First-time homebuyers are searching for homes they can grow into rather than trade up quickly

Send this article to your social connections.

The concept of a “starter home” implies eventual mobility, a house that’s outgrown in favor of something that accommodates shifting taste, family size, or other preferences. But as buyers enter the market increasingly later in life — spending their earlier years renting — by the time they purchase, that home may be the first and the last stop, at least for a long while.

A starter home, in theory, is “not someone’s forever home, but a stepping stone,” said Mary Yazbeck, principal broker for Yazbeck Realty Group, based in Braintree. Starter homes may have modest square footage, a lower room count, a need for some cosmetic updates, and come in at a lower price point for the area with lower monthly payments.

Advertisement:

According to estimates provided by the National Association of Realtors (based on the median sales price for the Boston metro area in the first quarter of 2026), a starter home might cost around $635,715, requiring an annual income of $169,970 to qualify for a loan. (A typical renter’s income in the Boston metro area is $76,260, NAR estimates.)

But for some, the concept may be becoming more malleable.

“Younger buyers and newly married couples may still search with a starter-home mindset, but today they’re often looking for flexibility,” she said. That could look like accommodating lifestyle changes such as future children, remote work, multigenerational living, and the ability to renovate over time because they know the next move might not be soon, or easy.

Advertisement:

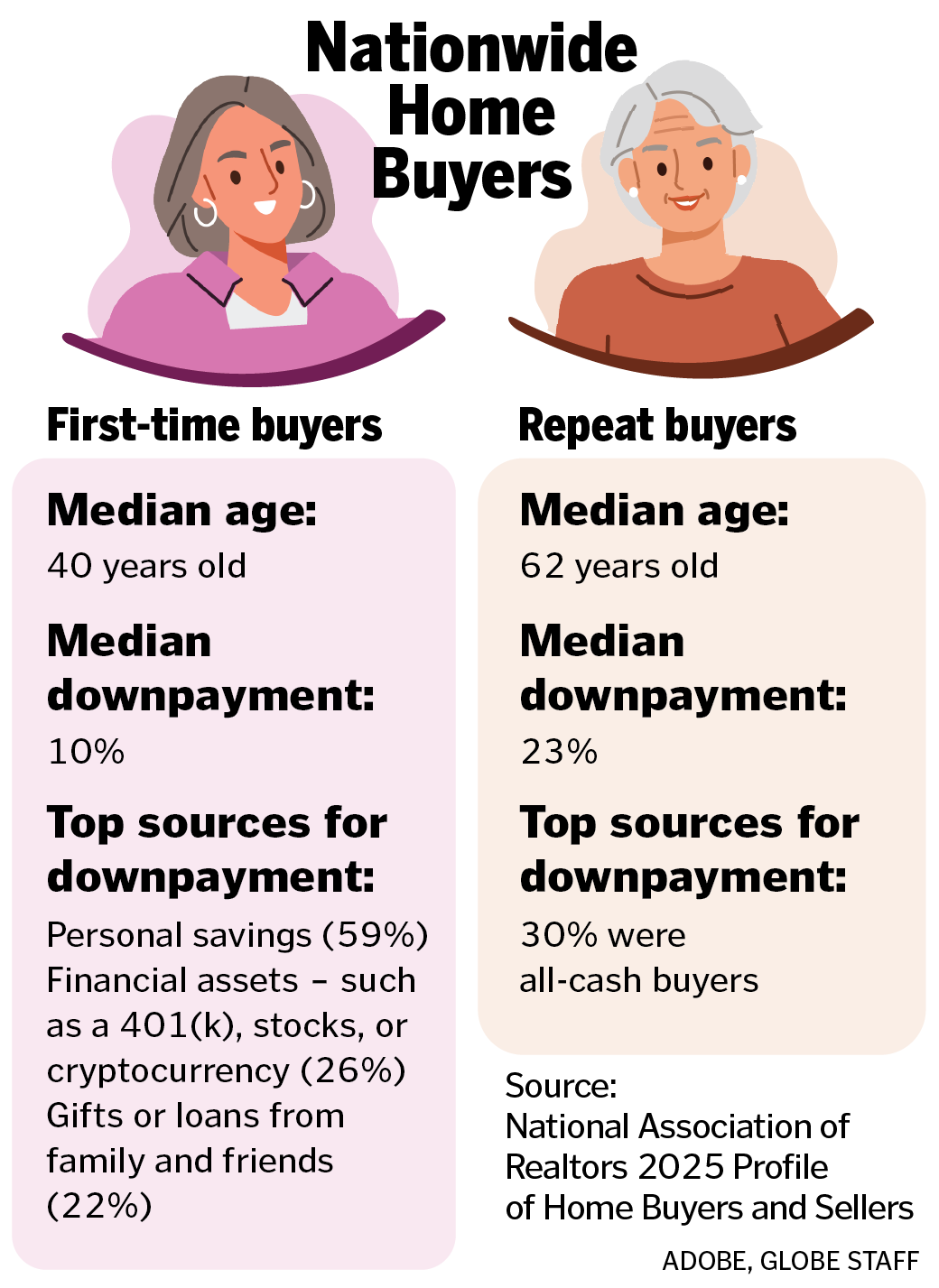

The first-time homebuyer rate hit a national all-time low of 21 percent of the market in 2025, according to the National Association of Realtors’ most recent annual survey. Down payments commanded an all-time high since 1989, too, at 10 percent of total home prices. First-time homebuyers were a median age of 40 years old by the time they bought.

