An AI-powered credit decisioning engine automates the evaluation of loan applications using machine learning models trained on borrower data, credit history, and behavioral signals. In auto lending, these platforms score applications, apply policy rules, and issue approvals or declines — in some cases within milliseconds — replacing or augmenting the manual underwriting review process that traditional institutions rely on. For a broader look at how modern auto credit decisioning software fits into the full lending risk architecture, this post covers the landscape in which these engines operate.

These platforms primarily market speed. However, what is often overlooked in marketing presentations is that nearly two-thirds of organizations have yet to scale AI across their enterprises, as highlighted by McKinsey’s 2025 Global Survey on the state of AI. The main obstacles are not related to technological deficiencies. Instead, they stem from data readiness issues and a lack of clarity around use cases. Most lenders find themselves in the gap between deploying an AI decisioning platform and deriving measurable portfolio value from it.

This gap continues to grow. According to Experian’s research, 65% of lenders are finding it difficult to obtain AI-ready data, despite 89% recognizing AI as essential throughout the lending lifecycle. A platform that offers millisecond decision-making is only as accurate as the data it processes. If that data consists of a flat-file snapshot of unchanging borrower credit score and other attributes, the speed advantage is lost at the point of initial interaction with outdated information.

The evaluation question a CRO should ask is not “How fast does this engine approve loans?” It is “What does this engine see that my current scorecard misses — and can I defend that to an examiner?” dotData Signal Intelligence is not a decisioning engine. It is the Signal Intelligence layer that sits upstream — surfacing Driver Signals and Precision Impact Segments from multi-table relational data that macro-level decisioning engines are architecturally incapable of computing. The distinction matters at the P&L level and at the examination table.

The difference between a scorecard and an AI decisioning engine is not as dramatic as vendors often imply; at the same time, it is substantially more significant than many Chief Risk Officers (CROs) may recognize. The difference is less pronounced because both tools rely on historical averages and produce aggregate output that provides insight into risk concentrations. More significantly, however, as McKinsey pointed out, institutions that have effectively integrated AI into credit scoring are already gaining advantages in loss-rate performance, decision speed, and customer experience. The competitive advantages enabled by AI will become difficult to overcome as they accumulate over multiple innovation cycles.

