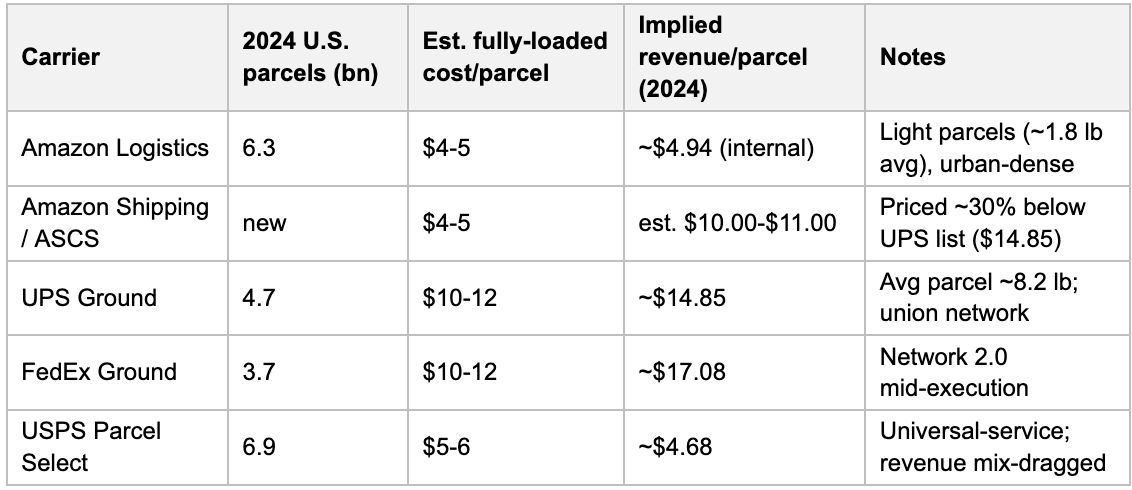

Industry-wide, the Pitney Bowes 2024 Parcel Shipping Index puts average revenue per parcel at $9.09. The fully loaded cost figures below are MWPVL and industry trade-press estimates;

Amazon’s fully-loaded cost per parcel is less than half UPS Ground’s. Even priced 30% below UPS list, ASCS clears more margin per parcel than UPS does on the same lane. That is a structural cost-curve gap that took 15 years and more than $200 billion in cumulative fulfillment capex to close.

Pooling produces ~16% of that gap. The other ~35 percentage points come from three places: a lighter average parcel (1.8 lb vs 8.2 lb), a non-union labor base (Amazon DSP blended $19-25/hr against UPS’s top union rate of $49/hr), and a more aggressive automation profile.

Pooling, on its own, does not produce the cost gap. Pooling makes it durable. It is why the gap will not close even if UPS tries harder: Amazon’s N grows alongside any operating improvement an incumbent can make.

ASCS is not just selling logistics. It is selling a measurable, signable, board-presentable margin uplift. For any Fortune 500 CPG shipping 100 million units a year, even a $2-per-parcel saving on a quarter of that volume is $50 million in annualized COGS reduction on one line item, decided in one quarter and requiring zero deployed capital. UPS cannot match the price without burning unit economics. FedEx cannot either.

I wrote in Shrinking to Win that UPS is closing up to 200 buildings by 2030, cutting 30,000 more positions in 2026, and halving Amazon’s volume.

The framing then was that UPS had built a pandemic-era network around the wrong customer and was contracting on purpose. ASCS forces a sharper reading.

UPS’s problem is not just that the Amazon volume was unprofitable. UPS’s problem is that the customer base it is counting on to replace Amazon, healthcare, SMB, and premium brands, is the exact base ASCS will pursue next.

UPS spent 2025 and 2026 engineering its way to a smaller, healthier network.

Amazon spent the same period turning surplus capacity into a product line.

Both moves are rational. Only one increases the size of the prize. Closing 200 facilities is fine on the inventory side; fewer hubs means more consolidation, but the routing penalty runs the other way. Each remaining hub serves a larger geographic area, and the replacement volume of healthcare, SMB, and premium freight is more dispersed than the Amazon volume UPS walked away from.

Cost per stop rises. The pooling gains from consolidation are real but small. The routing penalty from lost density is the larger effect on the same √N curve.

I am skeptical of UPS’s premise. UPS is right that healthcare and premium SMB have higher per-piece margins. UPS is wrong if it assumes ASCS will not eventually address those segments. AWS started by selling to startups; it now runs the largest banks and most regulated healthcare systems in the country. The arc bends toward Amazon.

P&G is now an Amazon logistics customer.

In every prior Amazon-as-platform iteration, customers ended up depending on the underlying infrastructure, thereby constraining their strategic optionality.

Marketplace sellers at significant volume found their product mix, pricing, and inventory effectively co-managed by Amazon.

