Hannah Aldridge, Senior Research and Policy Analyst at the Resolution Foundation, explains why having a decent salary isn't always enough to get a mortgage, and what we can do about it.

by

I’ve reached a point in my life where many of my peers are homeowners who talk about things like ‘kitchen triangles’[1]. As someone who doesn’t own their home, I nod smile and remind myself that I’m not alone. That’s what the data says anyway – the number of mortgagors is falling, more so among low and middle income households than for richer families. So, to what extent can I / we lay the blame for that trend on how easy – or otherwise – it is for typical households to get a mortgage?

In Credit Where Credit’s Due? we’ve had a go at figuring out the extent to which the financial regulatory system is holding back aspiring homeowners. We identify 8.3 million potential first‑time buyer families – working adults aged 21–55 who do not own a home – and model the tests that they would have to pass to get a mortgage on a ‘starter home’ (the lower quartile price of a terraced home in their region).

The surprising thing? Their earnings are not (directly) holding them back. Almost half of potential buyers have enough income to qualify, but they simply don’t have enough saved. Only 15 per cent have enough piled up in the bank to lay down even a 5 per cent deposit.

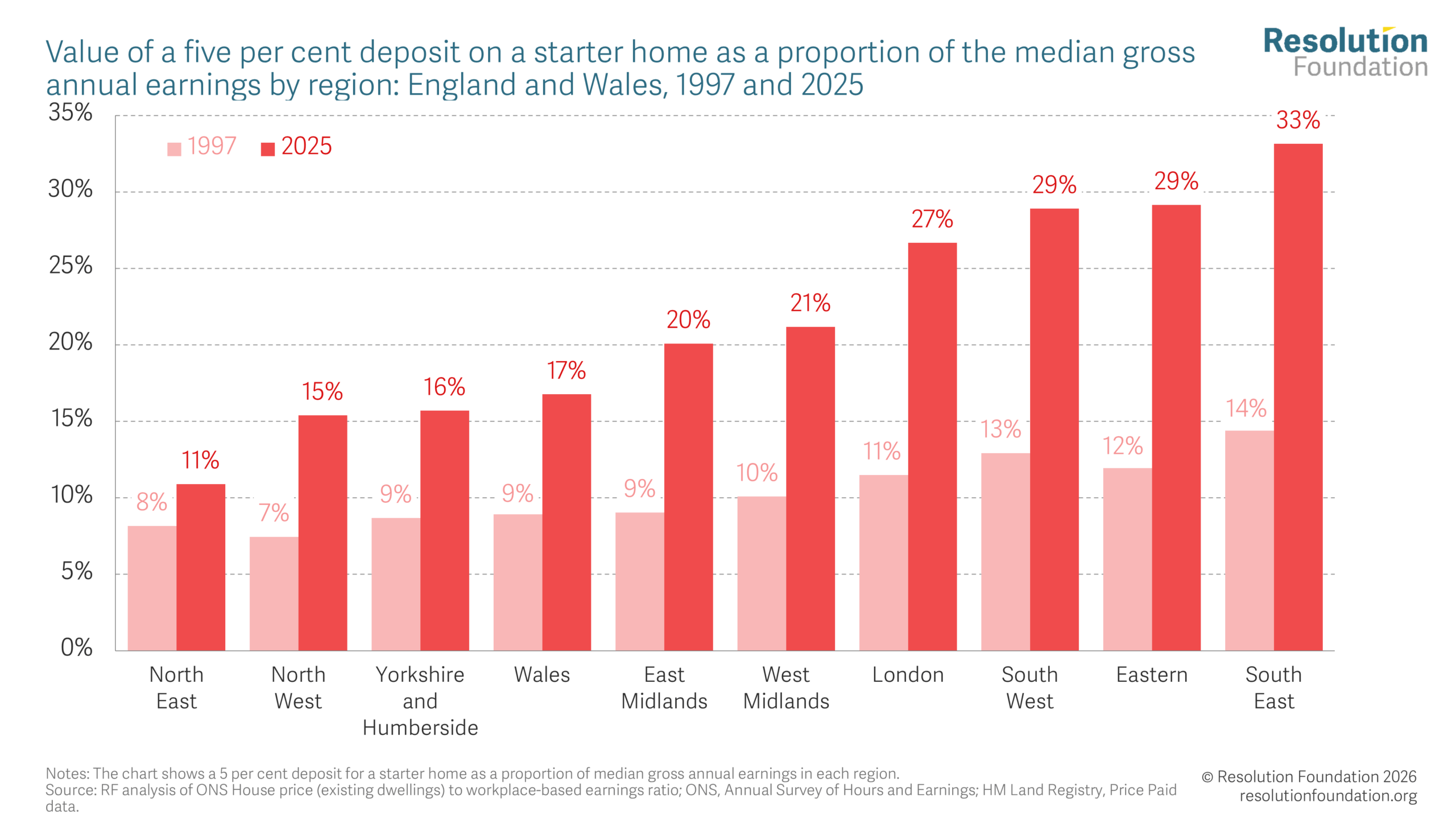

This comes down, ultimately, to house prices. As their growth has consistently outpaced that of earnings, saving enough for a deposit has become increasingly time consuming. In most parts of the country, the size of a 5 per cent deposit on a modest starter home has more than doubled relative to median earnings, so that now 1.7 million potential buyers would need to save for more than a decade before they could think about buying. The result is an unequal system, where around one‑third of first‑time buyers rely on financial support from family or friends – a boon that’s not on the table for the majority.

The value of a deposit for a starter home has more than doubled in nearly every region of the country over the last thirty years

It’s tempting, then, to think that loosening mortgage lending rules would help a clear path to increased homeownership. But we’ve found that a wider rollback of financial regulation would carry significant risks – without even addressing the core problem.

Repayment burdens for first‑time buyers are already historically high at around 22 per cent of gross income. That’s a level we only used to see in the run‑up to housing crashes. So, it really doesn’t look as though the lending rules are too tight. Plus, research from the Bank of England shows that increasing the flow of mortgage credit raises house prices without expanding homeownership. So, a wholesale loosening of credit would be both risky and futile, to put it bluntly.

If the aim is genuinely to support those currently unable to get on the housing ladder, the solutions lie elsewhere. Luckily, we have come up with another option. We propose a game changing Starter Deposit scheme aimed at the 1 million families who could afford mortgage repayments (and already spend as much or more on rent) but lack the upfront savings needed to buy. The scheme would provide an equity loan worth 5 per cent of a deposit on a starter home, so long as the buyer can secure a mortgage on the rest. It would be available on both new‑build and existing properties and capped to keep it targeted on those unable to secure a deposit. For our target group, this could reduce their annual housing costs by £2,600.

None of this replaces the long‑term need to build more homes, which is the most effective way to improve affordability and living standards in the long term. But while progress on supply is slow, there is still space to support aspiring homeowners through targeted deposit support.

[1] The triangle shape that would be formed in a kitchen if a line was drawn between the sink, hob and fridge.