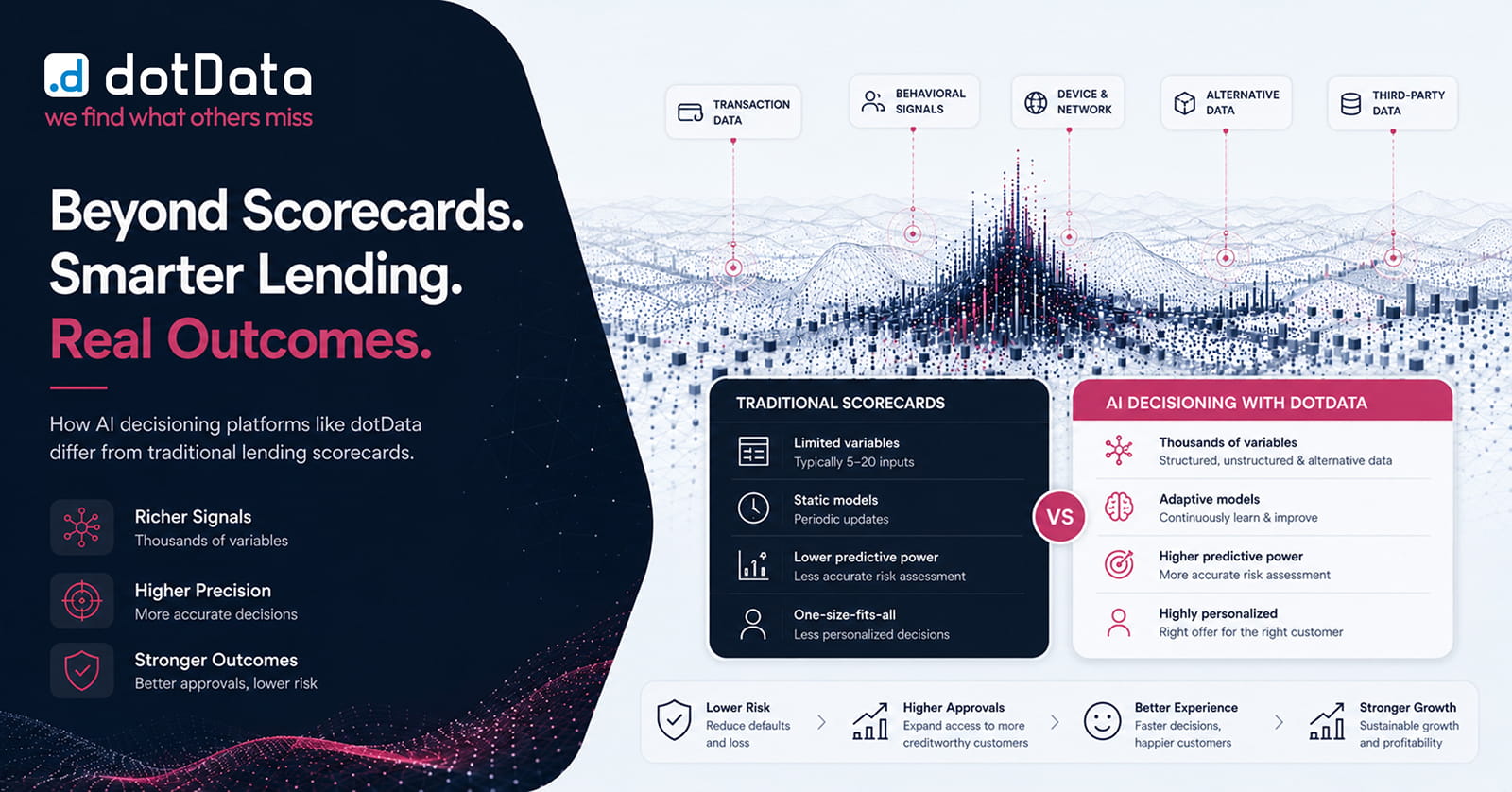

Traditional scorecards evaluate a fixed set of borrower attributes — FICO, DTI, LTV — as static, point-in-time inputs. AI decisioning platforms extend that by processing larger sets of variables and applying machine learning to dynamically weight them. The functional gap is not variable count. It is about whether the platform detects non-obvious multi-table behavioral interactions that no human team would have thought to encode as a rule, and whether it can produce an auditable explanation of what it found.

Most commodity AI platforms fail that second test. They evaluate the variables they have been given; they do not programmatically explore the cross-table relational space to surface the interactions nobody thought to look for. The Signal Discovery Console does. By automatically evaluating millions of relational combinations across the LOS, LMS, and credit bureau data simultaneously, it produces Driver Signals that no scorecard or standard AI platform can generate — because those platforms are structurally limited to the hypotheses their designers encoded. The difference appears on the roll rate line six months after origination. Either the sub-segment was caught before funding, or it was charged off.

The CFPB set the compliance standard in its September 2023 Consumer Protection Circular: lenders must provide specific, auditable reasons for adverse action, even when AI drives the credit decision. “The algorithm decided” violates ECOA and Regulation B. That is not a future regulatory concern — it is current enforcement posture, and it applies regardless of model complexity, vendor architecture, or institution size.

The implication is clear. Per OCC 2025 supervisory feedback, 35% of AI models at community and regional banks get rejected due to inadequate explainability documentation. The 35% figure is not a failure of technology. Still, it is, in fact, due to a lack of architecture that begins the instant a lender chooses a black-box decisioning platform, without auditing what that platform can actually produce when an examiner requests documentation for loan rejections. In many instances, lenders cannot show the documentation; they can show a credit score – and that’s not the same thing.