AWS customers found that egress fees, region availability, and cross-cloud cost made “multi-cloud” more of a slide deck than reality.

Once a customer’s volume sits on the platform, the platform owns it. P&G, which runs freight on ASCS, will, within a few years, find itself in a similar position. The reason P&G signs is the per-parcel cost. The actual cost is the optionality.

This is the part of the playbook AWS doesn’t fully prepare us for. AWS customers compete with Amazon retail in a few places (Whole Foods, Twitch, MGM). ASCS customers compete with Amazon retail in almost every category they ship. The strategic friction is structurally higher. Amazon will need to commit, contractually, to information firewalls, capacity guarantees, and lane-pricing rules that AWS and Marketplace never had to write down. Whether those commitments are credible is the open question.

.

For most of the last decade, “what is Amazon?” has had a complicated answer. Largest online retailer. Largest cloud infrastructure provider. Third-largest digital advertising platform. Largest private logistics operator. Each is, on its own, the answer to “what is your business?” for a Fortune 100 company.

ASCS clarifies the portrait:

Amazon is not a retailer that runs other businesses on the side.

Amazon is a platform company that uses retail to set the cost curve for everything underneath it.

Retail is the demand signal.

Marketplace monetizes other people’s retail off the same signal.

AWS monetizes the compute built to handle retail.

ASCS monetizes the logistics built to fulfill retail.

Advertising monetizes the attention concentrated on retail.

Retail is not the business.

Retail is the engine that justifies the size of every other business.

This is the inverse of the QVC story I wrote about last month.

QVC built an integrated stack optimized for one demand pattern. When the pattern shifted, QVC could not unbundle and sell the layers individually. Amazon engineered every layer, from the start, to be sellable as an independent service.

QVC built its own infrastructure. Amazon built its own infrastructure and everyone else’s, then waited.

The bull case is arithmetic against AWS. AWS hit an $8B run rate by year 5, $30B by year 9, $80B by year 16. The U.S. parcel shipping market generated $203.2 billion in 2024, and Pitney Bowes projects it will reach ~$275 billion by 2030. If ASCS captures 5% of that future market, that is $14 billion of annualized non-Amazon revenue; 10% capture is $27 billion; 15% is $41 billion. Apply a 25% operating margin assumption, below AWS’s 38%, because logistics incurs higher variable costs, and the bull case adds $3-10 billion of segment operating income by 2030.

Signals to watch: named enterprise customers, average revenue per customer, growth in non-Amazon volume, segment margin once Amazon discloses it. If ASCS hits 100 named customers and a $5 billion run rate by the end of 2027, the bull case is in motion. If it hits neither by the end of 2028, the AWS analogy is wrong.

The bear case has three legs.

Regulatory: the FTC, EU, and several state AGs are explicitly watching for Amazon to use its position in one market to leverage another. ASCS is a textbook example of the practice they are looking to address.

Customer trust: if P&G or 3M finds itself in an Amazon Basics competition that ASCS subsidizes through information advantage or capacity prioritization, the trust required to run a logistics partnership erodes. The commitments Amazon will have to make compress the margin profile that makes ASCS attractive in the first place.

Competition: a leaner UPS executing its automation roadmap and a reinvigorated FedEx coming out of Network 2.0 may defend SMB and healthcare segments at price points ASCS cannot match without burning unit economics.

If the bull case is right, ASCS is the next AWS. If the bear case is right, ASCS is a constrained business that hits a regulatory or trust wall. Either way, UPS and FedEx have to assume the bull case in their own planning, because the cost of being wrong is too high to absorb.

Twenty years ago, Amazon decided to stop treating IT infrastructure as a cost to minimize and start treating it as a platform to monetize. That decision is among the largest contributors to shareholder value in the last quarter-century.

The question every operating company should ask in 2026 is the one Bezos asked in 2003. What is in my cost center that, running at an unreasonable scale, would have buyers?

For most companies, the answer is nothing, because most cost centers were not built at the scale required for conversion. That is the deeper signal. Amazon’s strategic edge is not the cost centers it has converted. The edge is the willingness, decades earlier, to build cost centers at a scale where the square root law of pooling could begin to do real work. The willingness to spend $83 billion of capex in a single year. The willingness to invest in a logistics network as if it were a profit center long before it was monetized. The willingness to be wrong for a decade.

The Amazon pattern is, at heart, a pattern of progressive pooling.

Marketplace pools sellers.

AWS pools tenants.

Ads pool impressions.

ASCS pools shippers.

Each move increases N by an order of magnitude on a different operating axis. Each move pushes the company further down the same √N cost curve.

UPS spent fifteen years optimizing its network for a game whose rules were already changing. Amazon spent fifteen years building the next one.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。