True starter homes are a “thing of the past,” said Patrick O’Donnell, a Keller Williams Realtor based on the South Shore.

“People are just glad to get into their home now,” he said. “They’re not moving as often.”

“I’m seeing clients prioritize stability and ownership over the idea of quickly ‘moving up,’” Yazbeck said. “Many of them are purchasing homes they intend to live in for the next decade, anticipating limits brought on by low inventory and high inventory and pricing. Instead of moving into something bigger, they’ll spend that money renovating where they are.”

But “fixer upper” can mean many things depending on who you ask.

“When you talk to a buyer, and they say, ‘I want a fixer upper,’ you need to ask them the next question, ‘Well, what does that look like to you?’” said Kimberly Allard, a broker/owner with Century 21.

Advertisement:

Often, clients will answer that they’re prepared to paint and replace flooring, but she said every buyer should be prepared to do that. Asking deeper questions about lifestyle goals can save a lot of trouble down the line as a true “fixer-upper” is no shortcut to a bargain.

Most homes in Boston’s antique housing stock would probably qualify as needing fixing up, and renovation and labor costs could negate potential savings there, O’Donnell said. Plus, for those who work full-time to afford the mortgage, there isn’t much time left to DIY.

“Unless you’re a handyman … you really want to look for turnkey because it can add up very quickly,” he said.

Sometimes vision and practice don’t align, Allard said. For example, those who travel most weekends might not be the best candidates for the kind of house that demands long hours on weekend improvements. A condo could be a better fit.

According to the Commonwealth of Massachusetts, of about 3 million housing units statewide, 57 percent are single-family homes, 20 percent are two- to four-unit multifamily buildings, and 22 percent are larger complexes — and all are exhibiting low vacancy rates. Expect about $500,000 for entry-level pricing in a 30-mile radius outside Boston, O’Donnell said.

Advertisement:

NAR estimates that only 34 percent of homes in the Boston metro area are priced below their “starter home” threshold of $636,000, and 24.7 percent are priced below $551,000. If you’re aiming to reserve 20 percent for a down payment, that’s $100,000. But don’t count yourself out, or even count that high, Allard said.

“Some people think that they need a large deposit, which you absolutely do not,” she said. “There are many loan products out there that allow you to buy a home if you are properly qualified with very little down.”

In April, the Massachusetts Housing Finance Agency announced a first-time homebuyer assistance program for qualifying buyers, offering $25,000 in interest-free down payment assistance until July.

Partnering with a real estate agent who can help navigate potential programs for first-time buyers is essential, Allard said. (She advises looking for certified Realtors who are members of the National Association of Realtors trade association that follows a dedicated ethics code.)

Managing expectations, and emotions, is an important piece of the first-time home-buying process, said Toyosi St. Cyr, a Realtor and first-time homebuyer specialist with Keller Williams based in Franklin. Baby boomers who are looking to downsize are often the competition and may come to the table ready to make a cash purchase. That’s often more appealing to sellers than first-timers with custom mortgage products and less flexibility. But it can be soul-crushing to buyers who lose out in negotiation. St. Cyr said she coaches clients to expect that it might take more than one offer and multiple potential homes before a deal is closed.

Advertisement:

“It’s really [about] helping them understand the difference between a starter home and a dream home,” she said.

Jonathan Lane, 32, who just closed on a $295,000 Northborough condo with 10 percent down, said he hopes to outgrow the unit eventually. And this first time around has given him experience navigating the process. He received an overly optimistic preapproval estimate from the bank that would land him a mortgage “way, way, way higher than anything I could pay normally,” he said. So, he purchased at about $100,000 less than his initial approval, which resulted in more realistic monthly payments.

As a starter home, condo life looked more flexible to Matthew Hadeka, who just closed on a three-bedroom Brookline unit in a multifamily building.

“There’s less overhead associated with owning a condo,” he said. “I think there’s some level of peace of mind or comfort in having more flexibility down the road if we are in a position that we feel we can either move elsewhere by choice, or move elsewhere to upgrade.”

Dianna Bronchuk Duran, 31, of Roslindale, found herself unexpectedly on the market after the sudden loss of her father left her equipped to make a down payment. Duran, who grew up in a townhome, said she’s open to alternate housing formats for her husband and herself, including a scenario in which the couple buys with friends. An additional variable is her residency requirement as a public employee in Boston.

“It’s scary, it’s an anxious moment, [and] it’s invigorating,” she said. “It’s cool to be able to walk through these different places and try to play Sims in your head of where you’re going to put things.”

Advertisement:

Address Newsletter

Our weekly digest on buying, selling, and design, with expert advice and insider neighborhood knowledge.

Want to leave a comment?

To comment, please create a screen name in your profile