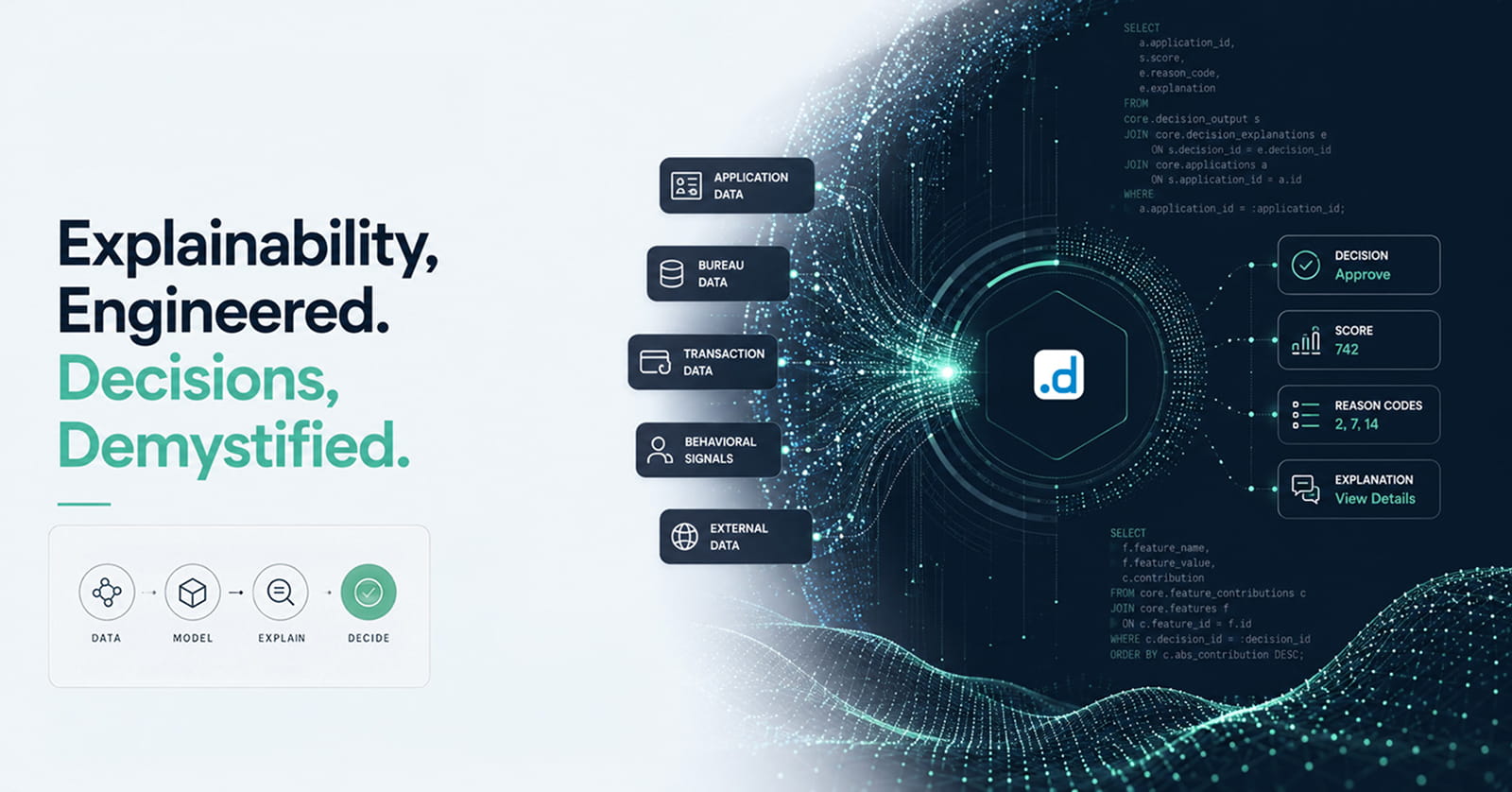

Explainability in AI-based credit decisioning means that the model logic should be traceable and well-documented, and that both borrowers and examiners should be able to understand the reasons behind adverse decisions. Under ECOA and Regulation B, lenders must provide specific, accurate reasons for adverse actions, even when an algorithm makes the decision. In fact, in algorithmic decisions, the need for transparency is even greater, since the algorithm’s full reasoning process may not be clear to either regulators or borrowers.

dotData Signal Intelligence is fundamentally a Glass Box architecture starting from the output layer. A well-documented rationale accompanies every Driver Signal — outlining the precise relational pattern, the population-match volume, and the directional lift above the portfolio baseline — conveyed in simple language and available for export as SQL. The Signal Intelligence WorkBench produces SQL rules that are ready for production: deterministic, traceable, and defensible to a credit committee or examiner without requiring further translation. Your compliance team is provided with the logic, not merely a confidence interval.

Most risk evaluations start with the wrong question. “How high is your automated underwriting rate?” optimizes for speed — which matters until the vintage deteriorates. The credit committee wants to know which specific segments the platform cleared and why. 80% of banks and credit unions plan to increase technology spending in 2026, per Cornerstone Advisors, yet many continue to fall short on planned system deployments. The implementation gap is not the budget. It is the absence of a disciplined evaluation framework that distinguishes Glass Box enrichment from black-box automation before contract signing.

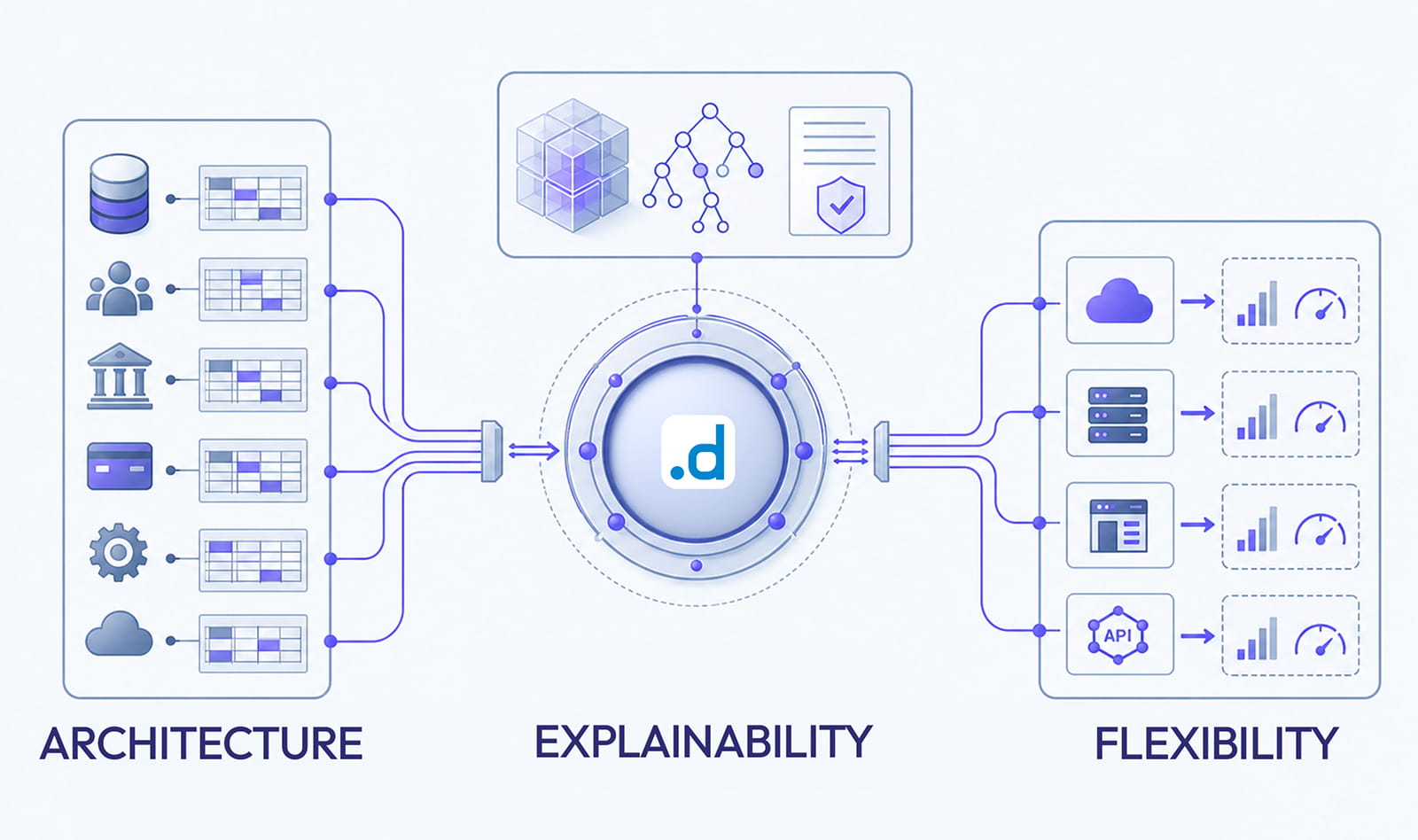

Determining which platform is the right credit decisioning software for a highly regulated industry like auto lending depends on several factors, but three stand out. First is the architecture itself. The platform should be able to leverage data from multiple internal and external data sources, and connect the information in relational ways without requiring a flat-file export to be prepared upstream. Next, explainability is key. The platform should generate easily auditable Glass Box rules that provide documented lift without needing human interpretation to translate black-box rules into policy language. Finally, deployment flexibility means that the system should make it relatively easy to move from identified signals to new or revised Post Model Adjustments without lengthy IT development cycles. Other functions, such as dashboards, the user interface, and vendor support policies, become preferences rather than critical functions.

Based on the outlined criteria, dotData Signal Intelligence can directly ingest multi-source, multi-table relational data without pre-flattening, using Glass Box SQL-based rules that yield documented lift. dotData enables easy post-model adjustments within an existing LOS workflow without altering the core system. Any new decisioning platform should be tested against the same criteria to identify exactly which layer is deficient and offer the credit committee a defensible basis for future procurement decisions.

Here’s the objection that stalls most AI decisioning evaluations: “Our LOS integration would be a six-month IT project.” It is the most common concern raised — and the most avoidable — because IT complexity is almost always a function of the platform’s output format, rather than the integration itself. Platforms that output black-box risk scores require integration work because the score must be manually mapped to a policy rule written separately by a human. That translation layer is where IT projects are born.

Platforms that output Glass Box SQL rules eliminate the need for that translation layer. The discovered Driver Signal becomes the PMA rule; the PMA rule goes directly into the existing LOS connector in the format the LOS already consumes—no IT project required. The loan portfolio monitoring infrastructure the institution already runs is the deployment environment — not the target for a rebuild. The credit team controls the rule; the LOS applies it; the examiner can trace it.

The Automated Pipeline Engine in the Signal Discovery Console automatically generates production-ready SQL and tracks every preprocessing and signal selection decision, ensuring the output is auditable end-to-end. For the CRO or VP of Lending operating inside the Signal Intelligence WorkBench, that SQL becomes a checkbox PMA rule in the existing workflow — no data science intermediary required between discovery and deployment. Discovery-to-deployment compresses from months to days—with zero modifications to the core LOS.

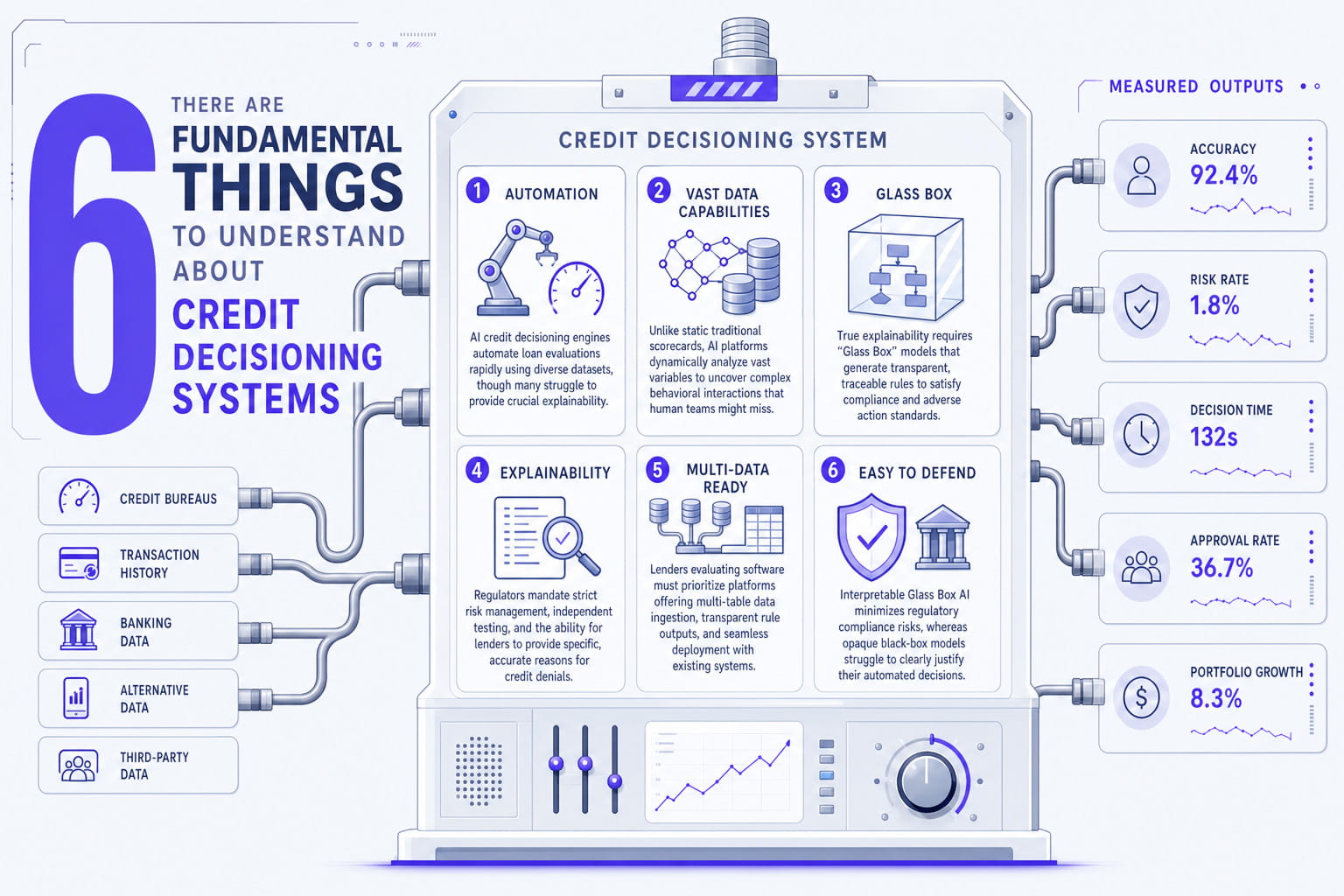

An AI-driven credit decisioning engine is a machine learning framework that streamlines the evaluation of loan applications — assessing borrower risk, enforcing policy regulations, and granting approvals or rejections without requiring manual underwriting review.

For auto lenders, these systems can evaluate application criteria in seconds, using diverse data sources that go far beyond conventional FICO and DTI metrics and can incorporate behavioral, transactional, and alternative data points. The core advantages are speed and scalability. Explainability and the discovery of multi-table, multi-source signals are key features that many such platforms fail to address.

Traditional scorecards apply fixed weights to a fixed set of variables — calibrated to historical averages and evaluated at a single point in time. AI platforms dynamically weight larger sets of variables and can update model logic more frequently. The functional gap is not the number of variables. It is whether the platform detects multi-table behavioral interactions that no human team thought to encode as a rule, and whether it can explain what it found to an examiner in terms that satisfy ECOA adverse action requirements.

Explainability means the model’s logic can be traced from input to output, documented in a format that satisfies SR 11-7’s independent validation requirement, and communicated in plain language for ECOA adverse action notices. A Glass Box model produces deterministic, readable rules — specific behavioral conditions, directional lift above baseline, exportable SQL. A black-box model produces a static credit score, leaving the institution responsible for constructing an explanation that the model itself did not generate.

The Office of the Comptroller of the Currency (OCC) requires all banks to properly manage the risks associated with credit models, including AI-based models. This means testing them independently, regularly tracking their actual performance, and keeping clear records. While community banks with assets under #30 billion have more flexibility in how often they test, they must still manage these risks. Additionally, the Consumer Financial Protection Bureau (CFPB) requires lenders to provide applicants with specific, accurate reasons for any denied credit, even if they use highly complex AI in their lending operations.

The three essential criteria, prioritized as follows: ingestion of multi-table relational data (rather than flat-file scoring), output that adheres to the Glass Box rule (rather than relying on black-box scores), and compatibility of PMA deployment with the current LOS (rather than necessitating an IT overhaul). All other factors — such as user interface, vendor support levels, and reporting dashboards — are secondary until these three conditions are satisfied. A vendor unable to showcase all three during a live evaluation is addressing a different inquiry than what regulators will pose.

A black-box AI model produces scores or probabilities based on logic that cannot be fully traced to human-readable rules. Glass-box scoring models, on the other hand, provide deterministic and interpretable logic that shows conditions, directional lifts over the average, and rules that can be conveyed in plain language. A Glass Box model, when subjected to auditing, can be justified to regulators and is suitable for communication to borrowers who are set to receive adverse action notices. According to the CFPB and the OCC, black-box outputs lacking sufficient supplementary explainability documentation pose a compliance risk.

The three-gate framework — multi-table data ingestion, Glass Box output, PMA compatibility — is not a dotData proprietary checklist. It is what SR 11-7, OCC Bulletin 2025-26, and CFPB adverse action guidance collectively require of any AI model touching credit decisions. Most lenders discover the gaps during an examination. The alternative is running the audit before the examiner does.

If the gaps are visible, talk to the dotData lending team.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。